[ad_1]

USDA eligibility for 2021

USDA eligibility is predicated on a mixture of family measurement and geography, as well as to the standard mortgage approval requirements akin to revenue and credit score rating verification.

Households of 1-4 folks can have an revenue as much as $91,900 in many of the U.S., and households with 5 or extra members could make as much as $121,300. USDA revenue limits are much more beneficiant in some areas with a better price of dwelling.

When you’re shopping for a house exterior of a significant metropolis, and have first rate credit score, it’s value checking your eligibility for this zero-down mortgage program.

Verify your USDA loan eligibility (Jun 19th, 2021)

On this article (Skip to…)

The USDA dwelling mortgage program

The USDA mortgage program is without doubt one of the finest mortgage loans out there for qualifying debtors.

There’s no down fee required, and mortgage insurance coverage charges are sometimes decrease than for standard or FHA loans. USDA rates of interest are typically below-market, too.

To qualify for 100% financing, dwelling patrons and refinancing owners should meet requirements set by the U.S. Division of Agriculture, which insures these loans.

Fortunately, USDA tips are extra lenient than many different mortgage sorts.

USDA eligibility necessities

Primary USDA mortgage necessities embody:

- Minimal credit score rating — 640 with most lenders

- Clear credit score historical past — No late funds or current chapter or foreclosures

- Earnings necessities — Earnings limits differ by space; typically $91,900 for a 1-4 individual family

- Employment — Debtors want a gradual revenue and employment historical past. Self-employment is eligible

- Geographic necessities — You have to personal a house in an eligible space

- Property necessities — Should be a single-family dwelling you’ll use as your major residence

- Mortgage sort — Solely a 30-year, fixed-rate mortgage is allowed

As well as, most USDA lenders need debtors to have a debt-to-income ratio (DTI) beneath 41 p.c.

Meaning your month-to-month debt funds (together with issues like bank cards, auto loans, and your future mortgage fee) shouldn’t take up greater than 41% of your gross month-to-month revenue.

This rule just isn’t set in stone, although.

USDA is versatile about its mortgage necessities. And lenders can generally approve functions which can be weaker in a single space (like credit score rating or DTI) however stronger in one other (like revenue or down fee).

USDA’s purpose is to assist low- and moderate-income patrons grow to be owners. So for those who meet the fundamental standards — otherwise you’re shut — verify your eligibility with a lender.

Verify your USDA loan eligibility (Jun 19th, 2021)

USDA revenue limits

USDA’s revenue restrict is about at 115% of your space’s median revenue (AMI). Meaning your family revenue can’t be greater than 15% above the median revenue the place you reside.

The precise greenback quantity varies by location and family measurement. As an example, USDA permits a better revenue for households with 5-8 members than for households with 1-4 members.

And, USDA revenue limits are larger in areas the place staff sometimes earn extra.

Right here’s only a pattern to point out you the way USDA revenue eligibility can differ by location:

| Space | 2021 Earnings Restrict for 1-4 Individual Family | 2021 Earnings Restrict for 5-8 Individual Family |

| Adams County, Nebraska | $91,900 | $121,300 |

| Duluth, Minnesota | $96,300 | $127,100 |

| Olympia-Tumwater, Washington | $103,700 | $136,900 |

| Napa, California | $135,250 | $178,550 |

You may check current USDA income limits for your county here.

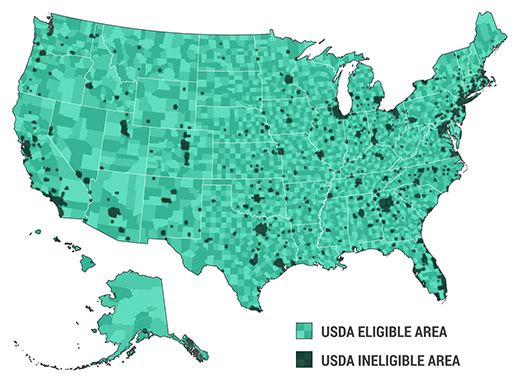

USDA property eligibility

Formally referred to as the ‘rural growth mortgage,” USDA’s mortgage program is meant to advertise homeownership in underserved elements of the nation.

Due to this, the USA Division of Agriculture will solely assure loans in eligible “rural” areas.

However don’t be deterred. USDA’s definition of ‘rural’ is looser than you may anticipate at first.

You don’t have to purchase loads of land or work in agriculture to be USDA eligible. You simply must reside in an space that’s not densely populated.

Formally, USDA defines a rural space as one which has a inhabitants beneath 35,000 or is “rural in character” (which means there are some particular circumstances). And that covers the overwhelming majority of the U.S. landmass.

So earlier than you write off a USDA mortgage, verify your space’s standing. You’ll find out if a property is eligible for a USDA mortgage on USDA’s website. Most areas exterior of main cities qualify.

USDA eligibility map

Supply: USDAloans.com based mostly on Housing Assistance Council information

USDA mortgage insurance coverage necessities

The USDA single-family housing assured program is partially funded by debtors who use USDA loans.

Through mortgage insurance coverage premiums charged to owners, the federal government is ready to preserve the USDA rural growth program reasonably priced.

USDA final modified its mortgage insurance coverage charges in October 2016. These charges stay in impact at this time.

At this time’s USDA mortgage insurance coverage charges are:

- 1.00% upfront charge, based mostly on the mortgage measurement (could be rolled into the mortgage stability)

- 0.35% annual charge, based mostly on the remaining principal stability

As a real-life instance of how USDA mortgage insurance coverage works, let’s say {that a} dwelling purchaser in Cary, North Carolina is borrowing $200,000 to purchase a house with no cash down.

The client’s mortgage insurance coverage prices embody a $2,000 upfront mortgage insurance coverage premium, plus a month-to-month $58.33 fee for mortgage insurance coverage.

Be aware that the USDA upfront mortgage insurance coverage just isn’t required to be paid as money. It may be added to your mortgage stability to cut back your funds required at closing.

Verify your USDA eligibility

USDA-guaranteed loans can be utilized for dwelling shopping for and to refinance actual property you already personal (so long as it’s in an eligible space).

For individuals who qualify, that is typically among the best mortgage choices out there.

USDA loans are nice for first-time dwelling patrons particularly, as you don’t want any cash saved up for the down fee. However keep in mind — you’ll nonetheless should pay for closing prices.

It may very well be simpler than you suppose to qualify for a house mortgage by way of the USDA program. Verify your eligibility with a USDA-approved lender at this time.

[ad_2]

Source link

{kind=link}