[ad_1]

Is a USDA mortgage or FHA mortgage higher?

USDA and FHA are two wonderful mortgage choices. Both one can get you right into a home with few out-of-pocket prices and a low rate of interest.

Is one higher than the opposite? That relies on your scenario.

USDA loans enable zero down fee, however there are location and

revenue restrictions to qualify. FHA loans are extra versatile about revenue,

credit score, and placement, however have greater upfront prices.

Fortunately, there’s a straightforward method to decide on. Simply ask your lender about

USDA loans and FHA loans.

You is perhaps eligible for one however not the opposite. And in the event you’re

eligible for each, you’ll be able to evaluate charges and costs to see which mortgage choice is

higher for you.

Compare USDA and FHA loans (Mar 18th, 2021)

On this article (Skip to…)

USDA vs. FHA eligibility

A big a part of the choice between USDA vs. FHA relies on which

kind of mortgage you qualify for.

Right here’s a quick overview of how USDA and FHA eligibility necessities

evaluate:

| USDA Mortgage | FHA Mortgage | |

| Minimal Down Fee | 0% | 3.5% |

| Minimal Credit score Rating | 640 | 580 |

| Upfront Mortgage Insurance coverage Price* | 1% of mortgage quantity | 1.75% of mortgage quantity |

| Annual Mortgage Insurance coverage Price | 0.35% of mortgage quantity | 0.85% of mortgage quantity |

| Revenue Limits | Max. 15% above native median revenue | None |

| Location Necessities | Should be in a professional “rural space” | None |

| Mortgage Limits | None | Max. $356,362 in most areas |

| Eligible Mortgage Varieties | 30-year fixed-rate mortgage | 30-year fixed-rate , 15-year fixed-rate, or adjustable-rate mortgage |

| Eligible Property Varieties | Single-family major residence | 1-, 2-, 3-, or 4-unit major residence |

*For each mortgage sorts, the upfront mortgage insurance coverage payment will be rolled into the mortgage quantity so that you don’t must pay it upfront

Compare USDA and FHA loans (Mar 18th, 2021)

USDA vs. FHA vs. standard

A USDA home loan is commonly your best option for debtors who meet the U.S. Division of Agriculture’s tips.

With no down fee requirement and low mortgage insurance coverage charges,

USDA mortgages are sometimes cheaper each upfront and in the long term than FHA

loans.

USDA could also be cheaper than standard financing, too, you probably have a

credit score rating within the low 600’s and a small down fee.

Nonetheless, not everybody will meet USDA’s geographic or revenue necessities.

And, the minimal credit score rating for USDA is 640 — which is even greater than the

minimal for standard mortgages (620).

For these with decrease credit score, or those that don’t meet USDA tips, an FHA loan may very well be an awesome alternative.

The Federal Housing Administration solely requires 3.5% down and a 580

FICO rating. That’s about as lenient as credit score necessities go for mortgages.

Another choice is a 3%-down conventional loan, which has comparable upfront prices and affords the potential for decrease month-to-month mortgage funds. In case you have good credit score, a standard mortgage could reward you with decrease rates of interest and mortgage insurance coverage prices.

All that may sound like lots to think about. We break down every

issue in additional element beneath.

However the important thing factor to recollect is that many lenders supply all three

sorts of mortgage loans. So that you don’t must make a ultimate choice in your

personal.

Your mortgage officer or mortgage dealer can assist you evaluate USDA, FHA,

and standard loans to seek out the most effective mortgage for you.

Find the right mortgage for you (Mar 18th, 2021)

USDA house

mortgage professionals and cons

What in the event you might get a no-down-payment mortgage with

comparable mortgage charges to FHA? And what if that mortgage allowed you

to finance closing prices, even with out an ultra-high credit score

rating?

This mortgage truly does exist, and it’s

known as the U.S. Division of Agriculture (USDA) Rural Improvement house mortgage. Extra

generally, it’s recognized merely as a ‘USDA mortgage.’

The USDA mortgage has shortly risen in reputation with

first-time and lower-income debtors due to its zero-down allowance

and low charges. However not everybody will qualify. Right here’s what you need to know.

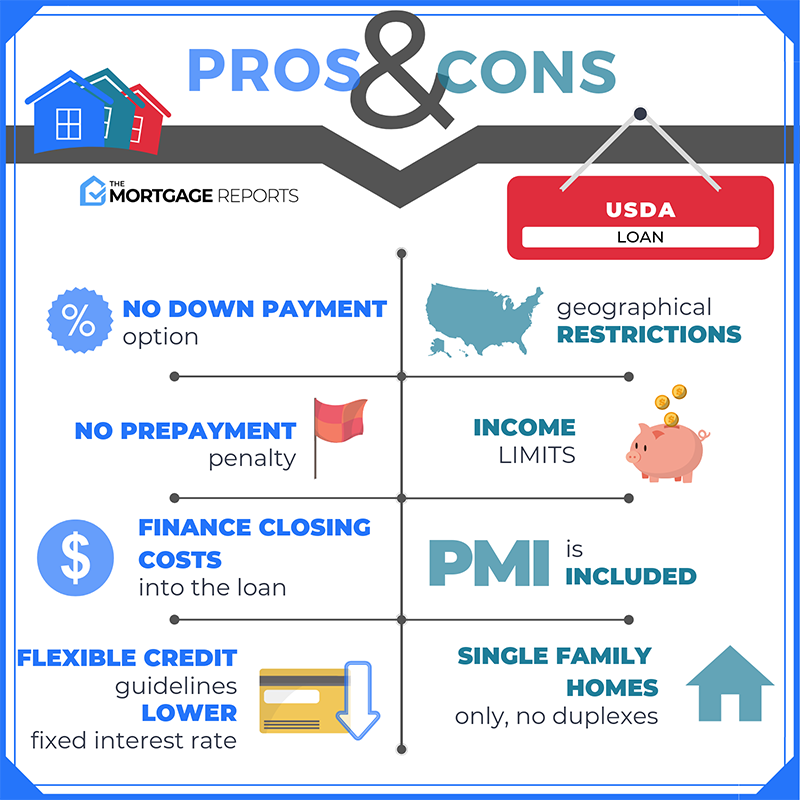

USDA professional: Zero down fee required

USDA loans require no down fee. You

could finance as much as 100% of the property worth, which, generally, is above the

house’s buy value. In these circumstances, the client can finance closing prices.

For instance, say you make

a suggestion on a house for $200,000. The lender’s official appraisal report states

the house is value $205,000.

The client can open a USDA mortgage

for the complete worth, so long as the surplus funds are utilized to closing costs such because the title report and mortgage

origination charges.

Extra funds may even be used

to prepay property taxes and home-owner’s insurance coverage.

So, ultimately, USDA

debtors might get into a house with near nothing out of pocket.

With FHA, the house purchaser should

give you a 3.5% down fee plus closing prices. FHA has no guideline stating

that the mortgage quantity can exceed the acquisition value.

The one solution to get a zero out-of-pocket mortgage with FHA is to get a considerable down payment gift, down payment assistance, or seller contributions for closing prices.

USDA is extra versatile, so

consumers with little money on-hand ought to look into this selection first.

USDA con: You need to purchase in a ‘rural’

location

USDA eligibility relies on

the placement of the house. You need to buy a property in a rural space as

outlined by the USDA.

However the definition of “rural”

is sort of liberal, and based mostly on U.S. census data from greater than 15 years

in the past. So many suburban areas are nonetheless eligible.

USDA publishes online maps consumers can use to test the eligibility of a sure deal with or geographical space. Patrons will discover that some complete states are USDA-eligible. Even extremely populated states include surprisingly huge qualifying areas.

An estimated 97% of the

American panorama is geographically eligible for a USDA mortgage.

Nonetheless, some consumers would possibly discover that eligible areas are too far outdoors employment facilities, and for that motive select an FHA loan, which comes with no geographical restrictions.

USDA con: Revenue limits apply

The Rural Improvement mortgage was created to spur homeownership in

rural areas, particularly amongst low-income and moderate-income house

consumers who may not in any other case qualify.

As such, USDA publishes revenue limits. Maximums are set at 115%

of the median revenue to your county or space. However, these limits aren’t overly

restrictive.

The next are examples of most family

incomes in varied locales across the nation.

- Denver, Colorado: $112,850

- Portland, Oregon: $105,950

- Philadelphia, Pennsylvania: $111,100

- Albany County, Wyoming: $92,450

You’ll find present USDA revenue limits to your space here.

Not everybody will fall inside USDA revenue limits. That’s the place

FHA is available in. FHA loans include completely no revenue limits for its customary

program.

Check your zero-down USDA loan eligibility (Mar 18th, 2021)

FHA mortgage

professionals and cons

Whereas USDA loans stand out for being ultra-affordable, many

debtors want an FHA mortgage for its looser underwriting necessities.

There aren’t any revenue limits once you apply for an FHA mortgage, and also you

would possibly have the ability to get away with a decrease credit score rating and better money owed than USDA

or standard lenders would enable.

Right here’s what you need to know.

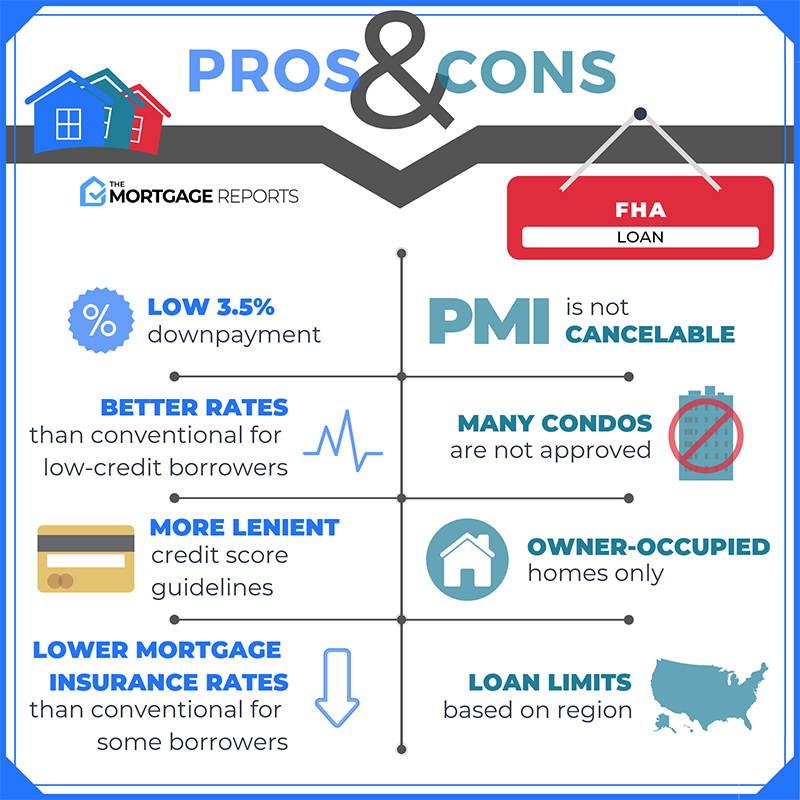

FHA professional: Versatile credit score necessities

One of many largest advantages of the FHA mortgage program is its low

credit score rating threshold. Most FHA lenders will settle for credit score scores as little as

580 with simply 3.5% down. That’s a far cry from USDA’s 640 credit score minimal.

The Federal Housing Administration will even enable FICO scores of

500-579. Nonetheless, you’ll have to make a ten% down fee — and few lenders will

truly approve scores this low.

FHA tends to be versatile in relation to credit score historical past, too.

For instance, FHA tips particularly state that lack of credit history just isn’t a motive to disclaim somebody’s mortgage.

In case you have little or no data in your credit score report — or none

in any respect — since you haven’t borrowed a lot up to now, an FHA mortgage continues to be an

choice. You’ll simply must show your monetary accountability in one other method,

for instance, with a 12-month historical past of on-time lease funds.

USDA has comparable guidelines, however it is perhaps tougher to discover a USDA lender

to approve you. With the FHA program, lenient credit score necessities are the norm.

FHA professional: Versatile debt-to-income ratios

FHA can be extra versatile than USDA in relation to debt-to-income ratios (DTIs).

Your debt-to-income ratio compares your month-to-month

debt funds and gross month-to-month revenue. Lenders use this quantity to find out

how a lot of your revenue is taken up by current money owed, and the way a lot room is

left over in your price range for month-to-month mortgage funds.

Though the U.S. Division of Agriculture doesn’t set mortgage limits,

its revenue limits successfully cap the quantity you’ll be able to borrow.

For example, in case your month-to-month pre-tax revenue is $4,000 and also you

pay $600 per thirty days towards scholar loans and bank cards, your current DTI is

15 p.c.

USDA’s most DTI — together with housing funds — is usually

41 p.c. So essentially the most you’ll be able to spend in your mortgage every month is $1,040.

- $600

+ $1,040 = $1,640 - $1,640

/ $4,000 = 0.41 - DTI =

41%

The USDA usually limits debt-to-income ratios to 41%, besides

when the borrower has a credit score rating over 660, secure employment, or can present a

demonstrated skill to save lots of.

These mortgage utility strengths are sometimes called “compensating factors” and might play a giant

position in getting authorised for any mortgage — not simply USDA.

FHA, alternatively, typically permits a DTI of as much as 45 with none compensating

elements. Within the instance above, a forty five p.c DTI allowance raises your most

mortgage fee to $1,300.

A much bigger month-to-month fee will increase the quantity you’ll be able to borrow. That

means you’ll be able to probably purchase a greater, costlier house.

If current money owed are a problem for you, you might need to select an

FHA mortgage over a USDA mortgage for its flexibility on this space.

FHA con: Increased mortgage insurance coverage charges

The principle draw back to FHA financing is paying mortgage insurance coverage

premiums (MIP).

Each FHA and USDA loans cost debtors mortgage insurance coverage. So do

standard loans, when consumers put lower than 20% down. (This is named

personal mortgage insurance coverage or ‘PMI.’) All three sorts of mortgage insurance coverage defend

the lender in case of foreclosures.

USDA’s mortgage insurance coverage charges are usually the most cost effective of the

three.

FHA loans are recognized for having costlier mortgage insurance coverage —

though, standard PMI charges would possibly truly be greater you probably have a decrease

credit score rating and small down fee.

Check out how mortgage insurance coverage prices would possibly evaluate for a

$250,000 house with 3.5% down. The borrower on this state of affairs has a 640 credit score

rating.

| USDA Mortgage Insurance coverage (MI) | FHA Mortgage Insurance coverage Premium (MIP) | Typical Non-public Mortgage Insurance coverage (PMI) | |

| Upfront Price (% of mortgage quantity) | 1.0% | 1.75% | None |

| Upfront Price ($) | $2,400 | $4,200 | $0 |

| Annual Price (% of mortgage quantity) | 0.35% | 0.85% | 1.65% |

| Month-to-month Fee (annual fee / 12) | $70 / month | $170 / month | $330 / month |

Just a few issues to notice right here:

- Upfront mortgage insurance coverage premiums for USDA and FHA will be rolled

into the mortgage quantity - The annual FHA MIP fee drops to 0.80% in the event you put not less than 5% down

- Typical PMI charges can drop steeply when you could have the next

credit score rating

The opposite large distinction in relation to mortgage insurance coverage is that

standard PMI will be canceled as soon as a home-owner has not less than 20% fairness.

Against this, USDA mortgage insurance coverage lasts the lifetime of the mortgage. So

does FHA mortgage insurance coverage, except you set not less than 10% down. In that case,

MIP lasts 11 years.

Whereas this would possibly look like a deal-breaker, even owners with

‘everlasting’ mortgage insurance coverage aren’t caught with it perpetually. These with FHA and

USDA loans might be able to refinance into a standard mortgage with no PMI as soon as

they attain 20% fairness within the house, because of the mortgage stability dropping or the house

worth rising, or each.

So, you probably have a credit score rating within the low 600s and PMI charges would

be tremendous excessive, don’t let the truth that PMI is cancelable sway you. An FHA or

USDA mortgage might nonetheless be cheaper in the long term.

Check your FHA loan eligibility (Mar 18th, 2021)

Evaluate USDA and

FHA mortgage charges

There’s yet one more large advantage of utilizing both a USDA or FHA mortgage. Each have below-market mortgage charges, that means you’re prone to get a decrease rate of interest than you’ll with a standard mortgage.

Immediately’s charges are at historic lows, so it’s a good time to lock an

inexpensive fastened fee through the FHA or USDA program. Examine your mortgage choices

to see which one works greatest for you.

[ad_2]

Source link

{kind=link}