[ad_1]

The VA residence mortgage: Unbeatable advantages for veterans

For a lot of who qualify, the VA mortgage program is the absolute best mortgage.

Backed by the U.S. Division of Veterans Affairs, VA loans are designed to assist active-duty army personnel, veterans and sure different teams turn into householders at an inexpensive value.

The VA mortgage asks for no down fee, requires no mortgage insurance coverage, and has lenient guidelines about qualifying, amongst many different benefits.

Right here’s every part you could learn about qualifying for and utilizing a VA mortgage.

Verify your VA loan eligibility. Start here (Nov 3rd, 2021)

On this article (Skip to…)

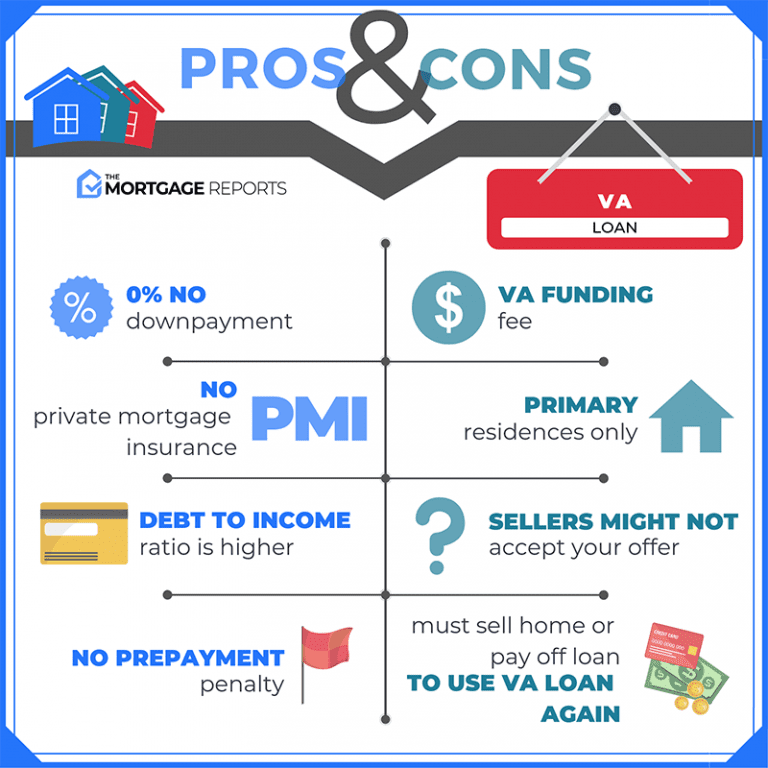

Prime 10 VA mortgage advantages

1. No down fee on a VA mortgage

Most residence mortgage applications require you to make at the least a small down fee to purchase a house. The VA residence mortgage is an exception.

Quite than paying 5%, 10%, 20% or extra of the house’s buy worth upfront in money, with a VA mortgage you possibly can finance as much as 100% of the acquisition worth.

The VA mortgage is a real no-money-down residence mortgage alternative.

2. No mortgage insurance coverage for VA loans

Sometimes, lenders require you to pay for mortgage insurance coverage for those who make a down fee that’s lower than 20%.

This insurance coverage — which is named personal mortgage insurance coverage (PMI) for a traditional mortgage and a mortgage insurance coverage premium (MIP) for an FHA loan — would shield the lender for those who defaulted in your mortgage.

VA loans require neither a down fee nor mortgage insurance coverage. That makes a VA-backed mortgage very inexpensive upfront and over time.

3. VA loans have a authorities assure

There’s a purpose why the VA mortgage comes with such favorable phrases.

The federal authorities ensures these loans — that means a portion of the mortgage quantity might be repaid to the lender even for those who’re unable to make month-to-month funds for no matter purpose.

This assure encourages and permits personal lenders to supply VA loans with exceptionally engaging phrases.

Verify your VA loan eligibility. Start here (Nov 3rd, 2021)

4. You may store for the perfect VA mortgage charges

VA loans are neither originated nor funded by the VA. They don’t seem to be direct loans from the federal government. Moreover, mortgage charges for VA loans aren’t set by the VA itself.

As a substitute, VA loans are supplied by U.S. banks, savings-and-loans establishments, credit score unions, and mortgage lenders — every of which units its personal VA mortgage charges and costs.

This implies you possibly can store round and examine mortgage presents and nonetheless select the VA mortgage that works greatest on your finances.

5. VA loans don’t enable a prepayment penalty

A VA mortgage gained’t limit your proper to promote the property partway by way of your mortgage time period.

There’s no prepayment penalty or early-exit charge regardless of inside what time-frame you resolve to promote your private home.

Moreover, there aren’t any restrictions relating to a refinance of your VA mortgage.

You may refinance your existing VA loan into one other VA mortgage by way of the company’s Curiosity Price Discount Refinance Mortgage (IRRRL) program, or change right into a non-VA mortgage at any time.

6. VA mortgages are available many sorts

A VA mortgage can have a hard and fast price or an adjustable price. As well as, you need to use a VA mortgage to purchase a home, condominium, new-built residence, manufactured residence, duplex, or different sorts of properties.

Or, it may be used for refinancing your present mortgage, making repairs or enhancements to your private home, or making your private home extra energy-efficient.

The selection is yours. A VA-approved lender may also help you resolve.

Verify your VA loan eligibility. Start here (Nov 3rd, 2021)

7. It’s simpler to qualify for VA loans

Like all mortgage varieties, VA loans require particular documentation, an appropriate credit score historical past, and ample earnings to make your month-to-month funds.

However, in comparison with different mortgage applications, VA mortgage pointers are typically extra versatile. That is made potential due to the VA mortgage assure.

The Division of Veterans Affairs genuinely needs to make the mortgage course of simpler for army members, veterans, and qualifying army spouses to purchase or refinance a house.

8. VA mortgage closing prices are decrease

The VA limits the closing prices lenders can cost to VA mortgage candidates. That is one other method {that a} VA mortgage may be extra inexpensive than different sorts of loans.

Cash saved on closing prices can be utilized for furnishings, shifting prices, residence enhancements, or the rest.

9. The VA presents funding charge flexibility

VA loans require a “funding charge,” an upfront value primarily based in your mortgage quantity, your kind of eligible service, your down fee measurement, and different components.

Funding charges don’t must be paid in money, although. The VA permits the charge to be financed with the mortgage, so nothing is due at closing.

And, not all VA debtors can pay it. VA funding charges are usually waived for veterans who obtain VA incapacity compensation and for single surviving spouses of veterans who died in service or because of a service-connected incapacity.

10. VA loans are assumable

Most VA loans are “assumable,” which suggests you possibly can switch your VA mortgage to a future residence purchaser if that individual can be VA-eligible.

Assumable loans is usually a large profit whenever you promote your private home — particularly in a rising mortgage price setting.

If your private home mortgage has as we speak’s low price and market charges rise sooner or later, the idea options of your VA turn into much more helpful.

VA mortgage charges

The VA mortgage is seen as one of many lowest-risk mortgage varieties accessible available on the market.

This security permits banks to lend to veteran debtors at decrease rates of interest.

In the present day’s VA mortgage charges*

| Mortgage Kind | Present Mortgage Price |

| VA 30-year FRM | 2.375% (2.547% APR) |

| Typical 30-year FRM | 3.125% (3.125% APR) |

| VA 15-year FRM | 2.25% (2.571% APR) |

| Typical 15-year FRM | 2.625% (2.625% APR) |

*Present charges supplied day by day by companions of the Mortgage Reviews. See our loan assumptions here.

VA charges are greater than 25 foundation factors (0.25%) decrease than standard charges on common, based on knowledge collected by mortgage software program firm Ellie Mae.

Most mortgage applications require greater down fee and credit score scores than the VA residence mortgage. Within the open market, a VA mortgage ought to carry a better price because of extra lenient lending pointers and better perceived threat.

But the results of the Veterans Affairs efforts to maintain veterans of their houses means decrease threat for banks and decrease borrowing prices for eligible veterans.

Find and lock a low VA loan rate today. Start here (Nov 3rd, 2021)

VA mortgage calculator

Eligibility

Am I eligible for a VA residence mortgage?

Opposite to in style perception, VA loans can be found not solely to veterans, but in addition to different lessons of army members.

The record of eligible VA borrowers consists of:

- Energetic-duty service members

- Members of the Nationwide Guard

- Reservists

- Surviving spouses of veterans

- Cadets on the U.S. Navy, Air Drive or Coast Guard Academy

- Midshipmen on the U.S. Naval Academy

- Officers on the Nationwide Oceanic & Atmospheric Administration.

A minimal time period of service is usually required.

Minimal service required for a VA mortgage

VA residence loans can be found to active-duty service members, veterans (until dishonorably discharged), and in some circumstances, surviving relations.

To be eligible, you could meet certainly one of these service necessities:

- You’ve served 181 days of lively responsibility throughout peacetime

- You’ve served 90 days of lively responsibility throughout wartime

- You’ve served six years within the Reserves or Nationwide Guard

- Your partner was killed within the line of responsibility and you haven’t remarried

Your eligibility for the VA residence mortgage program by no means expires.

Veterans who earned their VA entitlement way back are nonetheless utilizing their profit to purchase houses.

Verify your VA home loan eligibility. Start here (Nov 3rd, 2021)

The VA mortgage Certificates of Eligibility (COE)

What’s a COE?

With a purpose to present a mortgage firm you might be VA-eligible, you’ll want a Certificates of Eligibility (COE). Your lender can purchase one for you on-line, normally in a matter of seconds.

How you can get your COE (Certificates of Eligibility)

Getting a Certificates of Eligibility (COE) could be very simple most often. Merely have your lender order the COE by way of the VA’s automated system. Any VA-approved lender can do that.

Alternatively, you possibly can order your certificates your self by way of the VA advantages portal.

If the web system is unable to situation your COE, you’ll want to supply your DD-214 kind to your lender or the VA.

Does a COE imply you might be assured a VA mortgage?

No, having a Certificates of Eligibility (COE) doesn’t assure a VA mortgage approval.

Your COE exhibits the lender you’re eligible for a VA mortgage, however nobody is assured VA mortgage approval.

You could nonetheless qualify for the mortgage primarily based on VA mortgage pointers. The assure a part of the VA mortgage refers back to the VA’s promise to the lender of compensation if the borrower defaults.

Qualifying for a VA mortgage

VA mortgage eligibility vs. qualification

Being eligible for VA residence mortgage advantages primarily based in your army standing or affiliation doesn’t essentially imply you’ll qualify for a VA mortgage.

You continue to need to qualify for a VA mortgage primarily based in your credit score, debt, and earnings.

Minimal credit score rating for a VA mortgage

The VA has established no minimal credit score rating for a VA mortgage.

Nonetheless, many VA mortgage lenders require minimal FICO scores of 620 or greater — so apply with many lenders in case your credit score rating is perhaps a problem.

Even VA lenders that enable decrease credit score scores don’t settle for subprime credit score.

VA underwriting pointers state that candidates will need to have paid their obligations on time for at the least the latest 12 months to be thought of passable credit score dangers.

As well as, the VA normally requires a two-year ready interval following a Chapter 7 chapter or foreclosures earlier than it’ll insure a mortgage.

Debtors in Chapter 13 will need to have made at the least 12 on-time funds and safe the approval of the chapter court docket.

Verify your VA loan home buying eligibility. Start here (Nov 3rd, 2021)

VA mortgage debt-to-income ratios

The connection of your money owed and your earnings known as your debt-to-income ratio, or DTI.

VA underwriters divide your month-to-month money owed (automobile funds, bank cards, and different accounts, plus your proposed housing expense) by your gross (before-tax) earnings to give you your debt-to-income ratio.

As an illustration:

- In case your gross earnings is $4,000 per thirty days

- And your whole month-to-month debt is $1,500 (together with the brand new mortgage, property taxes and householders insurance coverage, plus different debt funds)

- Then your DTI is 37.5% (1500/4000=0.375)

A DTI over 41% means the lender has to use further formulation to see for those who qualify below residual earnings pointers.

VA residual earnings guidelines

VA underwriters carry out further calculations that may have an effect on your mortgage approval.

Factoring in your estimated month-to-month utilities, your estimated taxes on earnings, and the world of the nation by which you reside, the VA arrives at a determine which represents your “true” prices of residing.

It then subtracts that determine out of your earnings to search out your residual income (e.g. your cash “left over” every month).

Consider the residual earnings calculation as a real-world simulation of your residing bills.

It’s the VA’s greatest effort to make sure that army households have a stress-free homeownership expertise.

Right here is an instance of how residual earnings works, assuming a household of 4 which is buying a 2,000 square-foot residence on a $5,000 month-to-month earnings.

- Future home fee, plus different debt funds: $2,500

- Month-to-month estimated earnings taxes: $1,000

- Month-to-month estimated utilities at $0.14 per sq. foot: $280

This leaves a residual earnings calculation of $1,220.

Now, examine that residual earnings to VA residual income requirements for a household of 4:

- Northeast Area: $1,025

- Midwest Area: $1,003

- South Area: $1,003

- West Area: $1,117

The borrower in our instance exceeds VA’s residual earnings requirements in all components of the nation.

Subsequently, regardless of the borrower’s debt-to-income ratio of fifty%, the borrower may get accredited for a VA mortgage.

Qualifying for a VA mortgage with part-time earnings

You may qualify for this sort of financing even you probably have a part-time job or a number of jobs.

You could present a 2-year historical past of constructing constant part-time earnings, and stability within the variety of hours labored. The lender will be sure any earnings obtained seems secure. See our full guide to getting a mortgage when you’re self-employed or work part-time.

Find out if you qualify for a VA loan. Start here (Nov 3rd, 2021)

VA funding charges and mortgage limits

In regards to the VA funding charge

The VA fees an upfront charge to defray the prices of this system and make it sustainable for the long run.

Veterans pay a lump sum that varies relying on the mortgage goal and down fee quantity.

The charge is generally wrapped into the mortgage. It doesn’t add to the money wanted to shut the mortgage.

VA residence buy funding charges

| Kind of Navy Service | Down Cost | Charge for First-Time Use | Fee for Subsequent Use |

| Energetic Responsibility, Reserves, and Nationwide Guard | None | 2.3% | 3.6% |

| 5% or extra | 1.65% | 1.65% | |

| 10% or extra | 1.4% | 1.4% |

VA cash-out refinance funding charges

| Kind of Navy Service | Charge for First-Time Use | Charge for Subsequent Makes use of |

| Energetic Responsibility, Reserves, and Nationwide Guard | 2.3% | 3.6% |

VA streamline refinances (IRRRL) & assumptions

| Kind of Navy Service | Charge for First-Time Use | Charge for Subsequent Makes use of |

| Energetic Responsibility, Reserves, and Nationwide Guard | 0.5% | 0.5% |

Manufactured residence loans not completely affixed

| Kind of Navy Service | Charge for First-Time Use | Charge for Subsequent Makes use of |

| Energetic Responsibility, Reserves, and Nationwide Guard | 1.0% | 1.0% |

VA mortgage limits in 2021

VA mortgage limits have been repealed,

due to the Blue Water Navy Vietnam Veterans Act of 2019.

There is no such thing as a

most quantity for which a house purchaser can obtain a VA mortgage, at the least so far as the

VA is anxious.

Nonetheless, personal lenders could set their very own limits. So examine along with your lender in case you are searching for a VA mortgage above native conforming loan limits.

Verify your VA loan eligibility. Start here (Nov 3rd, 2021)

Eligible property varieties

Homes you should purchase with a VA mortgage

VA mortgages are versatile about what sorts of property you possibly can and might’t buy. A VA mortgage can be utilized to purchase a:

- Indifferent home

- Apartment

- New-built residence

- Manufactured residence

- Duplex, triplex or four-unit property

You too can use a VA mortgage to refinance an present mortgage for any of these sorts of properties.

VA loans and second houses

Federal rules restrict loans assured by the Division of Veterans Affairs to “major residences” solely.

Nonetheless, “major residence” is outlined as the house by which you reside “many of the 12 months.”

Subsequently, for those who personal an out-of-state residence by which you reside for greater than six months of the 12 months, this different residence, whether or not it’s your trip residence or retirement property, turns into your official “major residence.”

Because of this, VA loans are in style amongst getting older army debtors.

Shopping for a multi-unit residence with a VA mortgage

VA loans let you purchase a duplex, triplex, or four-plex with 100% financing. You could reside in one of many items.

Shopping for a house with multiple unit may be difficult.

Mortgage lenders think about these properties riskier to finance than conventional, single-family residences, so that you’ll must be a stronger borrower.

VA underwriters should be sure you should have sufficient emergency financial savings, or money reserves, after closing on your own home. That’s to make sure you’ll have cash to pay your mortgage even when a tenant fails to pay lease or strikes out.

The minimal money reserves wanted after closing is six months of mortgage funds (masking principal, curiosity, taxes, and insurance coverage – PITI).

Your lender may even need to learn about earlier landlord expertise you’ve had, or any expertise with property upkeep or renting.

For those who don’t have any, you might be able to sidestep that situation by hiring a property administration firm. However that’s as much as the person lender.

Your lender will take a look at the earnings (or potential earnings) of the rental items, utilizing both present rental agreements or an appraiser’s opinion of what the items ought to fetch.

They’ll normally take 75% of that quantity to offset your mortgage fee when calculating your month-to-month bills.

VA loans and rental properties

You can’t use a VA mortgage to purchase a rental property. You may, nonetheless, use a VA mortgage to refinance an present rental residence you as soon as occupied as a major residence.

For residence purchases, with the intention to acquire a VA mortgage, you have to certify that you simply intend to occupy the house as your principal residence.

If the property is a duplex, triplex, or four-unit condo constructing, you have to occupy one of many items your self. Then you possibly can lease out the opposite items.

The exception to this rule is the VA’s Curiosity Price Discount Refinance Mortgage (IRRRL).

This mortgage, also called the VA Streamline Refinance, can be utilized for refinancing an present VA mortgage on a house the place you at present reside or the place you used to reside, however not do.

Check your VA IRRRL eligibility. Start here (Nov 3rd, 2021)

Shopping for a condominium with a VA mortgage

The VA maintains a listing of accredited condominium initiatives inside which you’ll buy a unit with a VA mortgage.

At VA’s website, you possibly can seek for the hundreds of accredited condominium complexes throughout the U.S.

In case you are VA-eligible and out there for a condominium, be sure the unit you’re concerned with is accredited.

As a purchaser, you might be in all probability not capable of get the advanced VA-approved. That’s as much as the administration firm or house owner’s affiliation.

If a condominium you want is just not accredited, you have to use different financing like an FHA or standard mortgage or discover one other property.

Word that the condominium should meet FHA or standard pointers if you wish to use these sorts of financing.

Veteran mortgage aid with the VA mortgage

The U.S. Division of Veterans Affairs, or VA, supplies residence retention help. The VA intervenes when a veteran is having bother making residence mortgage funds.

The VA works with mortgage servicers to supply mortgage choices to the veteran, aside from foreclosures.

In fiscal 12 months 2019, the VA revamped 400,000 contact actions to succeed in debtors and mortgage servicers. The intent was to work out a mutually agreeable compensation choice for each events.

Greater than 100,000 veteran householders prevented foreclosures in 2019 alone due to this effort.

The initiative has saved the taxpayer an estimated $2.6 billion. Extra importantly, huge numbers of veterans and army households acquired one other probability at homeownership.

Verify your VA loan eligibility. Start here (Nov 3rd, 2021)

When NOT to make use of a VA mortgage

In case you have good credit score and 20% down

A major benefit to VA residence loans is the dearth of mortgage insurance coverage.

Nonetheless, the VA assure doesn’t come freed from cost. Debtors pay an upfront funding fee, which they normally select so as to add to their mortgage quantity.

The charge ranges from 1.4% to three.6%, relying on the down fee share and whether or not the house purchaser has beforehand used his or her VA mortgage eligibility. The commonest charge is 2.3%.

On a $200,000 buy, a 2.3% charge equals $4,600.

Nonetheless, consumers who select a traditional mortgage and put 20% down get to keep away from mortgage insurance coverage and the upfront charge. For these army residence consumers, the VA funding charge is perhaps an pointless expense.

The exception: Mortgage candidates whose credit standing or earnings meets VA pointers however not these of standard mortgages should go for VA.

For those who’re on the “CAIVRS” record

To qualify for a VA mortgage, you have to show you may have made good on earlier government-backed money owed and that you’ve got paid taxes.

The Credit score Alert Verification Reporting System, or “CAIVRS,” is a database of shoppers who’ve defaulted on authorities obligations. These people aren’t eligible for the VA residence mortgage program.

In case you have a non-veteran co-borrower

Veterans usually apply to buy a home with a non-veteran who is just not their partner.

That is okay. Nonetheless, it won’t be their most suitable option.

Because the veteran, your earnings should cowl your half of the mortgage fee. The non-veteran’s earnings can’t be used to compensate for the veteran’s inadequate earnings.

Plus, when a non-veteran owns half the mortgage, the VA ensures solely half that quantity. The lender would require a 12.5% down fee for the non-guaranteed portion.

The Typical 97 mortgage, however, permits down funds as little as 3%.

One other low-down-payment mortgage choice is the FHA residence mortgage, for which 3.5% down is appropriate.

The USDA residence mortgage additionally requires zero down fee and presents related charges to VA loans. Nonetheless, the property have to be inside USDA-eligible areas.

For those who plan to borrow with a non-veteran, certainly one of these mortgage varieties is perhaps your better option.

Explore your mortgage options. Start here (Nov 3rd, 2021)

For those who apply with a credit-challenged partner

In states with neighborhood property legal guidelines, VA lenders should think about the credit standing and monetary obligations of your partner. This rule applies even when she or he is not going to be on the house’s title and even on the mortgage.

Such states are as follows.

- Arizona

- California

- Idaho

- Louisiana

- Nevada

- New Mexico

- Texas

- Washington

- Wisconsin

A partner with less-than-perfect credit score or who owes alimony, baby help, or different upkeep could make your VA approval more difficult.

Apply for a traditional mortgage for those who qualify for the mortgage by your self. The partner’s monetary historical past and standing needn’t be thought of if she or he is just not on the mortgage utility.

Verify your VA loan home buying eligibility. Start here (Nov 3rd, 2021)

If you wish to purchase a trip residence or funding property

The aim of VA financing is to assist veterans and active-duty service members purchase and reside in their very own residence. This mortgage is just not meant to construct actual property portfolios.

These loans are for major residences solely, so if you’d like a ski cabin or rental, you’ll need to get a traditional mortgage.

If you wish to buy a high-end residence

Beginning January 2020, there aren’t any limits to the scale of mortgage a lender can approve.

Nonetheless, lenders could set up their very own limits for VA loans, so examine along with your lender earlier than making use of for a big VA mortgage.

Spouses and the VA mortgage program

What spouses are eligible for a VA mortgage?

What if the service member passes away earlier than she or he makes use of the profit? Eligibility passes to an unremarried partner, in lots of circumstances.

For the surviving partner to be eligible, the deceased service member will need to have:

- Died within the line of responsibility

- Handed away because of a service-connected incapacity

- Been lacking in motion, or a prisoner of battle, for at the least 90 days

- Been a completely disabled veteran for at the least 10 years previous to dying, and died from any trigger

Additionally eligible are remarried spouses who married after the age of 57, on or after December 16, 2003.

In these circumstances, the surviving partner can use VA mortgage eligibility to purchase a house with zero down fee, simply because the veteran would have.

VA mortgage advantages for surviving spouses

Surviving spouses have an extra VA mortgage profit, nonetheless. They’re exempt from the VA funding charge. Consequently, their mortgage stability and month-to-month fee might be decrease.

Surviving spouses are additionally eligible for a VA streamline refinance once they meet the next pointers.

- The surviving partner was married to the veteran on the time of dying

- The surviving partner was on the unique VA mortgage

VA streamline refinancing is usually not accessible when the deceased veteran was the one applicant on the unique VA mortgage, even when she or he acquired married after shopping for the house.

On this case, the surviving partner would want to qualify for a non-VA refinance, or a VA cash-out mortgage.

A cash-out mortgage by way of VA requires the army partner to satisfy residence buy eligibility necessities.

If that is so, the surviving partner can faucet into the house’s fairness to lift money for any goal, and even repay an FHA or standard mortgage to eradicate mortgage insurance coverage.

Verify your VA loan home buying eligibility. Start here (Nov 3rd, 2021)

Qualifying for those who obtain (or pay) baby help or alimony

Shopping for a house after a divorce is not any simple activity.

If, previous to your divorce, you lived in a two-income family, you now have much less spending energy and a diminished month-to-month earnings for functions of your VA residence mortgage utility.

With much less earnings, it may be tougher to satisfy each the VA House Mortgage Warranty’s debt-to-income (DTI) pointers and the VA residual earnings requirement on your space.

Receiving alimony or baby help can counteract a lack of earnings.

Mortgage lenders is not going to require you to supply details about your divorce settlement’s alimony or baby help phrases, however for those who’re keen to reveal, it may well depend towards qualifying for a house mortgage.

Totally different VA-approved lenders will deal with alimony and baby help earnings otherwise.

Sometimes, you’ll be requested to supply a duplicate of your divorce settlement or different court docket paperwork to help the alimony and baby help funds.

Lenders will then need to see that the funds are secure, dependable, and prone to proceed for one more 36 months, at the least.

You may additionally be requested to point out proof that alimony and baby help funds have been made previously reliably, in order that the lender could use the earnings as a part of your VA mortgage utility.

In case you are the payor of alimony and baby help funds, your debt-to-income ratio may be harmed.

Not solely would possibly you be shedding the second earnings of your dual-income households, however you’re making further funds that depend in opposition to your outflows.

VA mortgage lenders make cautious calculations with respect to such funds.

You may nonetheless get accredited for a VA mortgage whereas making such funds — it’s simply harder to point out ample month-to-month earnings.

Verify your VA loan eligibility. Start here (Nov 3rd, 2021)

VA mortgage assumption

What’s VA mortgage assumption?

One profit for residence consumers is that VA loans are assumable. Once you assume a mortgage mortgage, you’re taking over the present house owner’s month-to-month fee.

That may very well be an enormous benefit if mortgage charges have risen because the authentic proprietor bought the house. The client would have the ability to purchase a low-rate, inexpensive mortgage — and it may make it simpler for the vendor to discover a keen purchaser in a tricky market.

VA mortgage assumption financial savings

Shopping for a house by way of an assumable mortgage mortgage is much more interesting when rates of interest are on the rise.

For instance:

- Say a seller-financed $200,000 for his or her residence in 2013 at an rate of interest of three.25% on a 30-year fastened mortgage

- Utilizing this situation, their principal and curiosity fee could be $898 per thirty days

- Let’s assume present 30-year fastened charges averaged 4.10%

- For those who financed $200,000 at 4.10% for a 30-year mortgage time period, your month-to-month principal and curiosity fee could be $966 per thirty days

Moreover, as a result of the vendor has already paid 4 years into the mortgage time period, they’ve already paid almost $25,000 in curiosity on the mortgage.

By assuming the mortgage, you’ll save $34,560 over the 30-year mortgage as a result of distinction in rates of interest. You’d additionally save roughly $25,000 due to the curiosity already paid by the sellers.

That comes out to a complete financial savings of just about $60,000!

Verify your VA home loan eligibility. Start here (Nov 3rd, 2021)

How you can assume (tackle) a VA mortgage

There are at present two methods to imagine a VA mortgage.

- The brand new purchaser is a professional veteran who “substitutes” his or her VA eligibility for the eligibility of the vendor

- The brand new residence purchaser qualifies by way of VA requirements for the mortgage fee. That is the most secure methodology for the vendor because it permits the mortgage to be assumed understanding that the brand new purchaser is chargeable for the mortgage, and the vendor is not chargeable for the mortgage

The lender and/or the VA must approve a mortgage assumption.

Loans serviced by a lender with automated authority could course of assumptions with out sending them to a VA Regional Mortgage Middle.

For lenders with out automated authority, the mortgage have to be despatched to the suitable VA Regional Mortgage Middle for approval. This mortgage course of will usually take a number of weeks.

When VA loans are assumed, it’s the servicer’s accountability to verify the house owner who assumes the property meets each VA and lender necessities.

VA mortgage assumption necessities

For a VA mortgage assumption to happen, the next situations have to be met:

- The present mortgage have to be present. If not, any overdue quantities have to be paid at or earlier than closing

- The client should qualify primarily based on VA credit score and earnings requirements

- The client should assume all mortgage obligations, together with compensation to the VA if the mortgage goes into default

- The unique proprietor or new proprietor should pay a funding charge of 0.5% of the prevailing principal mortgage stability

- A processing charge have to be paid prematurely, together with an inexpensive estimate for the price of the credit score report

Discovering assumable VA loans

There are a number of methods for residence consumers to search out an assumable VA mortgage.

Consider it or not, print media remains to be alive and nicely. Some residence sellers promote their assumable residence on the market within the newspaper, or in a neighborhood actual property publication.

There are a variety of on-line assets for locating assumable mortgage loans.

Web sites like TakeList.com and Zumption.com give householders a option to showcase their properties to residence consumers seeking to assume a mortgage.

With the assistance of the A number of Itemizing Service (MLS), actual property brokers stay an incredible useful resource for residence consumers.

This is applicable to residence consumers particularly looking for assumable VA loans as nicely.

How do I apply for a VA mortgage?

You may simply and shortly have a lender pull your certificates of eligibility (COE) to be sure to’re capable of get a VA mortgage.

Most mortgage lenders provide VA residence loans. So that you’re free to buy and examine charges with nearly any firm that catches your eye.

Getting a VA mortgage on your new residence is comparable in some ways to securing every other buy mortgage. As soon as you discover a really perfect residence in your worth vary, you make a purchase order provide, after which endure VA appraisal and underwriting.

VA appraisal ensures that the house meets its minimal property necessities (MPRs) and is structurally sound and protected for occupancy.

What’s extra, VA-specific mortgage lenders are literally a number of the highest-rated (and lowest-priced) available on the market. Listed below are a couple of we’d advocate trying out.

[ad_2]

Source link

{kind=link}