[ad_1]

VA mortgage charges right this moment

VA mortgage charges are the bottom of any main mortgage program on common.

How low are they?

Right now’s 30–yr mounted VA mortgage rates of interest begin at % (% APR), in line with our lender community. Evaluate that to % (% APR) for a standard mortgage.

Your charge may differ, however VA loans can be found at low charges even to these with no excellent credit score historical past.

Check your VA loan rate. Start here (Nov 28th, 2021)

On this article (Skip to…)

Your finest VA mortgage charges proper now

As a result of they’re assured by the Division of Veterans Affairs, VA loans provide completely low charges to eligible service members, veterans, and their spouses.

Consider, your personal charge might be totally different from the charges proven under relying in your credit score rating, down cost, and different components. However in the event you qualify for a VA mortgage, you’re prone to get a decrease charge than comparable debtors with totally different mortgage varieties.

Make sure you store with a minimum of three VA–authorised mortgage lenders to seek out one of the best VA mortgage charge to your scenario.

| Mortgage sort | Right now’s common charges* |

| VA 30-year fixed-rate | % (% APR) |

| Typical 30-year fixed-rate | % (% APR) |

| VA 15-year fixed-rate | % (% APR) |

| Typical 15-year fixed-rate | % (% APR) |

*Common charges assume 0% down and a 740 credit score rating. See our full mortgage VA charge assumptions here.

Lock in your VA loan rate today. Start here (Nov 28th, 2021)

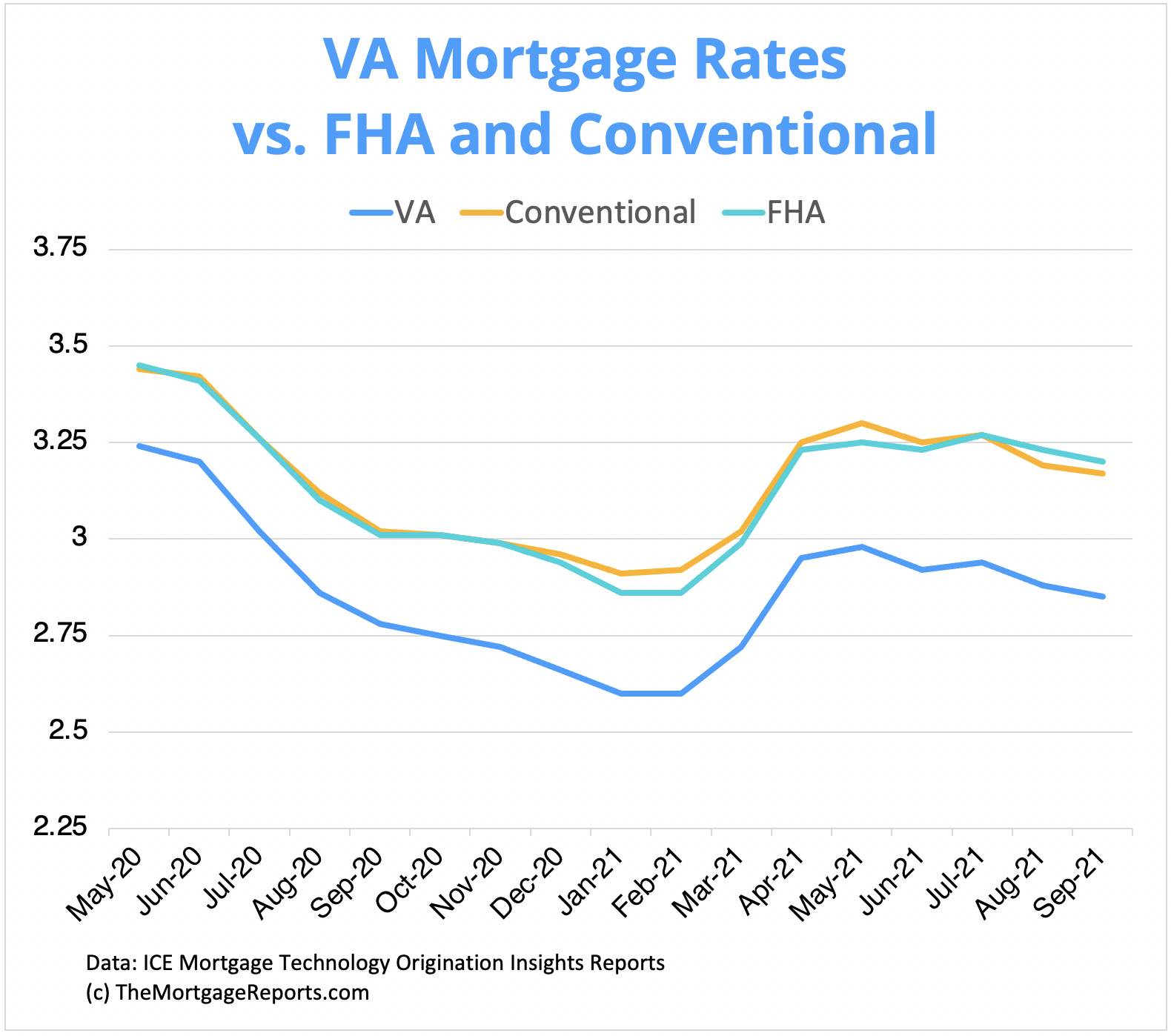

VA mortgage charges beat typical and FHA charges

For years, VA house mortgage charges have undercut these provided by typical and FHA mortgage packages.

As an eligible veteran or lively service member, you’ve got entry to under–common charges, whether or not you’re shopping for or refinancing a house.

Find your lowest VA mortgage rate. Start here (Nov 28th, 2021)

Why are VA rates of interest so ridiculously low?

Robust authorities backing means lenders can provide rock–backside rates of interest with little or no threat. And, they don’t require a down cost or non-public mortgage insurance coverage.

VA mortgage charges provide one of the best worth within the market right this moment, and a unbelievable profit for our nation’s veterans and lively responsibility service members.

Actually? No down cost or PMI?

In addition to decrease rates of interest, VA loans provide two different huge advantages:

- You don’t should put something down when buying a house

- There isn’t a month-to-month mortgage insurance coverage

In case you evaluate a VA mortgage with an FHA mortgage, the no–mortgage–insurance coverage rule alone saves you round $220 per thirty days when shopping for a house value $320,000.

VA mortgage calculator with charges

Curious how a lot your month-to-month mortgage funds could be at right this moment’s VA mortgage charges? Plug in your buy value and charge to seek out out.

How do I discover one of the best VA mortgage charges?

There are actually simply three components that decide your present VA charge. The present market charge, the lender, and also you.

Market charges

Right now’s house patrons and refinancers are in luck. CurrentVA mortgage charges are near the bottom in historical past on the time of this writing.

Debtors in earlier generations couldn’t have imagined 30–yr mounted mortgage charges within the excessive 2s or low 3s, however right this moment they’re not solely a actuality – they’re fairly frequent.

Mortgage lenders

This requires some homework. Don’t settle for the primary VA mortgage charge you’re provided. You don’t know if that’s a great rate of interest till you evaluate it with two or three different lenders.

Name a number of lenders – all on the identical day – and get written quotes. Evaluate the speed and charges. Don’t settle for an extremely–low mortgage charge in trade for 1000’s in closing prices.

Getting a number of mortgage quotes or Mortgage Estimates offers you an opportunity to see which lenders provide one of the best charges in your mortgage mortgage, mixed with the bottom origination charges.

Some lenders, for instance, quote charges primarily based on discount points you’d have to purchase upfront at closing.

Extra about the best way to discover a respected VA lender under.

You: The borrower

Your mortgage profile can have a huge impact in your charge.

Do you’ve got a great credit score rating? Stable earnings? Low debt–to–earnings ratio? You then shouldn’t have any downside getting authorised for low VA mortgage charges.

However if in case you have truthful or poor credit score, count on to obtain the next charge.

Your VA mortgage charge impacts the prices of borrowing. Greater charges imply larger month-to-month mortgage funds and extra curiosity paid over the lifetime of the mortgage.

The excellent news is that VA lenders are lenient on credit score scores, and even a excessive VA mortgage charge might be decrease than a median typical or FHA charge. They name this the “VA house mortgage profit” for a cause!

Check your VA loan rates. Start here (Nov 28th, 2021)

VA house mortgage charges sound superb. Am I eligible?

To get entry to VA house mortgage charges, you must be eligible for the mortgage itself.

You might be possible eligible if in case you have served:

- On lively responsibility between 90 days and two years, relying on service dates

- Within the Nationwide Guard or Reserves for a minimum of six years

You additionally will need to have acquired an different–than–dishonorable discharge.

The easiest way to know in the event you’re eligible is to obtain a Certificates of Eligibility (COE). This isn’t a mortgage approval, however a doc that exhibits lenders you’re eligible for this system.

Most lenders can get a COE for you in minutes, however in the event you really feel extra snug going via the Division of Veterans Affairs itself, you’ll be able to request one through the eBenefits web site.

In both case, it’s possible you’ll want your Type DD214 to show service historical past.

Check your VA loan eligibility. Start here (Nov 28th, 2021)

What’s the minimal VA mortgage credit score rating?

In our survey of top VA lenders, we discovered a large variance in minimal credit score scores for VA loans.

The bottom minimal rating was 550. The best: 620.

The VA doesn’t set a minimal rating itself. It lets the lender set its personal credit score necessities.

In case you’ve been denied attributable to a low rating, store round with totally different mortgage lenders. You may be stunned that you could simply be authorised at one lender however not one other.

Discovering one of the best VA mortgage lenders

VA mortgage charges can differ primarily based on the lender you select.

The lender may also decide the convenience with which you safe the mortgage.

There are a whole bunch of VA lenders throughout the U.S., so how do you decide the fitting one – one with nice charges and repair?

Begin with VA mortgage specialists

Referrals from associates are a great place to begin. Our evaluate of top nationwide VA lenders may assist, too. Select a lender and mortgage officer that does quite a lot of VA loans – you don’t need somebody who’s going to overlook an important step or will get “caught” on a novel side of your mortgage file.

Choose a minimum of two or three prime lenders and get a written quote (ask for a “Loan Estimate“) from all of the lenders on the identical day. Evaluate charges and costs.

Lowest charges or lowest upfront charges?

You’ll have to resolve which is extra vital to you: the bottom charge or the bottom charges. Paying fewer upfront charges normally leads to the next charge.

Or, you’ll be able to select a under–market charge and pay extra upfront for it. This technique ought to repay over the lifetime of the mortgage in the event you keep within the house for many years.

Evaluate mortgage estimates from every lender

No matter your technique, evaluate Mortgage Estimates from every lender. Typically, you should utilize one lender’s quote to negotiate rates or fees from one other lender. You’d be stunned at how a lot room a lender has to change their first quote.

Typically you will get an extremely–low charge and remove many charges, simply by negotiating.

The VA mortgage course of

Your course of will differ primarily based on the kind of VA mortgage you’re in search of.

VA mortgage refinance

If in case you have a VA mortgage and need to scale back your charge, you’ll possible qualify for a VA Interest Rate Reduction Refinance Loan, aka IRRRL.

VA mortgage IRRRL charges are extremely–low, and in the event you final bought or refinanced in the previous couple of years – and even earlier than that – you possibly can possible save rather a lot on curiosity.

You don’t want a house appraisal, earnings documentation, or financial institution statements. The VA says you don’t even want a brand new credit score report (although most lenders will pull one). The primary requirement is that you simply decrease your charge and cost sufficient that it advantages your scenario.

You merely apply with a lender and supply a number of particulars. You don’t should undergo the lender that at present holds your mortgage.

Most likely a number of weeks later, you signal last mortgage paperwork and shut on the brand new mortgage with a decrease charge and cost.

Get today’s low VA IRRRL rates. Start here (Nov 28th, 2021)

VA house buy mortgage

House shopping for with a VA mortgage is much more complicated than getting a VA refinance. Nevertheless it’s effectively value it contemplating right this moment’s low VA rates of interest.

Step one is getting pre–authorised along with your VA lender of selection. With the pre–approval letter, you can also make a suggestion on a house.

When you discover a house, the lender will request an appraisal. Whereas that’s being accomplished, flip in earnings, asset, and credit score paperwork to your lender.

With a clear file, you possibly can be a house owner inside 30–45 days, however longer if in case you have broken credit score or questionable earnings.

For an in–depth take a look at shopping for a house with a VA mortgage, see our guide.

Ought to I get a VA mortgage? I heard the VA funding payment was too costly

Some will let you know to keep away from VA loans due to the VA funding payment. Right here’s what you could find out about VA funding charges:

- 2.3% of the mortgage quantity for first–time VA mortgage customers with zero down

- 3.6% for repeat customers

- 0.5% for streamline refinances

Most house patrons can pay a VA funding payment of $5,750 for a house value of $250,000 with no down cost.

At first, that feels like rather a lot, nevertheless it’s affordable given the advantages of this system.

Most non–VA house patrons should give you a 3% to five% down cost. That’s a minimum of $7,500 on the identical house – an enormous hurdle, particularly for first–time homebuyers.

You’ll be able to wrap the VA funding payment into the mortgage quantity, that means it could possibly nonetheless be a zero–out–of–pocket mortgage. With a standard or FHA mortgage, you should make the down cost in money.

Making a down cost is the one largest barrier to homeownership for patrons right this moment.

Month-to-month mortgage insurance coverage (PMI) can also be eradicated with a VA mortgage.

The typical house purchaser will spend about 1% of the house mortgage quantity per yr on non-public mortgage insurance coverage. Over 5 years, that’s about $12,500 for a $250,000 mortgage quantity.

Certain, the VA funding payment isn’t low cost. Nevertheless it enables you to purchase a house now and reduces your month-to-month cost considerably.

Maybe the one cause you’ll think about a non–VA mortgage is in the event you already had 20% down and nice credit score.

I additionally heard house sellers don’t settle for patrons who use VA loans

Truthfully, this does occur.

Nevertheless it additionally occurs to patrons who use any sort of financing. Somebody with a much bigger down cost or an all–money provide normally beats somebody utilizing a bigger mortgage.

That is the place your actual property agent is available in. It’s their job to coach the vendor and their agent that VA loans are not any tougher than different mortgage varieties.

It’s true that VA appraisers could be a bit extra choosy concerning the property. However the minimum property requirements should not that rather more stringent than these of FHA or typical loans.

VA mortgage charges FAQ

VA mortgage charges differ by lender and applicant. A effectively–certified VA mortgage applicant may qualify for a charge beneath 3% primarily based on current knowledge from our lender community.

No. VA mortgage charges change day by day attributable to market circumstances, and differ by lender. Moreover, your credit score rating and different mortgage traits will change your VA mortgage charge. Though the VA mortgage program is about up by the federal government, VA mortgage charges should not “set” by any company, however by present market circumstances. Your mortgage time period may also affect charges. A 15–yr VA mortgage usually gives a decrease charge than a 30–yr VA.

A VA mortgage is a authorities–sponsored program, however it’s not administered by the U.S. Division of Veterans Affairs or some other authorities company. Personal mortgage lenders settle for purposes, then approve loans primarily based on guidelines printed by the VA. The method is similar to that of some other mortgage program. When shopping for, you’ll apply, provide documentation, get authorised, discover a house, signal last mortgage paperwork, and shut on the mortgage. For a refinance, the VA gives a program known as the IRRRL, during which you want nearly no documentation and no appraisal. So the method is way quicker.

There are two important standards to qualify for a VA mortgage. The primary is to be eligible primarily based in your navy service. The second is to qualify for the loans itself primarily based on lending necessities. Sometimes, those that served 90 days to 2 years (relying on service dates) are eligible for the VA mortgage profit. Surviving spouses might also be eligible. To qualify for the mortgage, you normally want a 620 or larger credit score rating, and sufficient regular earnings to cowl future housing funds, different money owed, and dwelling bills.

Often, you should utilize a VA mortgage as many instances as you need, so long as your earlier VA loans have been in good standing and at the moment are paid off. While you repay a VA mortgage or refinance it with a special mortgage sort, your entitlement is restored. You need to use that entitlement once more on one other main residence. You additionally could also be eligible to have two VA loans directly in case your first buy value was low and you’ve got remaining entitlement. Understand that you’ll pay the next funding payment for the second and subsequent makes use of of your VA mortgage profit.

The VA mortgage program does provide a money–out refinance possibility. This allows you to faucet your house’s fairness and take a few of it out as money, whereas changing your present mortgage with a brand new one. One huge perk of the VA money–out refi is that it’s the one main refinance program that allows you to finance 100% of your house’s worth, so you’ll be able to withdraw all of your out there fairness. You do not want a present VA mortgage to make use of the VA money–out refinance.

Sure, you possibly can get a hard and fast–charge mortgage or an adjustable–charge mortgage (ARM) with VA backing. Adjustable charge mortgages have a tendency to supply decrease rates of interest throughout their introductory interval. After that, your rate of interest can change annually. For some lively responsibility service members who plan to promote their house inside a pair years, an ARM could provide a pretty mortgage possibility.

No, the VA house mortgage profit exists to assist qualifying veterans and their households purchase a house to reside in. You can’t use a VA mortgage to buy a trip house, rental property, or property you propose to make use of for enterprise. You’ll be able to, nevertheless, use a VA mortgage to purchase a house with a number of items, so long as you propose to reside in a single whereas renting the others out The VA additionally means that you can refinance an funding property with a brand new VA mortgage, so long as you’ll be able to show you bought the house as a main residence and lived there for an inexpensive period of time.

No, the VA mortgage program doesn’t have a most mortgage restrict. Patrons can theoretically get a mortgage of any measurement with no down cost – though, the borrower should nonetheless qualify for the mortgage primarily based on credit score, earnings, and debt ranges.

Sure, all kinds of lenders have authorization to offer VA loans. In reality, a number of the nation’s main VA lenders are credit score unions, together with Navy Federal Credit score Union. We advocate working with a lender that makes a speciality of VA loans. VA mortgage specialists know the nuances of the VA mortgage program and its eligibility necessities. They’ll assist you navigate the method easily and work out any snags that come up.

VA mortgage charges: The underside line

Mortgage charges are low in every single place, however VA charges undercut even the bottom charges of different packages.

Make the most of this profit. Whereas your VA profit by no means expires, charges this low may.

Safe your rock–backside VA mortgage charge whereas it’s out there.

[ad_2]

Source link

{kind=link}