[ad_1]

Veterinarians are a number of the most extremely skilled professionals on the market. In case you suppose being a doctor and medical faculty is hard, strive studying and training drugs on a bunch of various anatomies. All this with extra restricted funding, assets and know-how. Given these boundaries, is vet faculty price it?

These hard-working, clever individuals have a troublesome go in the event that they need to earn a Physician of Veterinary Drugs diploma, or DVM for brief.

To begin with, there are a restricted variety of vet colleges in the US. Due to this fact, the admissions course of is extremely aggressive for vet faculty candidates. These accepted right into a DVM program are in for a grueling four-year schooling, which isn’t low cost as a result of complexity of veterinary drugs.

Lastly, as soon as they develop into a DVM, the veterinarian wage isn’t fairly the place it ought to be given their coaching. As an outsider, I’d suppose DVMs would make a greater revenue than they do. Right here’s the issue: Folks love their pets, however pet house owners are sometimes unable to spend limitless funds on their loving animal like they’d on themselves if that they had a well being difficulty.

The median veterinarian wage is $99,250, in response to the Bureau of Labor Statistics (BLS). And the typical vet faculty debt is round $150,000, in response to the American Veterinary Medical Association (AVMA). Some vet college students reported debt hundreds over $400,000.

We’ve seen this excessive common vet faculty debt right here at Scholar Mortgage Planner. That’s so much, particularly contemplating the median veterinarian wage for the highest 10% of earners is $164,490.

Even the highest earners within the veterinary profession are barely making more cash than the quantity owed by the typical graduate.

Veterinarians graduate with extra pupil loans than anticipated

It takes about 4 years to get a DVM after finishing a four-year bachelor’s program. These 4 years will be extraordinarily expensive.

For instance, in-state tuition and costs at Ohio State University’s College of Veterinary Medicine is about $153,000 for a resident. However increased dwelling bills can even contribute a good portion of pupil debt. Ohio State estimates a median value of about $85,000 over the lifetime of vet faculty.

Add that to tuition will increase annually, curiosity accruing on the loans and leftover loans from any undergraduates research. It pushes the price of turning into a DVM effectively above what’s anticipated.

We’ve labored with over 250 veterinarians right here at Scholar Mortgage Planner with a median vet faculty debt of $273,000.

So, is vet faculty price it financially?

How a lot do veterinarians make?

The common veterinarian wage is about $99,000 per yr. However how does that examine to the typical school graduate with out a sophisticated diploma?

In accordance with the BLS 2021 report, the median wage for a school graduate is about $74,000.

So turning into a veterinarian results in an additional $25,000 in earnings per yr by the averages.

Let’s assume that $25,000 in further revenue sustains all through your entire 30-year profession of a DVM which works out to an additional $750,000 in lifetime earnings for a veterinarian in comparison with somebody with a bachelor’s diploma. That looks like an enormous quantity.

Taking out $273,000 in loans to make an additional $750,000 tends to make monetary sense on the floor. However keep in mind, these further earnings will probably be taxed.

If we assume a mixed 40% tax price for federal and state, then we are able to scale back that $750,000 in earnings all the way down to about $450,000 in further take-home pay.

So now we’re speaking a couple of veterinarian having an additional $450,000 to repay the $273,000 of pupil mortgage debt that made it potential for the upper veterinarian wage.

Looks like vet faculty is price it financially on the floor, however these numbers are lacking a couple of key aspects:

- These numbers don’t present that many veterinarians spend the primary 20 to 25 years of their careers saddled with mortgage funds, gazing pupil mortgage balances that don’t appear to alter and, in lots of circumstances, proceed to develop.

- The opposite piece of the equation is that the price of paying again the loans will probably be increased than the precise mortgage stability.

- Mortgage forgiveness choices are extraordinarily restricted for veterinarians. Certain, the AVMA has many options listed. However they aren’t that straightforward to get. I’ve labored with solely a few vets who work for the Division of Agriculture and would qualify for Public Service Mortgage Forgiveness (PSLF).

Let’s dive deeper into what compensation truly seems like for veterinarians.

DVM pupil mortgage compensation choices

Our expertise at Scholar Mortgage Planner reveals there are two optimum methods for veterinarians to repay pupil loans. However they’re on reverse ends of the spectrum.

- Aggressive Pay Again: For individuals who owe 1.5 occasions their revenue or much less (e.g., somebody who makes $100,000 with loans at $150,000 or much less), their finest wager is to throw each greenback they will discover into paying again their loans as quick as potential for not more than 10 years.

- Pay the least quantity potential: For individuals who owe greater than twice their revenue (e.g., somebody who makes $100,000 and owes $200,000 or extra), the aim is to get on an income-driven compensation plan that may preserve their funds low after which maximize mortgage forgiveness, whether or not it’s PSLF or taxable mortgage forgiveness. PSLF choices are restricted for many veterinarians.

Mortgage compensation for veterinarians

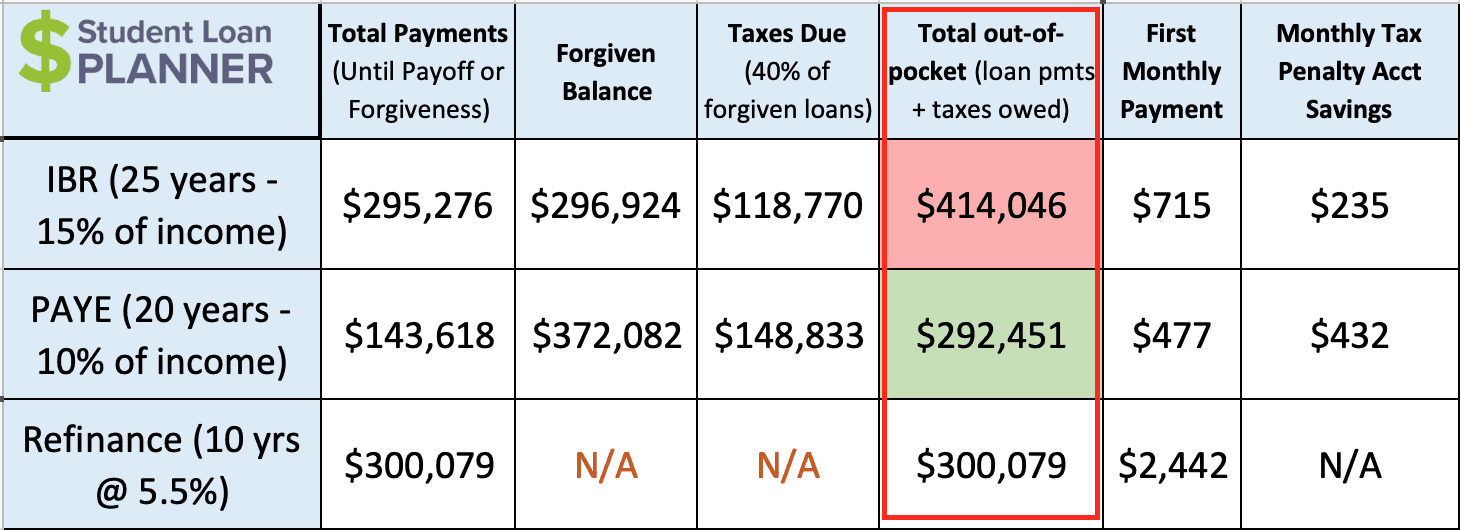

Let’s say Rachel has $225,000 in pupil loans at 6.8%. Her veterinarian common beginning wage is $75,000 and can develop about 3% per yr. She’s not married.

So let’s examine Earnings-Primarily based Reimbursement (IBR), Pay As You Earn (PAYE), and veterinarian refinancing to a 10-year mounted price.

Keep in mind how both aggressively attacking the loans (refinancing) or holding funds as little as potential and maximizing mortgage forgiveness (PAYE) would lower your expenses? IBR is neither of these.

As you possibly can see, IBR is by far the worst possibility. It’s going to finish up costing Rachel over $120,000 greater than PAYE and practically $114,000 greater than refinancing.

As for PAYE versus refinancing, the choices look comparatively shut from an out-of-pocket value. Listed below are the professionals and cons for every possibility:

PAYE

- Professional: Inexpensive month-to-month funds which can enable her to avoid wasting, make investments and put cash towards different monetary targets.

- Professional: Has 20 years to avoid wasting up for the taxes owed.

- Con: Mortgage stability will develop from $225,000 to $372,000.

- Con: It’ll take her 10 years longer in comparison with refinancing.

Refinancing

- Professional: She’ll be out of debt in 10 years or much less.

- Con: Whole out-of-pocket value is about $8,000 increased and paid again in half the time.

- Con: She loses entry to federal mortgage advantages as soon as she refinances.

Contemplating she’ll even be caught with $2,442 of refinancing month-to-month funds for 10 years with little to no flexibility, PAYE goes to be her most suitable choice.

Is vet faculty price it?

The purely monetary reply is sure, vet faculty is price it — however barely. The projected lifetime earnings of a veterinarian in comparison with the typical school grad is $450,000 after taxes versus the $292,000 in value of paying again pupil loans.

To me, that margin is manner too shut.

The unfold between a veterinarian wage and the typical school graduate simply isn’t all that compelling. To not point out they begin incomes a dwelling 4 years later resulting from in depth veterinary education and training.

Then there’s the psychology between making pupil mortgage funds for 20 to 25 years with out making a considerably increased wage versus the typical school grad.

Though it’s a well-liked profession alternative within the animal business, you want a real ardour for it as a result of making pupil mortgage funds may also be a lifestyle. It’d get particularly tight if the additional prices of getting married and elevating children comes round.

If veterinarians can preserve that long-term perspective and nonetheless really feel compelled to develop into a DVM, they’ll have a pleasant, lengthy profession with nice earnings remaining after being pupil debt-free.

Vet college students ought to solely select to pursue this path in the event that they’re all in and gained’t let pupil loans make them remorse their resolution after projecting what life will seem like 10 and 20 years after commencement.

Having a transparent understanding of how mortgage compensation works and how you can mitigate each the monetary and psychological elements of carrying that quantity of debt are each a should.

Veterinarians want a plan for pupil mortgage compensation

For veterinary graduates who’ve six-figure pupil loans, having the debt doesn’t should really feel like a heavy weight. There are many nice pupil mortgage compensation choices for veterinarians.

It’s important to have a path that might not solely save important cash but in addition a transparent understanding of the actions steps to get it carried out.

Scholar Mortgage Planner has carried out over 5,300 pupil mortgage consults for purchasers with over $1.34 billion of pupil loans. We might help you determine the optimum path in only one hour.

I work with debtors who owe between $200,000 to $400,000 in pupil loans. That makes me the purpose individual for many of our veterinarian pupil mortgage consults. Be at liberty to e mail me at [email protected] to ask any questions and study extra.

Refinance pupil loans, get a bonus in 2021

$1,000 BONUS1For 100k or extra. $200 for 50k to $99,999¹

$1,250 BONUS2For 250k+, tiered 300 to 500 bonus for 50k to 250k.2

$1,275 BONUS3For 150k+. Tiered 300 to 575 bonus for 50k to 149k.3

$1,000 BONUS4For $100k or extra. $200 for $50k to $99,9994

$1,050 BONUS5For 100k+. $300 bonus for 50k to 99k.5

$1,250 BONUS6For 100k+ or $350 for 5k to 100k.6

$1,250 BONUS7For 150k+. Tiered 100 to 400 bonus for 25k to 149k.7

Undecided what to do together with your pupil loans?

Take our 11 query quiz to get a customized suggestion of whether or not it’s best to pursue PSLF, IDR forgiveness, or refinancing (together with the one lender we expect might provide the finest price).

1Earnest: $1,000 for $100K or extra, $200 for $50K to $99.999.99. For Earnest, when you refinance $100,000 or extra by this web site, $500 of the $1,000 money bonus is supplied immediately by Scholar Mortgage Planner. Charge vary above contains optionally available 0.25% Auto Pay low costEarnest disclosures. 2Laurel Highway: In case you refinance greater than $250,000 by our hyperlink and Scholar Mortgage Planner receives credit score, a $500 money bonus will probably be supplied immediately by Scholar Mortgage Planner. If you’re a member of an expert affiliation, Laurel Highway may give you the selection of an rate of interest low cost or the $300, $500, or $750 money bonus talked about above. Gives from Laurel Highway can’t be mixed. Charge vary above contains optionally available 0.25% Auto Pay low cost. Laurel Road disclosures.3Elfi: In case you refinance over $150,000 by this web site, $500 of the money bonus listed above is supplied immediately by Scholar Mortgage Planner. Elfi disclosure. 4Sofi: In case you refinance $100,000 or extra by this web site, $500 of the $1,000 money bonus is supplied immediately by Scholar Mortgage Planner. Charge vary above contains optionally available 0.25% Auto Pay low cost. Sofi disclosures.5Commonbond: In case you refinance over $100,000 by this web site, $500 of the money bonus listed above is supplied immediately by Scholar Mortgage Planner. Commonbond disclosure. 6Credible: In case you refinance over $100,000 by this web site, $500 of the money bonus listed above is supplied immediately by Scholar Mortgage Planner. Credible disclosure.

7LendKey: In case you refinance over $150,000 by this web site, $500 of the money bonus listed above is supplied immediately by Scholar Mortgage Planner. Charge vary above contains optionally available 0.25% Auto Pay low cost.

[ad_2]

Source link

{kind=link}