[ad_1]

Should you’re an current home-owner or an aspiring one, you could have heard the phrase “home poor,” sometimes uttered by an overextended borrower.

It could additionally function a warning to a first-time home buyer from a seasoned home-owner, particularly proper now with dwelling costs so excessive.

The Definition of Home Poor

- Shopping for an excessive amount of home to your funds

- Even in case you technically make sufficient cash to afford it

- As a result of an excessive amount of of your paycheck goes towards the mortgage every month

- And different month-to-month housing bills like utilities, upkeep, and so on.

First, let’s outline what it means to be home poor. At first look, it’d sound like somebody who lives in a small or meager dwelling, however this isn’t the case.

It’s truly fairly the other – somebody who’s home poor has probably bitten off greater than they’ll chew, and is spending an excessive amount of of their earnings on housing funds.

This implies they might have bought a McMansion and don’t have a lot left over for different recurring prices, and even on a regular basis bills.

It may additionally imply that they took out a mortgage that was too giant for his or her wage, even when the property is extra modest.

It’s actually dictated by a borrower’s capability to make housing funds every month, not essentially the grandeur of the house, as budgets will differ by monetary state of affairs.

For instance, a extremely rich particular person may purchase a multi-million greenback dwelling, however wrestle to make mortgage funds as a result of their way of life is just too extravagant.

On the similar time, somebody making much less the nationwide median family earnings may purchase a less expensive dwelling, however nonetheless be home poor.

In different phrases, each wealthy and much less wealthy individuals may be home poor, assuming they purchased a property out of their worth vary and might’t deal with the associated housing expense.

Know Your Worth Vary

It’s necessary to know your worth vary, so to talk, when getting down to purchase actual property.

This isn’t a guessing sport, however moderately a fantastic science that requires mortgage calculators and a mortgage pre-approval to find out affordability, applicable mortgage dimension, mortgage sort, down fee, and so forth.

What I see all too usually is a potential home-owner going out of their worth vary to buy a house they simply should have.

Typically, it begins innocently sufficient, however earlier than lengthy, curiosity will get the perfect of them and so they slide that most worth button greater of their favourite actual property app.

These days, this will also be the results of a bidding struggle, the place the record worth was in funds, however the precise provide worth creeps greater due to competitors from different consumers.

That is one purpose why I made the suggestion to adjust your maximum purchase price lower in anticipation of an over-list bid.

Chances are high in case you can afford a $400,000 dwelling, you may need to set it to $350,000 realizing it’ll go over asking.

These Hidden Prices…

- Keep in mind all the numerous, many prices of homeownership

- Not simply the mortgage fee however the insurance coverage and property taxes

- Together with utilities (water, gasoline, electrical, trash, and so on.) and upkeep like gardening, pool service, home cleansing

- To not point out any potential repairs that can come up alongside the best way

Sadly, numerous future dwelling consumers don’t consider all of the hidden costs of homeownership, and even the not-so-hidden prices, which simply exacerbates the difficulty.

Should you’ve by no means owned your personal dwelling earlier than, you could be in for a impolite awakening. Do you recall your mother and pa telling you to take shorter showers, or to shut the fridge door, or to show off the lights!

There was a purpose for that – all of these actions lead to greater utility prices, which may be actually costly, even in case you’re tremendous conservative.

It’s possible you’ll get bonus factors for wanting past the principal and curiosity mortgage fee by contemplating property taxes and owners insurance coverage (PITI!).

However what in regards to the water invoice, trash pickup, gardening, heating and cooling, and common dwelling upkeep?

Should you had been beforehand renting, your landlord could have lined a few of these payments, and something that broke most likely wasn’t your duty. Not so if you personal the property.

This illustrates the hazard in going outdoors funds, which is unfortunately fairly frequent. It’s one of many tenets of non-public finance that’s continuously damaged.

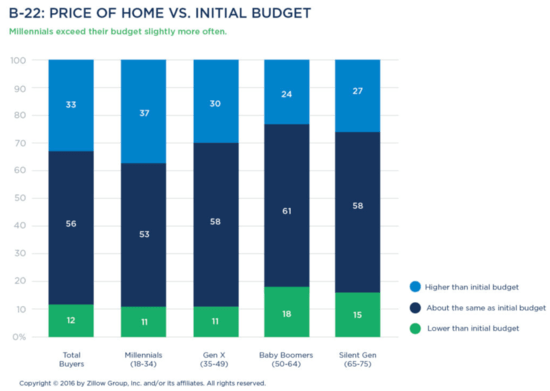

Zillow studied this again in 2016 and located {that a} third of dwelling consumers exceeded their preliminary funds, with 39% of first-time dwelling consumers responsible of doing this.

You can too see from the chart above that Millennials (sorry, it’s all the time this group) had been the most certainly to go over funds.

The scariest half about this group is that they’re most likely the most certainly to have youngsters, which can add much more dwelling bills (medical health insurance, education, and so on.) past their present state of affairs. All of the extra purpose to take child steps when shopping for a home…

The takeaway is that one can grow to be home poor in a wide range of methods, whether or not it’s deciding to pay greater than initially deliberate, or for failure to consider all the prices of homeownership.

In truth, a home-owner may get hit twice, by going over funds dwelling price-wise and never budgeting for these prices. This may spell large bother down the highway.

For the document, dwelling costs and mortgage rates have solely gone up since 2016, so my assumption is the variety of dwelling consumers going over funds has simply worsened.

How you can Keep away from Being Home Poor

- Keep inside your preliminary funds!

- And even set your most buy worth decrease than what you’ll be able to afford

- Get a pre-approval however go away a buffer past it

- Take into account the complete mortgage fee (PITI)

- Think about all utility prices

- Put aside cash for dwelling upkeep and sudden repairs

- Ensure you’ve cash left over to make different investments

- An emergency fund can be key (in case you lose your job)

First issues first, what you’ll be able to afford based on lender pointers and most debt-to-income ratios (DTI) isn’t essentially what it is best to spend on a house and a mortgage.

It’s potential to get a mortgage with a really excessive DTI ratio, nevertheless it’s an imperfect calculation that doesn’t all the time issue within the intangibles, nor precise takehome pay.

There are many recurring prices that don’t present up on a credit score report, and minimal bank card funds can fluctuate tremendously relying on excellent balances over time.

There’s a very good likelihood your bank card debt will enhance as soon as your housing expense rises, making it harder to replenish your emergency fund or save for retirement.

Moreover, numerous mortgage calculators aren’t very accurate, and have a tendency to underestimate issues like property taxes and owners insurance coverage. It could be in your greatest curiosity to overestimate these prices.

Identical goes for mortgage charges – the mortgage calculator may default to a best-case rate of interest that you just don’t essentially qualify for. Once more, overestimate when determining how much house you can afford.

Certain, get the mortgage pre-approval to see what you’ll be able to technically qualify for, however don’t essentially purchase a home that costly.

Maybe go away a buffer for gadgets that aren’t lined in that calculation, just like the utilities and the unanticipated dwelling repairs that may eat into your month-to-month funds.

House Inspections and Repairs

- A house inspection is a should except you’re a licensed contractor

- It helps uncover all the issues and potential issues with the property

- It’s possible you’ll even have to conduct a number of inspections for issues like chimneys, pool/spa, roof, and so on.

- Sadly some dwelling consumers are waiving inspections to make their provides extra aggressive

Talking of repairs, be sure to conduct an intensive dwelling inspection if you go below contract to raised anticipate any future prices, or maybe to get a credit score earlier than you progress in.

For instance, determine if the roof is wanting prefer it’ll have to be changed sooner moderately than later, or if a rework will probably be obligatory within the not-too-distant future.

There’s a purpose rental associations cost month-to-month HOA dues – they know these prices will come up finally, and funds accordingly.

Most owners in single-family houses aren’t required to put aside cash every month, however will probably face the identical points.

It may be fairly harmful if no cash is put apart in a financial savings account to handle these occasions.

A house guarantee will also be useful through the first yr or two to cowl any sudden breakdowns, and the vendor may even pay for it.

Additionally think about your future, aka your retirement. Be sure to have cash left over to fill your 401k or IRA, even in case you do plan to make use of your own home as a nest egg someday. House promoting prices are additionally tremendously underestimated.

Diversification is sweet, and as chances are you’ll recall from the large housing crash seen a few decade in the past, dwelling costs can go each up and down.

Lastly, don’t make optimistic assumptions, such as you’ll be making more cash sooner or later, as a result of it could not pan out. What is for certain is that your mortgage funds will maintain coming, as will the numerous different payments that accompany homeownership.

If you wish to maintain your own home long-term, and in addition take pleasure in different issues outdoors of it, funds accordingly. This may reduce your probabilities of turning into home poor, even when issues do take an sudden flip.

[ad_2]

Source link

{kind=link}