[ad_1]

Editor’s notice: The Biden Administration’s American Rescue Plan is the newest COVID-19 stimulus package deal and included a serious provision that eliminates taxes on pupil mortgage forgiveness for the primary time. At the moment, the measure expires on the finish of 2025. Learn what the American Rescue Plan stimulus means for debtors pursuing forgiveness underneath an income-driven compensation plan.

The USA authorities has handed three COVID-19 financial stimulus packages to date. These are the CARES Act (handed in March 2020), the Consolidated Appropriations Act of 2021 (handed in December 2020) and the American Rescue Plan (handed in March 2021).

The vast majority of the reduction for pupil mortgage debtors was included within the CARES Act. However new advantages have been added with every subsequent invoice. And President Joe Biden signed a White Home memorandum in January 2020 that prolonged the CARES Act’s cost and curiosity pause by eight months to September 30, 2021. The pause was set to run out on January 31, 2021.

On this article, we’ll take a deep dive on the present stimulus package deal for pupil loans and break down your entire choices for receiving coronavirus help. Right here’s what you might want to know.

What’s the present stimulus package deal for pupil loans?

Right here’s what’s included within the stimulus packages which may profit present or future pupil mortgage debtors:

- Suspension of all funds via September 30, 2021

- No curiosity will accrue till September 31, 2021

- The suspended funds depend in direction of mortgage forgiveness packages, together with PSLF and IDR forgiveness (PAYE, REPAYE, IBR)

- Taxes are eradicated on forgiven pupil loans via December 31, 2025

- Employers who contribute to their staff’ pupil loans obtain a tax break as much as $5,250 (via 2025)

- Debtors in default can have their months of suspended funds depend in direction of the 9 months wanted for mortgage rehabilitation

- No assortment, wage garnishment, or seizure of tax refunds will occur (backdated to March 13, 2020)

- Slight improve in most Pell Grant

- Incarcerated individuals can now obtain Pell Grants

- Over $1.6 billion in institutional debt of HBCUs has been discharged

- College students could now proceed to obtain a subsidy on sure backed Stafford loans for undergrad for an extended time period

- Employers could contribute as much as $5,250 every in direction of their staff’ pupil loans, with this program set to run out in 5 years now as a substitute of on the finish of this yr.

Right here’s what’s not been included in any of the stimulus packages.

- Canceling pupil mortgage debt

- Altering income-driven compensation packages

- Capping the quantity college students can borrow for undergraduate or graduate levels

The stimulus package deal is superb when you have federal pupil loans

Many politicians and employees teams have been clamoring for pupil mortgage cancellation to be included in one of many stimulus packages.

Whereas that didn’t come to cross, the CARES Act and subsequent government orders and payments have been terribly beneficiant for debtors with federal pupil loans.

There were already protections in place to scale back your income-based cost in case you misplaced your job.

Nonetheless, hundreds of thousands of individuals have been about to lose their jobs on the identical time, and that is clearly not what mortgage servicers are constructed for.

Debtors wanted federal assist as a result of many don’t know easy methods to recalculate their cost

Servicers like FedLoan Servicing shut down a lot of their operations firstly of the coronavirus pandemic.

So even when debtors knew they may recalculate their income-based cost to a quantity as little as $0 a month in the event that they misplaced their job, they couldn’t get somebody on the cellphone to try this in lots of instances.

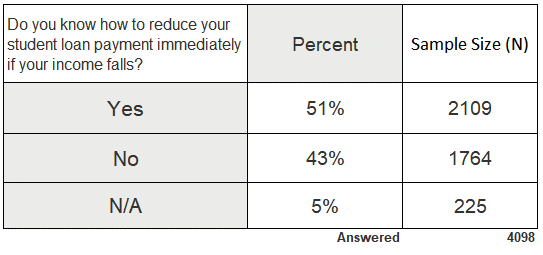

Additionally, our survey of 4,100 readers on March 18, 2020, suggested that at least 43% of borrowers didn’t even perceive easy methods to pause their federal pupil mortgage funds if their revenue fell. See the desk beneath.

Our readers are usually graduate degree-holding professionals who’re extra knowledgeable than common on pupil mortgage guidelines. Therefore, the true variety of debtors who know easy methods to recalculate their cost is probably going a lot decrease.

After I noticed this information, I knew an across-the board cost freeze was going to be wanted. That’s precisely what has occurred. And federal pupil mortgage debtors have benefited immensely consequently.

Throughout this forbearance interval, debtors have continued to accrue credit score in direction of PSLF, IDR, and different forgiveness packages. Within the case of PSLF, you would wish to take care of a full-time job at a not-for-profit or authorities employer. However these $0 a month funds would depend.

And, bear in mind, there are not any employment circumstances for 20-year PAYE and 25-year REPAYE forgiveness. So suspended funds depend for that kind of forgiveness too.

Some federal pupil mortgage debtors have been initially left behind

Initially, solely loans held by the Division of Training qualify for this curiosity and cost freeze, due to the stimulus plan language. So which means loans made underneath the Federal Family Education Loan Program (FFELP) didn’t qualify in the event that they have been held by a industrial lender.

The federal authorities stopped issuing FFELP loans in 2010. So anybody who graduated or went to high school earlier than that point doubtless has this type of pupil mortgage. The excellent news is that the Department of Education announced on March 30, 2021 that it was increasing the COVID-19 emergency reduction to debtors who had defaulted on a privately-held FFEL mortgage. It stated that the enlargement would offer assist to 1.14 million debtors.

The Division of Well being has a big pupil mortgage program too. Dentists, physicians and nurses typically take out Well being Professions Scholar Loans (HPSL) or Loans for Deprived College students (LDS). These loans carry a 5% rate of interest and often present up underneath the mortgage servicer Heartland ECSI when you have them.

You possibly can really consolidate these loans right into a Direct Consolidation Mortgage to obtain forgiveness. Nonetheless, most debtors assume Well being Professions pupil loans are personal and thus have been ineligible for forgiveness packages. That is a particularly widespread five-figure mistake our shoppers make when managing their very own pupil loans.

When lawmakers not noted the Division of Well being pupil loans from any reduction, it affected many hundreds of healthcare practitioners. Fortunately, the HRSA announced in February 2021 that it had additionally determined to retroactively waive is waiving curiosity and prolong administrative forbearance to Well being Professions Scholar Mortgage and Nurse College Mortgage debtors via September 30, 2021.

The stimulus invoice gives assist for debtors in default

Tens of millions of pupil mortgage debtors are in default on their pupil loans. One option to exit default is to make 9 months of consecutive funds.

Sadly, debtors typically miss a cost and can’t get their loans rehabilitated. And that may result in wage garnishment and seizure of tax refunds.

Importantly, in case you’re making an attempt to rehabilitate your federal pupil loans, with the stimulus plan now you can depend the months of suspended funds in direction of the 9 months wanted to exit default.

That’s huge information as most pupil debtors will be capable of rehabilitate their loans instantly when the forbearance ends on September 30, 2021.

Whenever you rehabilitate your pupil mortgage, you take away this adverse occasion out of your credit score rating and get enrolled in an income-driven plan in order that the loans are reasonably priced for the long run.

The opposite option to handle default is to consolidate your pupil loans. Nonetheless, that doesn’t take away the default out of your credit score rating.

Tax refund seizure, collections, and wage garnishment is on maintain

The COVID-19 reduction invoice pauses collections efforts on federal pupil loans. It additionally stops collections, wage garnishment, and seizure of tax refunds retroactive to March 13, 2020.

Importantly, this consists of defaulted FFEL debtors who didn’t have entry to stimulus package deal pupil mortgage advantages till March 2021.

That is huge information for debtors struggling essentially the most. If you happen to had your wages or tax refund seized on or after March 13, 2020, you might want to be certain that your tackle is present within the Division of Training system. Name 800-621-3115 to ensure they mail your examine to the precise tackle.

Employers can now deduct pupil mortgage funds made for workers’ pupil debt

Employer pupil mortgage compensation help is now tax-free (for each staff and employers) till December 31, 2025. Lobbyists for giant employers have needed to make this a tax-deductible profit for years. The hope was that it could incentivize youthful employees to stick with their firms.

By extending this profit for 5 years as a substitute of 1, Congress is actually speaking to giant employers that this profit might be everlasting. I count on an explosion of employer pupil mortgage help packages consequently.

I’ve gone on the document that employer pupil mortgage help does not help as much as you think. And it might probably really damage you in some instances.

It’s the identical factor as giving a tax break for employer-provided medical health insurance. It makes the workforce much less cell and extra tied to their job. And that’s within the curiosity of the employer greater than the worker.

Importantly, pupil mortgage contributions change cash which may have gone in direction of larger wages, which proceed after you will have $0 pupil loans.

Even some non-profit hospitals require that funds they make for pupil loans be utilized on to loans held by the mortgage servicer. And that simply doesn’t make sense within the case of a borrower working in direction of PSLF.

At the least now you possibly can apply lump sum funds to PSLF IDR month-to-month funds, which was not all the time the case.

Scholar mortgage forgiveness is tax-free for 5 years

Maybe the largest influence of President Biden’s American Rescue Plan is that it dictated that no federal debtors can pay revenue taxes on a discharged pupil mortgage via the top of 2025.

Some packages just like the Public Service Mortgage Forgiveness (PSLF) program already supplied tax-free forgiveness. But it surely was unclear if the IRS would tax debtors for the coed debt forgiveness they acquired after finishing one of many income-driven repayment plans. That’s why we’ve historically suggested our shoppers who’re hoping to earn IDR forgiveness to avoid wasting up for a possible tax legal responsibility 20-25 years down the highway.

However anybody who earns IDR forgiveness over the following 5 years received’t obtain a tax invoice on the forgiven pupil mortgage debt. Sadly, there received’t be a big variety of pupil mortgage debtors who might be eligible for forgiveness till the 2030s. We’ll have to attend to see if Congress considers making this a everlasting change in some unspecified time in the future down the highway.

Learn more about the student loan tax relief act.

Full disclosure: this web site receives a big portion of its income from readers who determine to refinance their pupil loans to a decrease rate of interest.

Federal pupil mortgage debtors obtain an curiosity freeze. However personal pupil mortgage debtors obtain a slap within the face.

By setting federal pupil mortgage rates of interest at 0%, you successfully kill any student loan refinancing (aside from refinancing loans which are already personal).

Our firm has money reserves. And folks will refinance once more sooner or later when federal pupil mortgage curiosity is now not at 0%. Plus, debtors wanted pupil mortgage reduction throughout this disaster, and I’m glad a few of our readers are getting that assist.

I’m incensed although that massive numbers of debtors who refinanced their pupil loans with personal lenders will get completely no assist from Congress.

They appear to be bailing out everybody else.

What message do you ship to debtors who needed to responsibly pay down their pupil debt whenever you rescue all federal pupil mortgage debtors however go away personal pupil mortgage debtors out of any reduction package deal?

A critic may ask what Congress may have carried out? It’s easy: reimburse personal firms for the curiosity simply as they did for a number of different industries.

Make this short-term pupil mortgage reduction result in a long-term plan

Suspending funds and curiosity for a lot of months is a good step for federal pupil mortgage debtors.

Clearly, we want extra debtors had been included within the reduction package deal.

Sadly, pupil loans will nonetheless be there after the cost and curiosity freeze is over.

If you happen to want a long run plan on easy methods to get to $0 of pupil loans endlessly, that’s what we specialize in.

What do you consider the coed mortgage coronavirus stimulus invoice? Hold forth within the feedback.

Refinance pupil loans, get a bonus in 2021

$1,000 BONUS1 For 100k or extra. $200 for 50k to $99,999¹

$1,050 BONUS2For 100k+. $300 bonus for 50k to 99k.2

$1,250 BONUS3 For 250k+, tiered 300 to 500 bonus for 50k to 250k.3

$1,275 BONUS4 For 150k+. Tiered 300 to 575 bonus for 50k to 149k.4

$1,000 BONUS5For $100k or extra. $200 for $50k to $99,9995

$1,250 BONUS6 For 100k+ or $350 for 5k to 100k.6

$1,250 BONUS7For 150k+. Tiered 100 to 400 bonus for 25k to 149k.7

Undecided what to do along with your pupil loans?

Take our 11 query quiz to get a personalised advice of whether or not you must pursue PSLF, IDR forgiveness, or refinancing (together with the one lender we expect may provide the finest price).

All charges listed above signify APR vary. 1Earnest: $1,000 for $100K or extra, $200 for $50K to $99.999.99. For Earnest, in case you refinance $100,000 or extra via this web site, $500 of the $1,000 money bonus is supplied immediately by Scholar Mortgage Planner. Charge vary above consists of non-compulsory 0.25% Auto Pay low costEarnest disclosures.

2Commonbond: If you happen to refinance over $100,000 via this web site, $500 of the money bonus listed above is supplied immediately by Scholar Mortgage Planner. Commonbond disclosure.

3Laurel Street: If you happen to refinance greater than $250,000 via our hyperlink and Scholar Mortgage Planner receives credit score, a $500 money bonus might be supplied immediately by Scholar Mortgage Planner. In case you are a member of knowledgeable affiliation, Laurel Street may give you the selection of an rate of interest low cost or the $300, $500, or $750 money bonus talked about above. Gives from Laurel Street can’t be mixed. Charge vary above consists of non-compulsory 0.25% Auto Pay low cost. Laurel Road disclosures.4Elfi: If you happen to refinance over $150,000 via this web site, $500 of the money bonus listed above is supplied immediately by Scholar Mortgage Planner. Elfi disclosure. 5Sofi: If you happen to refinance $100,000 or extra via this web site, $500 of the $1,000 money bonus is supplied immediately by Scholar Mortgage Planner. Charge vary above consists of non-compulsory 0.25% Auto Pay low cost. Sofi disclosures. 6Credible: If you happen to refinance over $100,000 via this web site, $500 of the money bonus listed above is supplied immediately by Scholar Mortgage Planner. Credible disclosure.

7LendKey: If you happen to refinance over $150,000 via this web site, $500 of the money bonus listed above is supplied immediately by Scholar Mortgage Planner. Charge vary above consists of non-compulsory 0.25% Auto Pay low cost.

[ad_2]

Source link

{kind=link}