![What to do with home equity & your extra cash [INFOGRAPHIC]](https://198businesscreditnews.com/wp-content/uploads/2021/09/Homeowners-have-hit-the-highest-equity-ever.jpg)

[ad_1]

Studying Time: 3 minutes

These are the highlights:

- The collective wealth amongst U.S. householders — saved as residence fairness — has boomed, big-time.

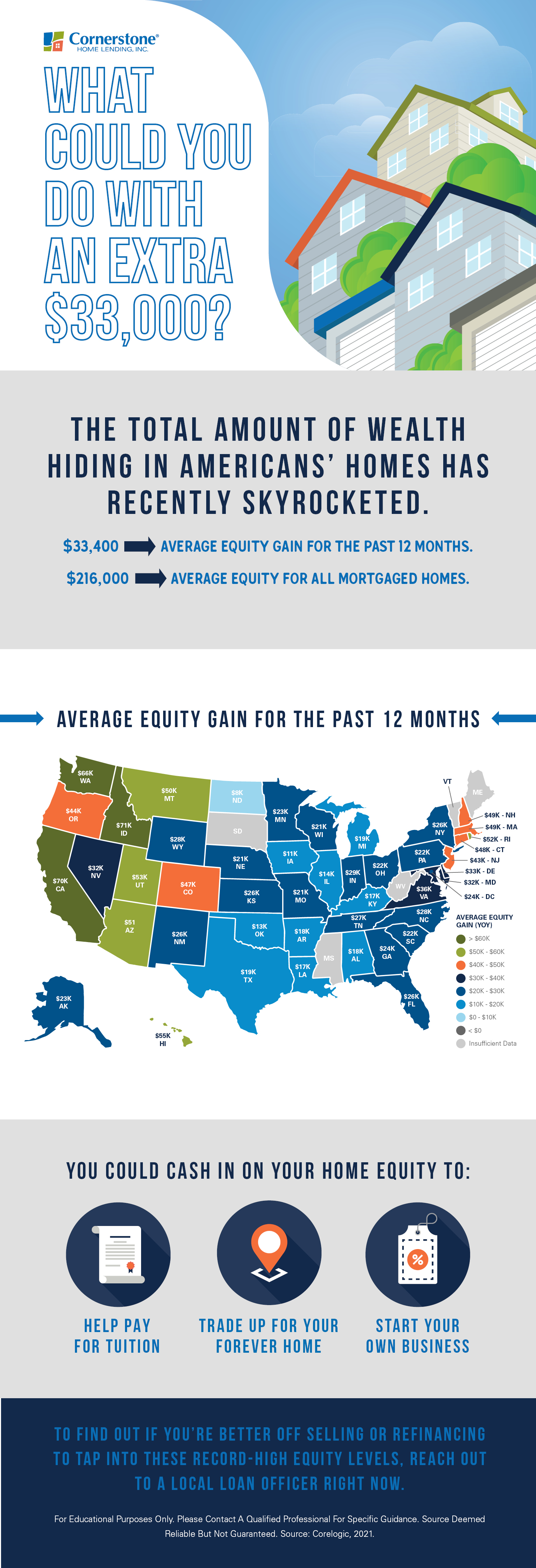

- Inside the previous 12 months, householders gained $33,400 in residence fairness on common; the common fairness for mortgaged houses has risen to $216,000.

- Whether or not you decide to sell or cash in and refinance, depend on the truth that your property fairness beneficial properties may make it easier to attain your future objectives.

It actually pays to be a home-owner. Householders within the U.S. are breaking information and now have seen a virtually $1.9 trillion improve in out there residence fairness since early 2020. Understanding what residence fairness means and when and how one can use it could make it simpler to resolve what to do together with your money.

What the heck is residence fairness? A fast refresher

Listed here are 5 key info to recollect:

1. Residence fairness is the appraised worth of your property minus what’s owed.

- If your own home was lately appraised at $300,000 and $100,000 is owed in your mortgage, it leaves $200,000 out there in fairness.

- Many lenders require {that a} borrower maintain a minimum of a 20-percent stability (80-percent LTV ratio) as a precaution, or else pay mortgage insurance coverage.

2. A house with unfavorable fairness means a home-owner owes extra on their mortgage than what their house is price.

- Destructive fairness can happen when a house’s worth declines — the alternative of the numerous appreciation seen in at present’s market.

- This additionally known as an “upside-down” or “underwater” mortgage.

3. Residence value appreciation helps your fairness — and your wealth — improve.

- You construct residence fairness by way of a mixture of appreciation and lowering your mortgage principal (by paying your month-to-month mortgage funds).

- This means to create wealth — and long-term monetary stability — is without doubt one of the essential reasons Americans prioritize homeownership and select to grow to be householders.

CoreLogic’s President and CEO Frank Martell says:

“Home-owner fairness has greater than doubled over the previous decade and grow to be an important buffer for a lot of weathering the challenges of the pandemic. These beneficial properties have grow to be an vital monetary instrument and boosted client confidence within the U.S. housing market, particularly for older householders and child boomers who’ve skilled years of value appreciation.”

4. A cash-out refinance offers you entry to tappable (out there) residence fairness.

- Many householders “money out” their fairness with a mortgage refinance, whereas additionally making month-to-month funds extra inexpensive with a greater mortgage time period and rate of interest.

- Changing an current mortgage with a brand new one offers the distinction in money; an ordinary cash-out refinance will exceed the remaining stability by 5 % or extra.

What are you able to do together with your fairness? Householders most frequently money of their fairness to pay for big-ticket bills, like:

- Faculty tuition.

- Emergency financial savings.

- Excessive-interest debt.

- Residence renovation.

- Funding alternatives.

- Medical bills.

- Particular events or household holidays.

With a cash-out refinance, you may stand up to 80 % of your property’s worth as money and use it for any function.

There’s a greater strategy to mortgage — and a quicker strategy to refinance. Download LoanFly now.

5. Some householders additionally use residence fairness to improve to a brand new home earlier than promoting one other.

- With a house fairness mortgage, a home-owner can entry the additional funds to buy a brand new home earlier than closing on their earlier residence.

- Usually, a home-owner must have a minimum of 20-percent fairness left over on their mortgage, together with every other funds wanted to pay for added charges connected to the brand new mortgage.

If you happen to’re not pleased with the house you’re residing in — which can have been made all of the extra apparent by current time spent sheltering in place — you can leverage your fairness to promote and comfortably transfer up into the subsequent value vary. Your fairness beneficial properties coupled with at present’s traditionally low mortgage charges (which can be quickly anticipated to rise) can yield an computerized shopping for energy improve.

As First American’s Chief Economist Mark Fleming explains:

“Present householders at present are sitting on document quantities of fairness. As householders acquire fairness of their houses, the temptation grows to listing their present residence on the market and use the fairness to buy a bigger or extra engaging residence.”

Tapping into your fairness could be straightforward. But at the same time as fairness reaches record-breaking volumes, not all householders are utilizing it. A lot of this has to do with a easy lack of know-how. Householders could not know the way a lot cash they now have out there to them.

If your property’s been getting cash because the market booms:

These further funds could possibly be there for the taking. Examine in in your rising fairness and get your questions answered quick. Connect with an area mortgage officer who can stroll you thru your choices.

Whereas refinancing may make a big distinction within the quantity you pay every month, there are different prices it is best to contemplate. Plus, your finance costs could also be increased over the lifetime of the mortgage.

For instructional functions solely. Please contact a certified skilled for particular steering.

Sources are deemed dependable however not assured.

[ad_2]

Source link

{kind=link}