[ad_1]

I’ve observed a pattern currently. Everybody’s an actual property professional.

It appears the most recent crisis and restoration has turned nearly each single particular person right into a guru on all issues to do with house shopping for and promoting.

I suppose a part of it has to do with the truth that the large housing bubble that fashioned a decade in the past swept the nation and was entrance web page information.

It additionally immediately affected tens of millions of People, many who serially refinanced their mortgages, then discovered themselves underwater, then finally quick offered, have been foreclosed upon, or held on for the experience again as much as new heights.

It’s a standard dialog piece today to speak about your native housing market.

Due to larger entry to info, of us are scouring Redfin and Zillow and arising with theories about what that house ought to promote for, or what they ought to have listed it for.

Neighbors are getting upset when close by listings are to not their liking for one cause or one other. What have been they considering?!

A New Housing Bubble Mentality

- Actual property is red-hot once more because of restricted provide and intense demand

- It will probably really feel like an ominous signal that we’re headed down a darkish street once more

- However that alone isn’t cause sufficient for the housing market to crash once more

- There need to be clear catalysts and monetary stress for an additional main downturn

All of this chatter portends some form of new bubble mentality in my thoughts, although it appears everyone seems to be simply basing their hypotheses on the latest housing bust, as a substitute of maybe contemplating an extended timeline.

One may take a look at the latest run-up in house costs as one more bubble, lower than a decade since house costs bottomed round 2012.

In any case, many housing markets have now surged properly past their earlier lofty ranges seen about 15 years in the past when house costs peaked.

For instance, Denver space house costs are about 86% increased than they have been in 2006. And again then, everybody felt house costs have been utterly uncontrolled.

In different phrases, house costs have been haywire, and are actually practically double that.

In the meantime, the standard U.S. house is at present valued round $273,000, per Zillow, which is about 27% increased than the height of $215,000 seen in early 2007.

It’s additionally practically 70% increased than the standard house value of $162,000 again in early 2012, when house costs roughly bottomed.

So if wish to take a look at house costs alone, you might begin to fear (although you additionally need to think about inflation which can naturally elevate costs over time).

However they are saying bubbles are financially pushed, and we’ve yet to see a return to shoddy underwriting.

I’ll say that there’s been a latest return of near-zero down financing, with many lenders taking Fannie and Freddie’s 97% LTV program a step additional by throwing a grant on prime of it.

This implies debtors can purchase houses right this moment with just 1% down payment, and even that tiny contribution could be gifted from another person.

So issues is perhaps getting a bit of murky, particularly in the event you take into account the rise in costs over the previous 4 or 5 years.

One may additionally argue that affordability is being supported by artificially low mortgage rates, which historical past tells us gained’t be round eternally.

There’s additionally a common sense of greed within the air, together with a sense amongst owners that they’re getting richer and richer by the day.

That kind of angle typically breeds complacency and pointless risk-taking.

However When Will Dwelling Costs Crash Once more?!

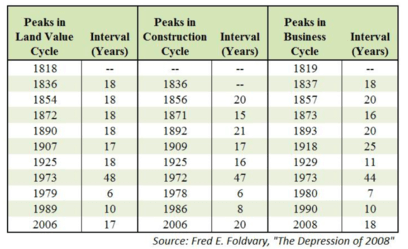

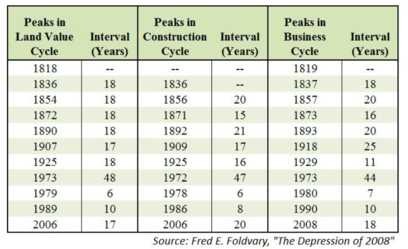

- If you happen to imagine in cycles, which appear to be fairly evident in actual property and elsewhere

- We’ll see one other housing crash sooner or later comparatively quickly

- There seems to be an 18-year cycle that has been noticed for the previous 200 years

- This implies the following house value peak (after which bust) would possibly start in 2024

All of these latest house value positive factors would possibly make one surprise when the following housing market crash will happen.

In any case, house costs can solely go up for therefore lengthy earlier than they drop once more, proper?

Effectively, the reply to that age-old query may not be as elusive as you suppose.

The true property market apparently strikes in cycles that some economists suppose could be predicted to a comparatively excessive diploma.

Whereas not an ideal science, there appears to be “a gradual 18-year rhythm” that has been noticed since across the yr 1800.

Sure, for over 200 years we’ve seen the actual property market comply with a well-recognized growth and bust path, and there’s actually no cause to suppose that may cease now.

It places the following house value peak across the yr 2024, adopted by maybe a recession in 2026 and a march down from there.

How a lot house costs will fall is a completely totally different query, however given how a lot they’ve risen (and may rise nonetheless), it may very well be a protracted, good distance down.

And we would not have tremendous low mortgage charges at our disposal to avoid wasting us this time, which is a scary thought.

You’ll By no means Get Again Into the Housing Market…

- There are 4 important phases in an actual property cycle

- A restoration interval and an enlargement interval

- Adopted by hypersupply and an eventual downturn

- Don’t imagine the hype that in the event you don’t purchase right this moment, you’ll by no means get the possibility!

One other housing bust in inevitable, regardless of of us telling us we’ll by no means get again in once more if we promote our house right this moment, or don’t purchase one tomorrow.

There are 4 phases to this predictable cycle, together with a restoration part, which we’ve clearly skilled, adopted by an enlargement part, the place new stock is created to fulfill demand. That is taking place now.

For the time being, house builders are ratcheting up provide to fulfill the extraordinary demand out there, with some 45 million expected to hit the average first-time home buyer age this decade.

The issue is like anything in life, when demand is scorching, producers tend to overdo it, creating extra provide than is important.

That brings us to the following part, a hypersupply interval the place builders overshoot the mark and wind up with an excessive amount of new building, at which level costs plummet and a recession units in.

The excellent news (for current owners) is that in keeping with this principle, we gained’t see one other house value peak till round 2024.

Meaning one other three years of appreciation, give or take, or not less than no main losses for the actual property market as a complete.

So even in the event you bought a house lately and spent greater than you’d have appreciated, it may very properly look low-cost relative to costs a couple of years down the road.

The dangerous information is that the actual property market is destined to stall once more in simply three quick years, which means the upside goes to decrease fairly a bit over the following few years.

This is perhaps very true in some markets which are already priced a bit of bit forward of themselves, which can be working out of room to go a lot increased.

However maybe extra essential is the truth that house costs have a tendency to maneuver increased and better over time, even when they do expertise momentary booms and busts.

So in the event you don’t try to time the market you may revenue handsomely over the long run, assuming you may afford the underlying mortgage.

And bear in mind, there’s more to homeownership than just the investment.

[ad_2]

Source link

{kind=link}