[ad_1]

Does inflation trigger mortgage charges to rise?

Many individuals consider inflation by way of day-to-day costs: the rising value of a gallon of gasoline, for instance, or a loaf of bread on the retailer.

Mortgage charges might sound additional indifferent from worth pressures. However in actual fact, the 2 are carefully associated.

The fundamental idea is that mortgages behave similar to bonds: when inflation rises and buying energy falls, rates of interest should additionally rise to maintain traders .

Publish-COVID inflation fears have many predicting higher mortgage rates in 2021. The query now’s how rapidly — and the way a lot — each numbers will rise.

Find a low mortgage rate today (May 18th, 2021)

On this article (Skip to…)

Inflation and mortgage charge developments

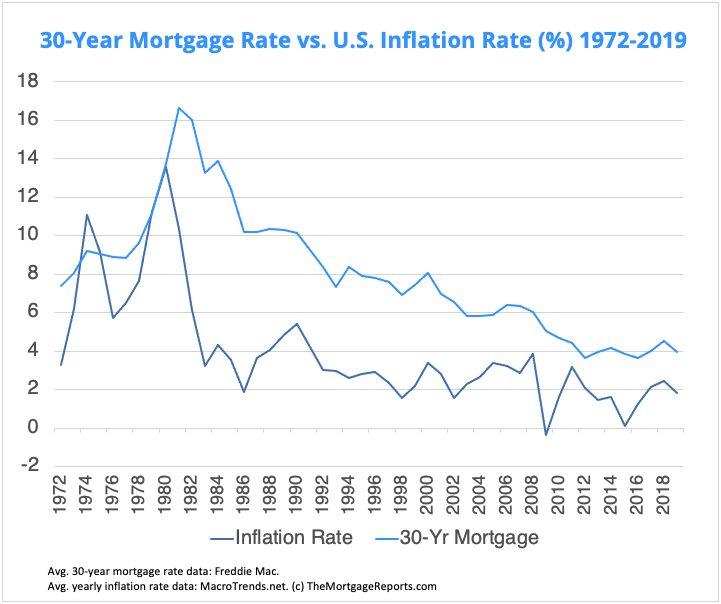

It’s not laborious to identify the connection between mortgage charges and inflation.

Evaluate a historic graph of 1 with the opposite, and it’s plain to see how mortgage charges and inflation transfer kind of in sync.

On the time this text was written, there was a rising worry of future inflation among the many investors that ultimately determine mortgage rates.

Many imagine an inflow of money from COVID stimulus plans, together with a continued low-rate coverage from the Federal Reserve, may trigger inflation to skyrocket in 2021.

This worry alone has been sufficient to push mortgage charges greater in some weeks.

However, at different instances, inflation fears have served solely to forestall charges from falling too far.

Why’s all this taking place? And the way seemingly is it we’ll quickly be seeing noticeably greater mortgage charges? Learn on to search out out.

Lock in at today’s low mortgage rates. Start here (May 18th, 2021)

What’s inflation?

Inflation is outlined as, “a common enhance in costs and fall within the buying worth of cash” by Oxford Dictionaries.

As an instance: Inflation within the US spiked at 13.55% in 1980. So in 1980, your {dollars} would have purchased you 13.55% much less at a retailer than they’d have in 1979. To take a look at it one other manner, it might have value you 13.55% extra to purchase the identical issues — $113.55 as an alternative of $100.

That’s what it means for a similar amount of cash to have a decreased buying energy.

Since 1980, inflation has steadily fallen. Its highest level since then was 5.4% in 1990. Since 2011, it’s jogged alongside at a charge of roughly 2% or beneath.

In consequence, many people have forgotten to be involved about inflation. However traders haven’t. And neither has our central financial institution, the Federal Reserve.

How does inflation have an effect on mortgage charges?

Inflation has a robust affect on mortgage charges. And that’s as a result of mortgage rates are determined by the bond market.

Similar to 10-Yr Treasurys, for instance, traders buy bundles of mortgages (known as Mortgage Backed Securities or MBS) and revenue from the curiosity paid on them.

In different phrases, mortgages are continually purchased and bought by traders.

Mortgage traders concentrate on future returns

We mentioned traders have a protracted reminiscence with regards to inflation. And you’ll see why.

Suppose you purchased a fixed-return asset comparable to an MBS or U.S. Treasury bond at present. You may get a yield (an annual return) of one thing over 2% on MBS and 1.6% on a Treasury bond, based mostly on figures for mid-Might 2021.

However, in the event you’re an investor anxious that inflation may develop into excessive, you gained’t wish to purchase long-term, fixed-yield property. As a result of your 1.6% or 2% yield could not purchase you a lot in 2, 5, or 10 years’ time.

Worse, bond yields just about all the time rise in keeping with the inflation charge.

So you might end up caught with a bond yielding 2% for as much as 30 years, when in a couple of years, yields could be two or 3 times as excessive — and even greater.

When traders are avoiding such bonds, yields (and the charges debtors pay) go up. As a result of sweetening the deal is the one approach to entice reluctant traders.

After all, if you have already got a fixed-rate mortgage mortgage, your month-to-month funds gained’t be affected. However while you resolve to purchase a home or refinance, you might be on the hook for greater charges if inflation has elevated.

Do mortgage charges all the time enhance with inflation?

For essentially the most half, sure. You sometimes get greater mortgage charges in periods of excessive inflation and decrease ones with low inflation.

Nevertheless, accountable economists not often use the phrases ‘all the time’ or ‘by no means.’ And that’s as a result of nothing’s ever sure on this planet of financial forecasting.

In the course of the interval of post-pandemic restoration, issues are particularly unpredictable.

Mortgage charges haven’t all the time reacted to financial information as anticipated. And traders and economists are break up on whether or not we’ll see runaway inflation or — because the Fed believes — worth pressures will probably be solely momentary.

COVID, inflation fears, and mortgage charges

Why is COVID-19 driving inflation?

The COVID-19 pandemic has been a significant driver of current inflation.

First, coronavirus created a necessity for enormous authorities spending on combating the pandemic and offering aid to People who’d suffered economically.

However COVID additionally created different issues because the medical emergency receded.

For instance, provide chains had been disrupted as our home economic system — in addition to international economies — struggled to reboot. So automotive vegetation had been left idle owing to a scarcity of processing chips. And costs of metals, lumber, and different uncooked supplies shot up, purely as a result of demand outstripped provide.

Virtually as importantly, US employers struggled to restaff having beforehand laid off staff.

Collectively, these pandemic-related drivers have undoubtedly pushed up the inflation charge.

What to anticipate within the coming months

On the time this was written, the speed of inflation was operating just a bit heat. However markets had been nonetheless obsessive about inflation.

Based on Bureau of Labor Statistics knowledge associated to April 2021:

“During the last 12 months, the all objects index elevated 4.2 p.c earlier than seasonal adjustment. That is the most important 12-month enhance since a 4.9-percent enhance for the interval ending September 2008.” –BLS

So markets are obsessed as a result of they’re involved about future (slightly than precise) inflation.

Traders would say they’re wanting forward and adjusting their methods to accommodate a future menace.

However there’s a hazard that groupthink about inflation may flip fears right into a self-fulfilling prophecy.

On Might 13, 2021, New York Instances financial correspondent Neil Irwin wrote: “Skilled inflation-watchers are on shut look ahead to indicators that these forces could be unleashing a type of fascinated about worth dynamics unseen because the early Nineteen Eighties, when costs rose partially as a result of everybody anticipated them to.”

The query is, will this be a short-term, one-time adjustment? Or may it flip into one thing that brings a constantly greater inflation charge for years to come back?

No one is aware of. However the Fed is assured that is only a momentary blip.

Will mortgage charges hold rising in 2021?

No one can ever be sure concerning the future route of mortgage charges. However, if inflation does take maintain, it’s past extremely seemingly that mortgage rates of interest will hold rising.

They could nicely climb greater even when the Fed is true about inflation cooling off inside a couple of months.

That’s as a result of financial development sometimes brings greater mortgage charges. And practically all economists imagine a growth is imminent.

May mortgage charges fall in 2021?

Rising charges appear seemingly, however aren’t assured. Why? As a result of there are many threats to the U.S. economic system that would arrest will increase and even perhaps ship charges decrease.

For instance, suppose some future variant of SARS-CoV-2 (the virus that causes COVID-19) emerges that seems to be proof against vaccines.

If that had been additionally extremely transmissible, it may set again all of the progress and restoration we’ve made since March 2020 — a minimum of till new vaccines are developed.

Or think about if sufficient traders all of a sudden determined that the inventory market is an overinflated bubble and pop it. That, too, could be an infinite setback for the economic system that’s fully unbiased of the pandemic.

Now, it’s possible you’ll suppose these threats are manner much less seemingly than both extra inflation or a growth. And this author would agree with you. However neither the 2 threats above nor others are unthinkable. It’s attainable they might occur.

And that’s why future mortgage charges can by no means be predicted with absolute certainty.

How does all this have an effect on you?

Studying about inflation and mortgage charges may also help you perceive what’s taking place within the greater financial image.

However what does all of it means for you? How does inflation have an effect on your individual house mortgage and your present or future mortgage funds?

For those who’re refinancing, when must you lock a charge?

Selecting when to lock your mortgage charge is all the time a raffle. You weigh the chances of various situations arising and of the totally different dangers and rewards they current.

For instance, it often is smart to lock your mortgage in the event you suppose charges are seemingly rise. And in the event you imagine charges will full considerably? You may wait.

However there’s by no means a “proper” reply. As a result of, as we mentioned, there’s by no means any assure about how charges will transfer from sooner or later to the following.

The Mortgage Reviews gives recommendation — up to date each enterprise day and on Saturdays — on what we expect could be the smartest transfer: to lock your charge or to proceed to drift it.

You possibly can visit that page as a useful resource, and hold popping again till you’re able to lock.

Check your mortgage rates today (May 18th, 2021)

For those who’re deciding when to purchase a house

Dwelling patrons could be considering now’s a nasty time to get into the actual property market.

Mortgage charges had been on the time this was written than they had been for a lot of 2020. And residential worth rises are trending upward, too.

CoreLogic reckons: “Dwelling costs nationwide, together with distressed gross sales, elevated 12 months over 12 months by 11.3% in March 2021 in contrast with March 2020 and elevated month over month by 2% in March 2021 in contrast with February 2021.”

But it surely solely is smart to delay in the event you imagine mortgage charges are going to fall and residential worth rises are going to average or drop.

it solely is smart to delay in the event you imagine mortgage charges are going to fall and residential worth rises are going to average or drop… Neither seems seemingly proper now.

Each of these might be prospects. However neither seems seemingly proper now.

So seemingly the easiest way ahead is to seize your house on the primary rung of the housing ladder as quickly as you’ll be able to.

Which may even imply selecting a extra modest house than you’d hoped for, if costs in your space are out of attain. However keep in mind — you’ll be able to all the time commerce as much as your dream house when you’ve benefitted from the rising house costs and residential fairness positive aspects which might be at the moment your enemy.

For extra assistance on this subject, see:

The underside line is that purchasing a house is a big monetary determination.

You need to time your buy for while you’re financially and emotionally prepared — not based mostly on slight modifications within the rate of interest market.

Verify your new rate (May 18th, 2021)

[ad_2]

Source link

{kind=link}