[ad_1]

-

Your common of accounts decreased due to a brand new account.

As we’ve written about many occasions within the articles in our Data Heart, the age of a tradeline is extraordinarily necessary, as is your general credit score age. It’s because credit score age is linked to fee historical past, which is vitally necessary to your credit score well being.

Fee historical past makes up 35% of your credit score rating and credit score age contributes 15% to your rating. Whenever you add the 2 collectively, you get 50%, which signifies that half of your credit score rating is managed by these two related components.

Inside the credit score age class, your common age of accounts is considered one of the necessary variables. The extra age your tradelines have, the extra they’ll profit your credit score. Due to this fact, anytime you lower your common age of accounts, you run the danger of your rating lowering consequently.

So in case you lately opened a brand new major tradeline or in case you have been added as a licensed person to an account that lacks age, the lower in your common age of accounts may be what’s behind your credit score rating troubles.

-

Your account balances elevated.

Did you utilize credit score to make a big buy lately? Have you ever been accumulating extra debt by not paying the complete steadiness you charged every month? If both of those eventualities is true for you, that would clarify why your credit score rating took a dive.

As your account balances enhance, so does your credit score utilization fee. That is unhealthy information to your credit score rating since credit score utilization contributes about 30% of your rating.

When you’ve been utilizing your bank card extra usually with out paying it off completely every month, that may very well be the supply of the change in your credit score rating.

Low utilization is favorable because it signifies that you’re not overextending your self financially. However, excessive utilization reveals that you’re utilizing loads of your accessible credit score, which implies you’re statistically extra more likely to default on a debt sooner or later. Because of this, excessive credit score utilization is penalized by credit score scoring fashions.

Luckily, there are numerous methods you should utilize to beat the issue of excessive revolving credit score utilization, akin to pre-paying your bank card invoice earlier than your assertion time limit, making extra frequent funds all through the month, growing your credit score restrict, or getting a steadiness switch card.

Learn extra about how one can enhance your utilization ratios in “What Is the Distinction Between Particular person and Total Credit score Utilization Ratios?”

Whenever you open a brand new account, it could possibly harm your credit score rating for a couple of causes. The primary and most necessary motive is that the account has no age, which implies it will negatively have an effect on your common age of accounts.

As well as, there was seemingly a tough inquiry in your credit score report on account of making use of for the brand new mortgage. In “Are Inquiries Actually Killing Your Credit score? What You Must Know,” every current exhausting inquiry in your report might have an effect on your credit score rating by as much as 5 factors.

The brand new account can also have a detrimental influence on the “new credit score” portion of your credit score rating. Having new credit score makes you appear to be a riskier borrower, which implies it may barely scale back your rating.

Nevertheless, new credit score solely makes up about 10% of your credit score rating, so the influence of opening one new account would seemingly be comparatively small and it might diminish over time.

-

You utilized for credit score however your software was denied.

Making use of for a mortgage or bank card, whether or not your software is permitted or denied, the ensuing exhausting inquiry may harm your credit score rating barely.

As we simply talked about, if you apply for credit score, the lender often has to do a tough pull (AKA a tough inquiry) in your credit score report back to see in case you qualify.

This doesn’t all the time lead to a brand new credit score account being opened. Typically, for instance, your credit score software may get rejected by the lender, or maybe chances are you’ll select to say no the phrases you have been provided and never proceed with opening the account. (Observe, nevertheless, that if you apply for a bank card, sometimes the account is mechanically opened if you get permitted for the cardboard.)

Sadly, even in case you didn’t really find yourself opening a brand new account, the truth that you utilized for credit score can nonetheless harm your rating. The exhausting inquiry nonetheless goes in your credit score report whether or not you opened an account with that lender or not.

When you solely utilized for one account, then your credit score rating will seemingly solely fall by a couple of factors, if in any respect. When you utilized for a number of accounts that you simply didn’t open inside the previous yr, nevertheless, it’s potential that you could possibly see an even bigger dip in your rating on account of all of these inquiries in your report.

-

You missed a fee a few times.

You may assume that lacking a fee right here and there may be not that large of a deal, however in actuality, it could possibly wreak havoc in your credit score rating. Recall that fee historical past is a very powerful issue contributing to your credit score rating, weighing in at 35% of your FICO rating.

If you’re 30 days late on making a fee even one time, this may have a big detrimental impact in your credit score, dropping your rating by as a lot as 60 to 110 factors.

When you nonetheless fail to make your fee by the next due date, you then get a 60-day late in your credit score report, which hurts your credit score much more.

30-day and 60-day lates are each thought-about minor derogatory objects in your credit score report, so that they received’t mess up your credit score as a lot as a serious derogatory merchandise.

Nevertheless, in case you get a 60-day late fee added to your credit score report, do your finest to make amends for funds earlier than one other 30 days cross, which is when issues get even worse.

-

You missed a fee for 3 months in a row or extra.

Lacking a fee even as soon as can severely set again your credit score rating, however the harm shall be even worse the longer you set off bringing the account present.

When you attain 90 days late on a credit score account, that’s now thought-about a serious derogatory merchandise, which is the worst potential sort of merchandise to have in your credit score report. (Different main derogatory objects embrace charge-offs, collections, foreclosures, settlements, judgments, repossessions, public information, and bankruptcies.)

Having a 90-day late in your credit score report is actually going to have a detrimental influence in your credit score. A credit score rating drop from a serious derogatory merchandise shall be much more extreme and tougher to get well from than that of a minor derogatory merchandise. As well as, the key derogatory merchandise may scare away potential lenders, making it more durable to acquire credit score sooner or later.

For extra info on main and minor derogatory objects and the way they’ll have an effect on your credit score, see “What Is a Derogatory Merchandise on Your Credit score Report?”

-

Certainly one of your accounts went into collections.

When you default on a debt, that means you didn’t fulfill your obligations to repay that debt, your creditor can promote your account to a set company, who will then attempt to gather the debt from you. A group account can be a serious derogatory merchandise in your credit score report, which implies it could possibly severely harm your rating you probably have an account go into collections.

Learn our article on collections in your credit score report to search out out every thing you’ll want to learn about assortment accounts.

-

You utilized for a number of bank cards in a brief time period.

Making use of for a number of bank cards leads to exhausting inquiries in your credit score report, which may have a extra important influence in your rating than only one inquiry.

Having too many exhausting inquiries in your credit score report in a brief time period signifies that you’re in search of loads of new credit score, which is a nasty signal to lenders, and it’ll carry down your rating.

With most credit score scoring fashions, inquiries for bank cards are all counted individually, even when they have been throughout the identical time. Since inquiries can every value your credit score rating as much as 5 factors, that may add up rapidly. (The exception to that is the VantageScore credit score rating, which counts all inquiries made inside a 14-day window of one another as one inquiry, no matter the kind of account.)

Moreover, in case you obtained permitted for and opened the entire accounts that you simply utilized for, then you could possibly additionally find yourself with too many new credit score accounts in your credit score report.

-

Certainly one of your bank cards was closed.

Many customers mistakenly consider the credit score fable that it’s going to assist their credit score in the event that they shut a few of their accounts. In a method, that is smart, as a result of it lowers the quantity of accessible credit score you have got, which reduces the potential quantity of debt you could possibly get into in case you have been to make use of all your accessible credit score.

Nevertheless, that isn’t how credit score scores work. Sadly, credit score scores don’t all the time make sense at first look.

We dispel this widespread false impression and extra in “Let’s Get to the Backside of These Credit score Myths.”

The reality is that closing an account nearly all the time hurts your credit score as a substitute of serving to it.

With revolving accounts, akin to bank cards, closing an account reduces your whole credit score restrict by eradicating the credit score restrict of that card. Whenever you scale back your credit score restrict, that motion will increase your general credit score utilization ratio, that means that you’re now utilizing a bigger fraction of your accessible credit score.

This hurts your credit score rating as a result of having a excessive credit score utilization ratio is penalized by the credit score scoring algorithms, whereas sustaining a low utilization ratio is rewarded.

The worst-case state of affairs to your credit score when closing an account is that if the account is closed whereas it nonetheless has a steadiness on it. On this case, that particular person account will appear to be it’s maxed out or over the restrict as a result of it has a steadiness however no credit score restrict. That alone is sufficient to considerably hurt your credit score, and the rise in your general utilization ratio solely worsens the issue.

Relying on what else is in your credit score file, closing a bank card may additionally negatively have an effect on your credit score combine, which may lead to a small credit score rating drop.

On the plus aspect, the rationale why an account was closed doesn’t play a job in your rating, so that you received’t be affected extra negatively if the cardboard was closed by the issuer than if it was closed at your request.

For extra details about closed accounts in your credit score report, see “How Do Closed Accounts Have an effect on Your Credit score?”

-

There was fraudulent exercise in your accounts.

Have you ever checked your bank card statements currently?

An surprising lower in your credit score rating may very well be the results of fraudulent exercise in your accounts.

When you see any fees in your assertion that you don’t acknowledge, then it may very well be fraudulent exercise that’s bringing down your rating. Maybe somebody was capable of get hold of your bank card info by phishing or via a knowledge breach and used it to run up the steadiness on the cardboard.

It’s necessary to watch your credit score accounts repeatedly so that you could catch any suspicious exercise early on. Higher but, arrange electronic mail or cell notifications in your account that can warn you to fraudulent exercise immediately.

If a prison does handle to get entry to your account, report the fraudulent fees to your bank card issuer instantly and ask to have the fees reversed. Most bank card firms have a zero legal responsibility coverage, which implies you received’t be held chargeable for paying for any of the fraudulent fees.

-

You paid lower than the minimal fee.

In case your money stream is tight, it may be tempting to ship the financial institution or bank card firm a partial fee as a substitute of the complete quantity that’s due that month. You could assume that it’s not as large of a deal as not paying in any respect, as a result of not less than you’re sending them a few of the cash.

Sadly, it doesn’t work that method. If you don’t cowl the complete minimal fee by the due date, it won’t be counted as an on-time fee.

When you can carry the account present earlier than 30 days cross, you should still must cope with a late price out of your bank card issuer (though it’s value asking them to waive the price), however not less than the late fee won’t present up in your credit score report.

However, if you don’t make a ample fee and 30 days go by, then you’ll have a late fee pop up in your credit score report, which may undoubtedly take a toll in your credit score rating.

To stop this from occurring, as quickly as you understand you will be unable to make the complete fee, contact your bank card issuer and ask if they’ve a monetary hardship program or attempt to negotiate an association with them that lets you pay what you’ll be able to with out damaging your credit score.

-

You didn’t use your bank card for a very long time.

Your bank card issuer may need closed your account if it had been inactive for a very long time.

When you don’t use a bank card for a protracted time period, it’s potential that your bank card issuer might determine to shut your account as a result of lack of exercise.

As we mentioned above, a closed bank card is unhealthy information to your credit score for the reason that lack of accessible credit score hurts your credit score utilization and it might additionally harm your mixture of credit score.

In accordance with The Stability, the bank card firm will not be required to provide you advance discover in the event that they plan to shut your account, so it’s finest to take proactive measures to stop this from occurring.

To keep away from having your card closed attributable to inactivity, ensure you use it to make a purchase order not less than as soon as each few months. A simple method to do that is to make use of the bank card to pay for a subscription service that renews every month. Then, arrange automated invoice funds in your bank card and the entire course of shall be automated.

-

You completed paying off an installment mortgage.

Making the ultimate fee in your auto mortgage, scholar loans, or mortgage is an thrilling accomplishment. But, if you end paying off an installment mortgage, your credit score rating might lower as a substitute of enhance.

Despite the fact that you now have much less debt, which feels like it might assist your credit score rating, this may occasionally not outweigh the detrimental influence in your mixture of credit score. The paid-off installment mortgage will now report as a closed account, which might be dangerous to your credit score if all you have got left is a couple of revolving accounts.

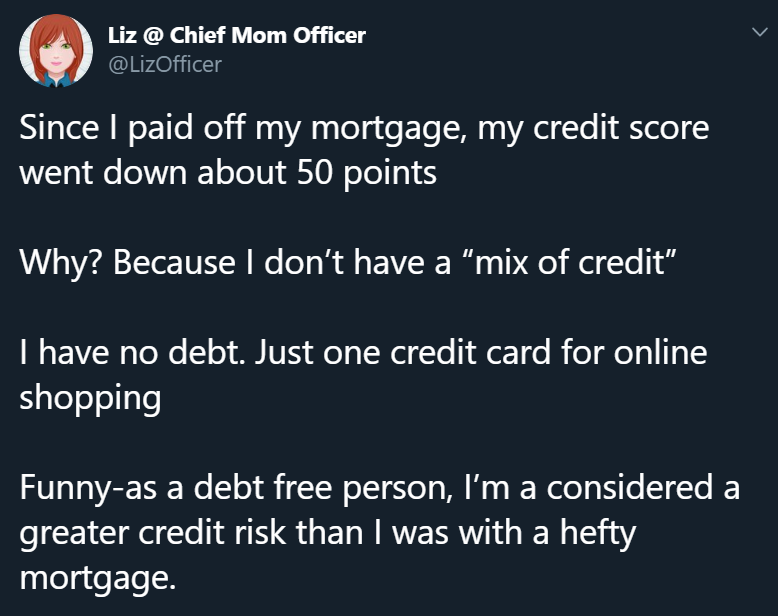

@LizOfficer shared a real-life instance of this on Twitter.

This Twitter person commented that paying off her mortgage made her credit score rating go down because it affected her mixture of credit score.

-

An account that you’re piggybacking on turned delinquent.

Typically being a licensed person on a bank card or having a joint account is usually a dangerous factor. You might be counting on the opposite individual to pay their payments on time and to handle their balances properly, in any other case, their habits can compromise your credit score.

In different phrases, a great tradeline ought to have a low utilization ratio, it ought to have the next age than your common age of accounts and your oldest account, and most significantly, it must have a good fee historical past.

Due to this fact, you need to keep away from being added as a licensed person to a tradeline that has any derogatory marks on it in order that these derogatory objects don’t get added to your credit score file and find yourself damaging your credit score.

That’s the hazard of piggybacking on a good friend or member of the family’s bank card—even when the tradeline is ideal if you find yourself first added to it, there’s no assure that it’s going to keep that method.

In case your licensed person tradeline does get any missed funds on its document, that would undoubtedly harm your credit score, and it might be sensible to take away your self from it instantly. To take action, merely name the bank card issuer and request to be faraway from the account, as most banks let you do that without having to undergo the first account holder.

Delinquency on the a part of the first account holder could cause issues in case you are piggybacking on another person’s credit score account.

Chapter is likely one of the worst issues you’ll be able to have in your credit score report. Since declaring chapter basically means you’re asking to be launched from the authorized obligation to repay your money owed, it reveals lenders that you’ve a particularly excessive threat of defaulting sooner or later, so it could possibly have a extreme detrimental influence in your credit score rating.

-

There are inquiries in your credit score file that you simply didn’t authorize.

Unauthorized inquiries in your credit score file can unfairly drag down your credit score. In our article on credit score inquiries, we reported that every exhausting inquiry in your credit score report can doubtlessly value you as much as 5 factors every.

Luckily, you have got the appropriate to dispute any exhausting inquiries in your credit score report that you simply didn’t authorize. You’ll be able to study extra in regards to the credit score dispute course of in “Find out how to Repair the Most Widespread Credit score Report Errors.”

-

Your credit score file obtained merged with another person’s.

Typically inaccurate info can get in your credit score report not on account of fraud or as a result of your lender reported it incorrectly, however as a result of your credit score file unintentionally turned combined with the knowledge of one other individual.

That is known as a “combined credit score file” or “combined credit score report” and it often happens with two customers who’ve related names.

If the credit score historical past of the opposite shopper with whom your file has been combined comprises detrimental info, that might clearly be detrimental to your rating, and also you would wish to right the state of affairs by submitting a dispute with the credit score bureau.

That is an instance of why it’s necessary to examine your credit score report repeatedly. If there may be incorrect info in your credit score report that ought to be eliminated, you don’t need to discover out about it if you’re making an attempt to use for credit score. You have to catch and right credit score report errors early in order that they don’t stand in the best way of you attaining your monetary targets.

-

You maxed out a number of of your bank cards.

Credit score utilization makes up almost a 3rd of your FICO rating, which implies it’s critically necessary to maintain your utilization low if you wish to preserve a excessive credit score rating. Maxing out even only one bank card can have a big detrimental influence, and in case you max out a number of playing cards, you’ll be even worse off.

Take a look at our article on utilization ratios for tips about how one can preserve your utilization fee at an optimum stage.

-

Somebody opened an account in your title.

An account in your credit score report that you simply don’t acknowledge may very well be an account that another person fraudulently opened in your title.

We already lined how opening a brand new account can negatively have an effect on your credit score initially, however don’t neglect that the identical factor can occur if another person makes use of your title to enroll in a brand new account.

When you see that your credit score rating has decreased, check out the inquiries and accounts in your credit score report back to see if there are any objects that shouldn’t be there.

-

You may have “double jeopardy” with assortment accounts in your credit score report.

Debt assortment companies are usually not recognized to be essentially the most reliable entities and sometimes should not have the very best practices in the case of protecting observe of money owed and contacting customers. Info usually will get misplaced or misrecorded when it’s transferred between collectors and generally quite a few assortment companies.

Due to this, some customers discover themselves with multiple entry for a similar open assortment account on their credit score report, which is called “double jeopardy.”

Whereas the identical assortment could also be listed a number of occasions as a result of account altering fingers, solely the entity who presently owns the debt ought to be reporting the account as open.

Luckily, if a set is being reported in error, you’ll be able to dispute the wrong info and have the knowledge be corrected or doubtlessly eliminated altogether.

-

Your credit score report says you missed a fee regardless that you paid on time.

Dispute any mistakenly reported late funds in order that they don’t unfairly have an effect on your credit score rating.

Since fee historical past is a very powerful consider your credit score rating, an incorrectly reported missed fee may severely harm your credit score, particularly in case you are beginning with superb credit score. The upper your rating to start with, the extra you stand to lose from a credit score mistake.

The sort of state of affairs is one other instance that demonstrates why it’s so essential to repeatedly examine your credit score report. When you all the time made all your funds on time, you may assume that you will need to have a spotless credit score document, solely to search out out at an inconvenient time {that a} creditor has been incorrectly reporting that you simply missed a fee.

Preserve a watch out for errors like this in your credit score report so that you could dispute them instantly.

-

Your bank card issuer lowered your credit score restrict.

Typically, bank card issuers decrease the credit score limits of their cardholders, even for individuals who have constantly managed their accounts responsibly.

Sadly, they’re often allowed to do that with out asking to your permission or letting you understand prematurely, so it might come as a nasty shock if you swipe your bank card and get declined, or when your credit score rating takes a dive as a result of your credit score utilization is all of the sudden a lot greater.

There are a couple of the explanation why your financial institution might scale back your credit score restrict, akin to the next:

Bank card issuers generally reduce bank card limits, which hurts your credit score utilization ratio.

- Your balances have been growing, which signifies that you’re taking up extra debt and may be at a higher threat of defaulting.

- You missed a fee and your account turns into delinquent.

- Your account was inactive since you didn’t use your bank card sufficient.

- The economic system is down and lenders need to reduce their threat publicity ranges.

No matter why your credit score restrict took successful, the consequence is similar: with much less accessible credit score, your credit score utilization will increase, which is unhealthy to your rating.

In case your bank card issuer slashed your credit score restrict, try “Find out how to Improve Your Credit score Restrict” for some helpful suggestions, and don’t be afraid to provide your financial institution a name to ask them to rethink.

-

A group account was deleted out of your credit score report.

Surprisingly, it’s really potential that getting a set account eliminated out of your credit score report may make your credit score rating go down as a substitute of up.

We discuss this in higher element in “Assortment Accounts on Your Credit score Report: The Final Information” and “What Are Credit score Scoring ‘Buckets?’” by credit score skilled John Ulzheimer, however the primary concept is that there are completely different credit score scoring “buckets” which have barely completely different strategies of calculating credit score scores for the customers inside every bucket.

By eradicating a set account out of your credit score report, it’s potential that you could possibly transfer from one bucket into one other bucket the place your rating will now be calculated in another way. Because of this new algorithm being utilized to your credit score report, your rating may develop into decrease than it was if you have been within the first bucket.

-

You haven’t used any credit score in a very long time.

If in case you have used credit score up to now however not lately, a few of your previous accounts might have fallen off of your credit score report altogether. Accounts which are closed or inactive don’t stay in your credit score report endlessly. Constructive accounts will usually keep in your credit score report for 10 years, whereas detrimental accounts might keep in your credit score report for as much as 7 years.

When these previous accounts age off of your credit score report, you lose the entire credit score historical past related to them, a very powerful of which is the fee historical past. Since you are shedding precious credit score historical past, your rating may take successful.

These with skinny credit score information or those that haven’t used credit score in a number of years might want to give attention to constructing credit score to ensure that their credit score rating to get well.

Conclusions

In terms of your credit score rating, minor fluctuations are regular, so there’s usually no want to stress about shedding a couple of factors right here and there.

If you’re practising good credit score habits and paying all your payments on time, it’s most likely not vital to observe your credit score like a hawk and examine your rating each single week, and a change of some factors in both course shouldn’t trigger you to panic.

Nevertheless, as we’ve got seen, you don’t need to neglect your credit score completely, since errors can and do occur.

As well as, remember that credit score strikes can generally have surprising outcomes, significantly in circumstances the place chances are you’ll be migrating from one credit score scoring “bucket” to a different.

When you see a big drop in your credit score rating, that’s undoubtedly value investigating additional so that you could perceive why it occurred, handle the problem, and hopefully get a few of these credit score rating factors again.

[ad_2]

Source link

{kind=link}