[ad_1]

How usually does the earnings tax popping out of your paycheck preserve you up at night time? Okay, now how usually do you’re feeling burdened about your six-figure student debt?

Chances are high your scholar debt is creating much more stress in your life than your taxes. In truth, paying extra taxes can typically “really feel good” as a result of it means you’re making more cash.

What if you considered your scholar loans that means, too? What in case your mindset was that the coed loans opened up the chance to get a greater schooling, earn extra earnings, and pursue a profession that you just’re obsessed with?

It is likely to be a leap in pondering at first, however we will get there.

To begin, you’ll have to unravel scholar debt from different kinds of debt. Federal scholar mortgage guidelines and reimbursement plans are completely different than different kinds of debt.

Bank card debt, a automobile mortgage, a private mortgage, and your mortgage have to be paid off in full it doesn’t matter what. Their funds are additionally based mostly on how a lot you owe.

However federal scholar mortgage debt has completely different guidelines of engagement. Not solely can your schooling result in larger earnings, however income-driven reimbursement plans could make mortgage reimbursement function extra like a tax than a debt.

Let’s look at this concept additional beginning with learn how to calculate scholar mortgage funds.

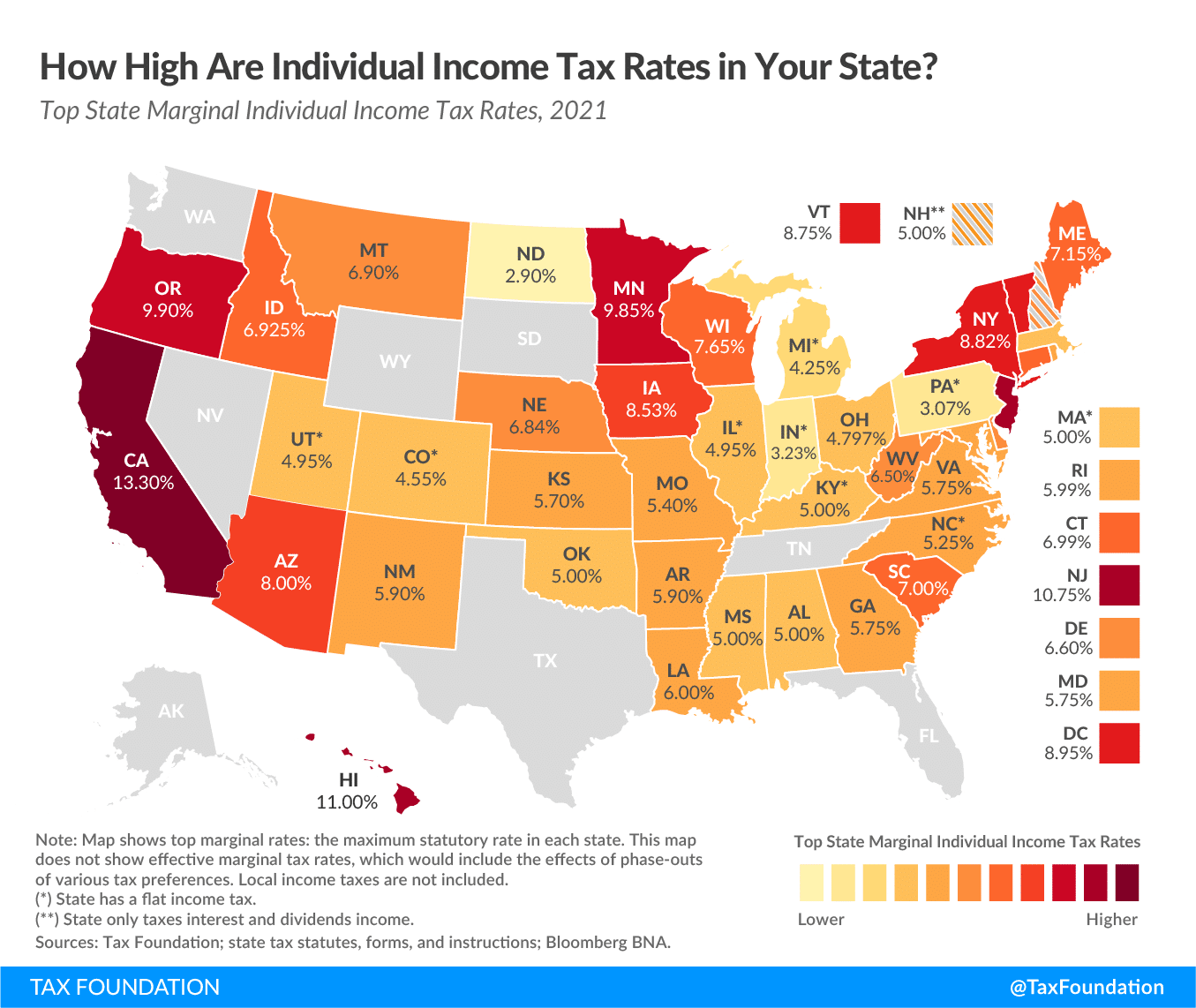

Would you progress to a distinct state simply to save lots of on taxes?

Most of us don’t select the place we reside due to the tax fee within the state. We’re extra prone to reside in a state that gives the life-style, job and household life we need to have.

Regardless of the state earnings tax occurs to be, it’s what it’s. We simply take care of it. Typically we don’t even give it some thought.

If we did select the place we lived based mostly upon the state’s tax fee, nobody would reside within the states with the best state earnings tax — particularly, California, New York, Oregon, New Jersey, Arizona, Hawaii, Minnesota, Vermont or Iowa.

We’d all reside within the eight states with no earnings tax, like Washington, Nevada, Texas, Florida, Tennessee, South Dakota, Wyoming or Alaska.

Regardless of its excessive taxes, some folks transfer to California for the nice climate. Some transfer to New York for the hustle, bustle and tradition of an enormous metropolis. Folks select to reside there regardless of the taxes.

The identical might be true of getting a graduate diploma.

Whether or not you went to high school to be a physician, dentist, pharmacist, veterinarian, chiropractor, lawyer, psychologist, social employee, or different graduate-level skilled, you’ll in all probability select it as a result of it’s a rewarding profession path for you.

Pupil loans are a byproduct of that call to have a satisfying profession path.

When you’ll be able to consider your scholar loans as a tax as a substitute of a debt, your mindset can shift to:

“I really like my job and am making more cash due to it, too. It’s price it to pay an additional tax within the type of scholar mortgage funds to reside the life I need.”

Let’s begin by understanding learn how to calculate your student loan payments, then undergo why they are often regarded as a tax.

How scholar mortgage funds are calculated

If in case you have federal scholar loans, you’ll be able to pay them again with one in every of two methods:

- Pay based mostly on how a lot you owe: Commonplace Plan, Prolonged Plan, and Graduated Plans

- Pay based mostly on how a lot you make: Earnings-driven reimbursement plans, like Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE) and Earnings-Primarily based Compensation (IBR)

The funds based mostly on how a lot scholar debt you owe are calculated similar to every other debt. The extra you owe, the upper your funds.

However income-driven reimbursement is completely different. Your discretionary income determines your funds and works as an schooling tax of kinds.

For those who’re on PAYE or REPAYE, your funds are 10% of your discretionary earnings. If you choose IBR, then your funds will likely be 15% of discretionary earnings.

Discretionary earnings

Discretionary earnings is the calculation used to find out your income-driven reimbursement plan cost. That is essential as a result of that quantity is multiplied by 10% or 15% to provide you with your income-driven cost quantity, similar to an earnings tax.

Discretionary earnings begins along with your adjusted gross earnings (AGI) out of your tax return. AGI is calculated by beginning along with your earnings from all sources (together with funding or rental earnings) after which subtracting sure deductions.

The key ones for most individuals are pre-tax retirement plan contributions and well being financial savings account (HSA) contributions.

Be aware: The usual deduction or different itemized deductions (mortgage curiosity, private charitable contributions) come after AGI and don’t have an effect on your scholar mortgage funds.

Maintaining it easy, let’s say that somebody incomes $100,000 in wage contributes $10,000 to their pre-tax retirement account via work. Their AGI can be $90,000.

Then, take your AGI and subtract 1.5x the federal poverty degree (FPL). Consider the FPL deduction as a normal deduction to decrease your earnings and scholar mortgage cost.

For 2021, the FPL for a single individual is $12,880. That’s a $19,320 deduction towards AGI.

So the discretionary earnings for a single individual making $100,000 and contributing $10,000 to a pre-tax retirement plan can be $70,680. That’s the quantity used to calculate scholar mortgage funds.

The FPL goes up $4,540 per member of the family (partner, children). Meaning the discretionary earnings deduction would go up by $6,810 per member of the family. If that very same individual was in a household of 4, their discretionary earnings can be $50,250.

Consider the FPL deduction as your normal deduction or itemized deductions to get to your calculated earnings tax fee.

Instance of scholar loans as an earnings tax

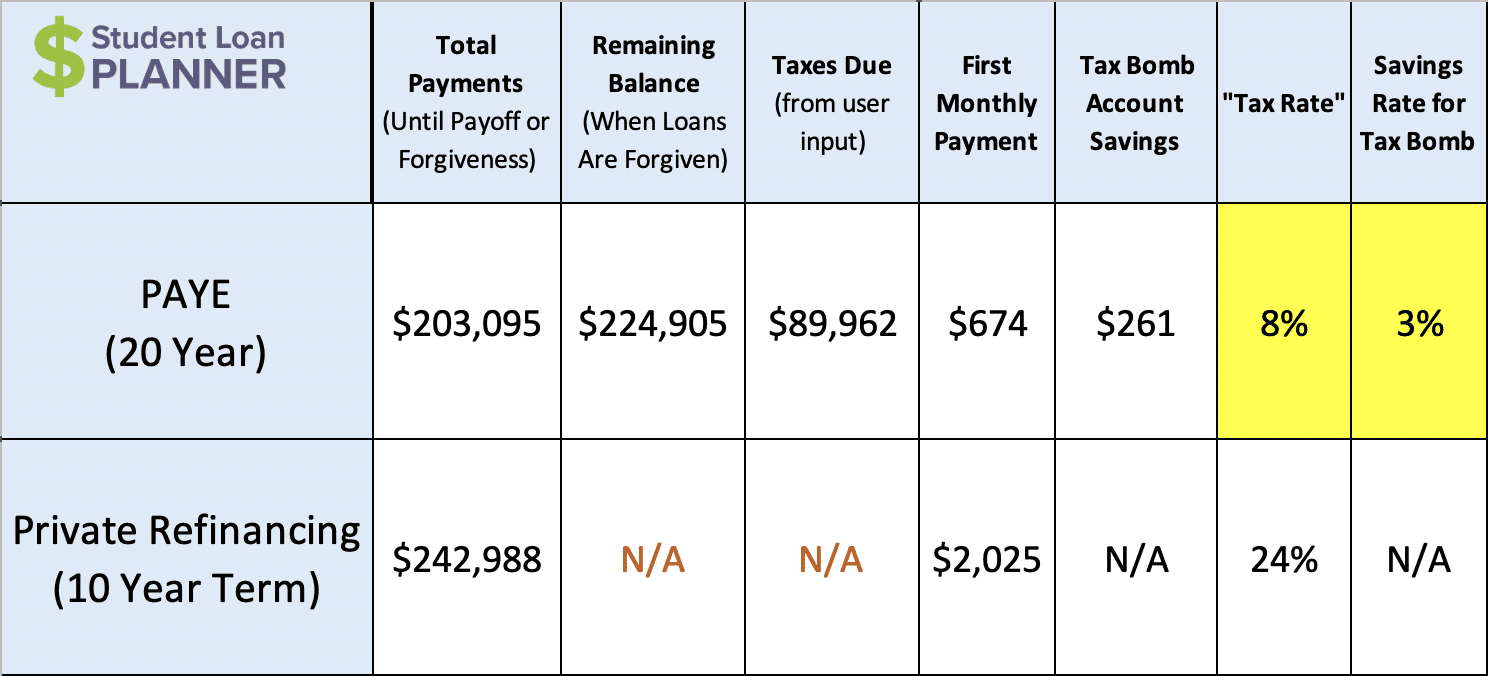

Emily’s a veterinarian making $100,000 and has $200,000 in vet faculty debt at 6.8%. She’s obsessed with veterinary drugs, however her scholar debt is actually weighing on her and making her query if she made the appropriate alternative.

She’s making an attempt to determine whether or not she ought to pay again her loans in full by paying $2,000 per thirty days or go on PAYE the place her funds are based mostly on her earnings.

If we simply take a look at this as a debt on PAYE, Emily will make $203,095 in funds over 20 years after which have a $89,962 tax bomb in 20 years. These are massive numbers and add to her stress degree as a result of it looks as if an infinite mountain to climb.

But when we break it down and say that her PAYE funds are like an 8% tax for 20 years of funds on PAYE and three% for the tax bomb financial savings, that’s completely different. Primarily her scholar loans go from a $200,000 debt to an 11% schooling tax that she’d pay for 20 years.

I may ask Emily, “Would you pay 11% extra in taxes to make $100,000 doing what you’re keen on?” That’s lower than what somebody dwelling in New York Metropolis pays between state and native taxes (12%+)!

She will simply set her funds and automate her tax bomb financial savings and consider it like month-to-month taxes she has to pay. That’s significantly better than having the burden of paying $2,000 per thirty days for 10 years the place she’d be locked right into a sure job to ensure she will make the funds.

She will actually select the job she likes essentially the most whether or not it pays kind of than what she’s making, and her scholar mortgage tax will alter up or down along with her earnings.

If she earns $75,000 or $125,000, her funds would go up and down along with her earnings similar to a tax. Nevertheless, her “tax fee” stays about the identical at 11%.

If she decides to take a number of months off to discover choices, she will alter her funds to $0 per thirty days. No earnings, no scholar mortgage cost “tax”. She will even take a break from the tax bomb financial savings and ramp again up after.

Pupil mortgage tax for top debt-to-income debtors

Having an excellent excessive debt-to-income ratio can really feel mentally debilitating. Watching these loans proceed to develop might be disheartening. Nevertheless it doesn’t need to be that means. Even a excessive scholar debt-to-income might be regarded as a tax, too.

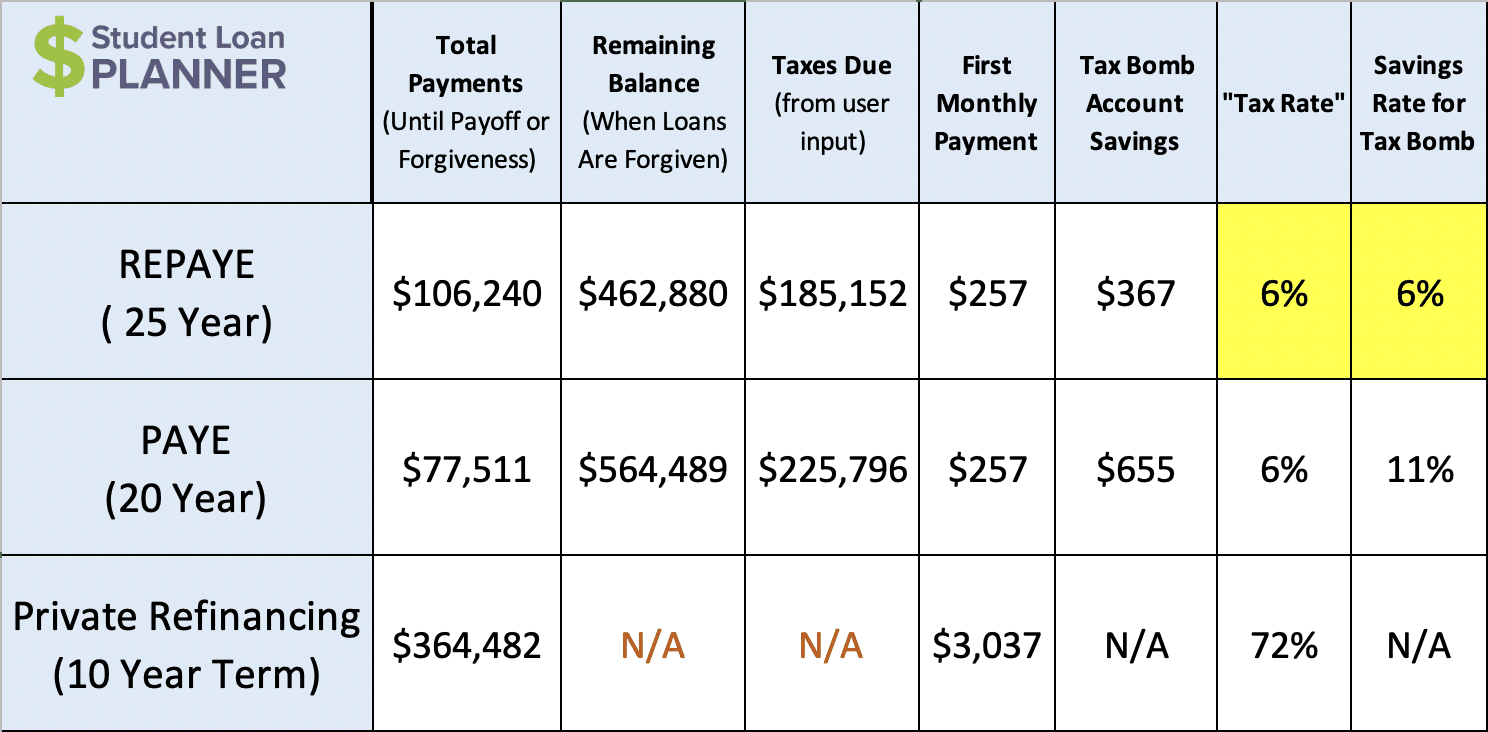

Let’s say that Tina has $300,000 of debt and is making $50,000 as a chiropractor. That’s a 6:1 debt-to-income ratio.

Paying off her loans in full can be a large hurdle as a result of the funds can be about $3,000 per thirty days for a 10-year time period and round $1,900 for a 20-year time period. Both choice would eat up most of her take-home pay.

The loans are inflicting Tina nice stress, as a result of she’s undecided learn how to handle them. But when she seems to be at income-driven reimbursement as a tax, then she has reasonably priced reimbursement choices to really feel higher.

Slightly than making an attempt to determine learn how to make a big month-to-month cost from $2,000 to $3,000, she will go on REPAYE and earmark $624 per thirty days to go towards her loans, $257 for the cost, and $367 for the tax bomb financial savings.

That equates to a scholar mortgage “tax” of 12% (6% for the cost, 6% for the tax bomb financial savings) which is lower than dwelling in California or New York Metropolis.

If she automates her scholar mortgage cost and likewise her tax bomb financial savings, it’ll depart proper after it hits her checking account just like a tax withholding. She gained’t even miss it.

Tina can sleep higher at night time after shifting her mindset from the coed loans being this heavy debt burden to an reasonably priced tax.

Are her loans enjoyable to have a look at now? In fact not. Does it trigger a substantial amount of stress reduction to shift her mindset? Completely.

You don’t need to really feel caught in a job due to scholar debt

What if chiropractic drugs isn’t figuring out for Tina and he or she decides to take one other profession path?

Nicely, when she thinks of the coed loans as a tax, she will have the liberty to pursue no matter she needs. Perhaps she finds one other job that pays $75,000. She will take it. What a couple of profession change to one thing like knowledge analytics? She will make that change, too.

As she makes kind of cash, her funds will alter accordingly till she reaches mortgage forgiveness. The reimbursement technique and tax might be constructed round no matter profession or life selections she chooses.

Must you make much less cash to pay much less scholar mortgage tax?

Heck no!

I usually get this query throughout a scholar mortgage seek the advice of. By no means take a lower-paying job simply to get decrease scholar mortgage funds.

Sure, your funds will go up as you make more cash, however wouldn’t you be prepared to pay $2,000 because of incomes an additional $20,000? I do know I’d as a result of my take-home pay after scholar mortgage funds would nonetheless have a very nice enhance.

Apart from, if you happen to’re frightened about making extra and paying extra in your income-driven funds, then simply put more cash away into your pre-tax retirement account or HSA. That can decrease your AGI → discretionary earnings→ scholar mortgage cost whereas serving to you construct an superior nest egg.

Pupil loans don’t need to be a burden

For those who’re battling anxiousness as a result of your debt otherwise you’re undecided what to make of this complete “scholar loans as a tax” factor, be at liberty to succeed in out.

We are able to look at your scholar mortgage scenario and present you the clear path ahead, a path that empowers you to place your profession and life objectives first and match a scholar mortgage reimbursement technique round that. Pupil loans don’t have to regulate your life.

Let’s get you again within the driver’s seat. Study extra about how our consult process works — we’re right here to assist.

Refinance scholar loans, get a bonus in 2021

$1,000 BONUS1For 100k or extra. $200 for 50k to $99,999¹

$1,050 BONUS2For 100k+. $300 bonus for 50k to 99k.2

$1,250 BONUS3For 250k+, tiered 300 to 500 bonus for 50k to 250k.3

$1,275 BONUS4For 150k+. Tiered 300 to 575 bonus for 50k to 149k.4

$1,000 BONUS5For $100k or extra. $200 for $50k to $99,9995

$1,250 BONUS6For 100k+ or $350 for 5k to 100k.6

$1,250 BONUS7For 150k+. Tiered 100 to 400 bonus for 25k to 149k.7

Unsure what to do along with your scholar loans?

Take our 11 query quiz to get a personalised suggestion of whether or not it’s best to pursue PSLF, IDR forgiveness, or refinancing (together with the one lender we predict may provide the finest fee).

1Earnest: $1,000 for $100K or extra, $200 for $50K to $99.999.99. For Earnest, if you happen to refinance $100,000 or extra via this website, $500 of the $1,000 money bonus is supplied straight by Pupil Mortgage Planner. Charge vary above contains elective 0.25% Auto Pay low costEarnest disclosures.

2Commonbond: For those who refinance over $100,000 via this website, $500 of the money bonus listed above is supplied straight by Pupil Mortgage Planner. Commonbond disclosure.

3Laurel Street: For those who refinance greater than $250,000 via our hyperlink and Pupil Mortgage Planner receives credit score, a $500 money bonus will likely be supplied straight by Pupil Mortgage Planner. In case you are a member of knowledgeable affiliation, Laurel Street would possibly give you the selection of an rate of interest low cost or the $300, $500, or $750 money bonus talked about above. Affords from Laurel Street can’t be mixed. Charge vary above contains elective 0.25% Auto Pay low cost. Laurel Road disclosures.4Elfi: For those who refinance over $150,000 via this website, $500 of the money bonus listed above is supplied straight by Pupil Mortgage Planner. Elfi disclosure. 5Sofi: For those who refinance $100,000 or extra via this website, $500 of the $1,000 money bonus is supplied straight by Pupil Mortgage Planner. Charge vary above contains elective 0.25% Auto Pay low cost. Sofi disclosures. 6Credible: For those who refinance over $100,000 via this website, $500 of the money bonus listed above is supplied straight by Pupil Mortgage Planner. Credible disclosure.

7LendKey: For those who refinance over $150,000 via this website, $500 of the money bonus listed above is supplied straight by Pupil Mortgage Planner. Charge vary above contains elective 0.25% Auto Pay low cost.

[ad_2]

Source link

{kind=link}