[ad_1]

Loyalty? Not within the mortgage enterprise. That’s, if you happen to really need to get monetary savings on your private home mortgage.

A couple of years again, an HSBC survey revealed that 52% of U.S. owners “switched suppliers” (sorry, they’re British) when acquiring subsequent mortgages.

This was primarily pushed (53%) by the will to get a greater deal, aka a lower mortgage rate with fewer closing prices.

That survey additionally discovered that 46% of shoppers investigated a mortgage switcheroo, once more both to save cash or to lock in a brand new low price as a result of rising rates of interest.

Different causes owners determined to go together with one other mortgage firm had been as a result of they moved and bought a brand new property.

Or as a result of their present mortgage deal was expiring. I believe they imply an adjustable-rate mortgage resetting.

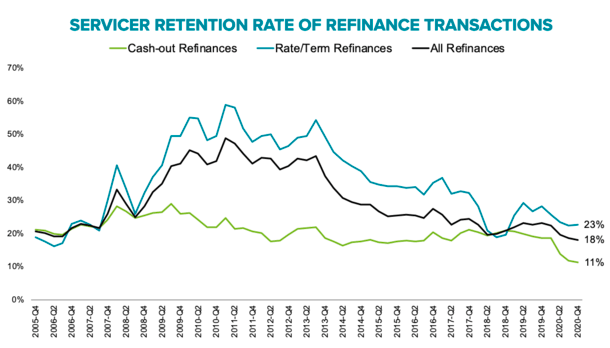

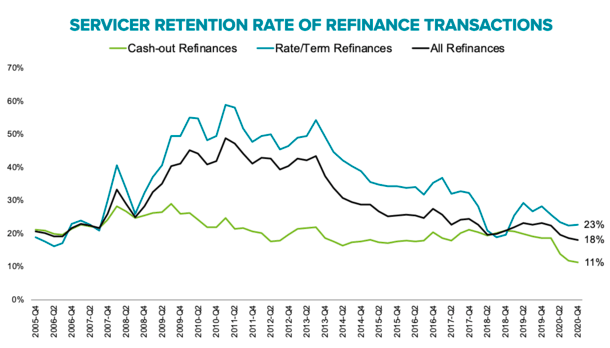

Mortgage Lender Retention Hits a Report Low

Now a brand new report from Black Knight claims that mortgage servicers retained simply 18% of the estimated 2.8 million owners who refinanced a mortgage within the fourth quarter of 2020, the bottom share on file.

Apparently, those that refinanced to enhance their price and/or time period had been retained at a better price (23%) versus these pulling cash out as a part of the transaction (11%).

This may very well be as a result of money out refinances being more durable to come back by currently, and thus provided by fewer lenders.

However right here’s the biggie – amongst higher-credit high quality price and time period refinances, debtors who switched mortgage lenders acquired greater than an eighth of a % decrease price than those that refinanced and remained with their present lender/servicer.

In different phrases, you may get a decrease mortgage price if you happen to change mortgage lenders, as an alternative of remaining loyal.

Mortgages Are Largely a Commodity

- House loans aren’t all that totally different from each other

- Which is why lenders are more and more developing with distinctive methods to promote you one

- The overwhelming majority are 30-year mounted merchandise whose solely distinction is likely to be the rate of interest or charges concerned

- And the bulk simply observe the underwriting tips of Fannie Mae, Freddie Mac, or HUD

It’s actually no shock that a whole lot of shoppers don’t stick with their unique mortgage lenders and/or loan servicers.

Apart from some present lenders generally talking borrowers out of a refinance, the product is generally the identical irrespective of the place you get it.

That makes buyer retention tough, particularly when different lenders are aggressively advertising to owners.

As of late, nearly all of dwelling loans are backed by the company tips of Fannie Mae, Freddie Mac, or the federal government by way of FHA loans and VA loans. I believe it’s one thing like 90% of mortgages.

This implies mortgage loans are fairly homogeneous, regardless of what channel they’re originated in, or which establishment supplies the financing.

You can get the identical actual dwelling mortgage from a neighborhood credit score union, a giant financial institution, a web based mortgage banker, or a mortgage broker.

And who actually cares the place you get your mortgage so long as the corporate is competent sufficient to shut the factor, and trustworthy by way of price and costs?

It’s not such as you’re going to stroll round and brag about your cool mortgage from X financial institution after the very fact. It’s definitely not a standing image, or a conspicuous transaction.

I’m fairly certain I’ve by no means had a dialog about somebody’s branded mortgage earlier than.

And I doubt an “influencer” goes to publish about theirs on Instagram. Properly, I take that again, they may…as a result of somebody paid them.

Mortgage Promoting Is Following the Insurance coverage Mannequin

- Most types of insurance coverage are equally boring and unoriginal

- However that doesn’t cease insurers like Geico from promoting 24/7

- And creating catchy names for run-of-the-mill choices that aren’t totally different from firm to firm

- Mortgage lenders are starting to do this too in a bid to separate themselves from the gang

That is precisely why insurance coverage firms use superstar endorsements and sensible advertising gimmicks to get you to modify, or conversely, to stay round.

Automobile insurance coverage isn’t cool or thrilling and by no means shall be, nor are mortgages, as a lot as I would like them to be.

In the end, we’re all being bought the identical factor, it’s simply that some firms attempt to differentiate themselves by slapping intelligent names onto their merchandise.

For instance, Quicken Mortgage’s Rocket Mortgage is about reinventing the mortgage course of, not the mortgage itself.

You’re nonetheless most likely going to get a 30-year fixed home loan or another extraordinary mortgage that you’d get wherever else.

It’s simply the way in which you get it which may change. As a substitute of assembly face-to-face with a banker, you may add paperwork in your smartphone and authorize the discharge of paperwork electronically.

This might make the expertise lots simpler and extra nice, nevertheless it doesn’t imply you’re essentially getting something totally different.

As a result of everyone seems to be principally providing their prospects identical factor, it comes down to cost, customer support, and now maybe intelligent advertising.

The one exception is portfolio home loan programs, which are literally distinctive to the mortgage lender offering them. These are loans saved on the originating financial institution’s books that include distinct underwriting tips.

We’re beginning to see extra of them, although most lenders stay pretty cautious with the mortgage disaster nonetheless a not-too-distant reminiscence, regardless of going down a decade in the past.

For instance, a whole lot of the zero down mortgages you see are distinctive to the businesses providing them, the newest one I got here throughout from Ideal Credit Union.

And a few of the so-called fintech disruptors like SoFi Mortgage are literally offering distinctive choices like a 5/1 ARM with an interest-only possibility and jumbo loans as excessive as $3 million with simply 10% down.

Be Cautious To not Pay Extra for the Identical Precise Mortgage

- Whereas it’s essential to make use of a mortgage lender you’ll be able to belief

- One that may really shut your private home mortgage competently at once

- It doesn’t actually matter what “model” the mortgage it’s

- And there’s a superb probability it’ll be resold shortly after closing anyway

These exceptions apart, many people have very related mortgages which are solely distinctive by way of the place they originated from.

As famous, most of in the present day’s mortgages are conforming loans, that means they meet the rules of Fannie and Freddie. Or they’re merely backed by the federal government by way of the FHA, VA, or USDA.

And nearly all of them are 30-year fixed-rate loans that perform precisely the identical.

That’s why you need to ask your self – if the corporate isn’t providing something totally different, why pay extra?

May as nicely discount store and discover the perfect mortgage price with the bottom closing prices, as an alternative of merely going with a family title due to a humorous business.

On the finish of the day, so long as they get you to the end line, you’ll most likely by no means take into consideration your mortgage firm once more. Simply make sure that they’re respected first…

Likelihood is your mortgage shall be bought off in a matter of months anyway, so the corporate you get it from doubtless received’t even service it.

In truth, your last correspondence is likely to be a discover of your private home mortgage altering arms…

(picture: lamdogjunkie)

[ad_2]

Source link

{kind=link}