[ad_1]

Mortgage charges might shock us this week

Debtors and consultants alike have been eyeing this week’s Federal Reserve assembly as a key second for mortgage charges.

The Fed is expected to announce on Wednesday that it’ll begin “tapering” its Covid-era bond-buying program, which has been maintaining mortgage charges low over the past 12 months and a half.

In concept, meaning charges ought to go up. However there’s a catch.

We’ve identified in regards to the Fed’s plans for some time now. So the announcement received’t come as a shock.

And meaning — opposite to standard perception — we might not see a big rate spike after the Federal Reserve assembly, if any in any respect.

Find your lowest mortgage rate. Start here (Nov 2nd, 2021)

Is the Fed going to boost rates of interest this week?

Within the easiest phrases, no. The Federal Reserve does not set mortgage rates, and it doesn’t have the facility to boost or decrease them at will.

Nonetheless, the Fed does have two levers with which it might affect mortgage rates of interest:

1. The federal funds fee

The federal funds fee is the rate of interest at which banks lend to at least one one other in a single day. Mounted mortgage charges usually are not based mostly on the fed funds fee or tied to it in any means — though they are often not directly influenced by it. So when the Fed raises its benchmark fee, mortgage charges simply would possibly tag alongside.

Nonetheless, the Federal Reserve has indicated it doubtless received’t improve its benchmark fee till 2022 at the earliest. So consultants usually are not anticipating large information on the speed entrance at this week’s Fed assembly.

2. The Fed’s bond-buying program

In contrast to the fed funds fee, the Federal Reserve’s bond-buying program has a direct impression on mortgage fee developments.

Because the starting of the pandemic, the Federal Reserve has been shopping for $40 billion monthly in mortgage-backed securities (MBS). MBS are a sort of bond that helps determine mortgage interest rates.

By maintaining demand for MBS artificially excessive, the Fed has pressured mortgage charges to remain low in the course of the Covid pandemic.

However now that the economic system is on a path to restoration, the Fed has decided it’s time to begin pulling again on this stimulus program. This course of is called “tapering” — a phrase you’ve doubtless heard for those who’ve been following mortgage charges over the previous few months.

Why we would not see an enormous fee spike after the Fed assembly

Most rate-watchers predict a proper announcement about when the Fed will begin tapering its bond-buying program after this week’s Fed assembly.

In concept, an official begin to tapering ought to result in greater charges for residence patrons and owners.

That’s what happened when the Fed ended the same program in 2013.

However the Federal Reserve has been cautious this time round.

Fed Chair Jerome Powell has been upfront in regards to the central financial institution’s plan to begin pulling again on stimulus earlier than the tip of the 12 months. And meaning this week’s tapering announcement — if it occurs — received’t be a shock.

Remember that mortgage charges are decided by buyers. And buyers typically act based mostly on what they count on the market to do.

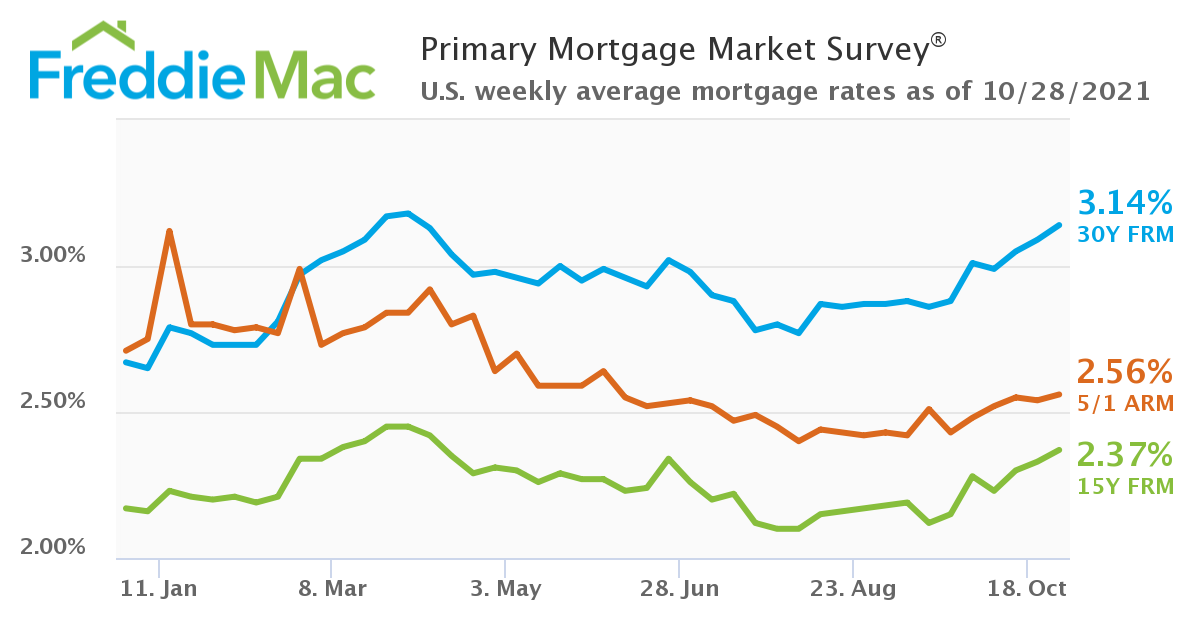

So there’s a very good probability the Fed’s tapering plans have already been priced into today’s mortgage rates. Certainly, common charges have elevated considerably over the previous few weeks main as much as the Federal Reserve assembly:

Supply: Freddie Mac

So we would not see an enormous improve after the assembly, as many consultants have been predicting.

Don’t get complacent — greater charges are nonetheless coming

What does all this imply for those who’re a house purchaser or a house owner seeking to refinance?

First, it means you shouldn’t panic about charges skyrocketing after this week’s Federal Reserve assembly. At this level, an enormous fee spike just like the one debtors noticed in 2013 appears unlikely.

Nonetheless, now shouldn’t be the time to get complacent.

Rates are still expected to rise in 2021 and 2022. And there are two large causes for that:

- Inflation — Higher inflation typically leads to higher rates. And the annual U.S. inflation fee was at a 13-year excessive in September

- Financial restoration and progress — As Covid instances proceed to say no, and the economic system continues to enhance, it appears inevitable that charges will go greater. Preserve in mid {that a} stronger economic system sometimes results in greater rates of interest for mortgage debtors

We’d see a gradual, regular fee climb fairly than a pointy improve. However most consultants agree that greater charges are coming eventually.

So, for those who’re able to lock a fee quickly, it’s a very good time to take action.

Pandemic-era, “record-low” charges could be gone for good. However there are nonetheless nice offers available for certified debtors.

Simply ensure you store round to search out the very best lender and rates of interest on your state of affairs. Doing so could save you thousands — and in immediately’s rising fee surroundings, discovering your greatest deal is extra vital than ever.

[ad_2]

Source link

{kind=link}