[ad_1]

There aren’t superb statistics on common chiropractor scholar loans. By means of my scholar mortgage consulting enterprise, I’ve helped some chiropractors with stunningly excessive scholar mortgage debt relative to their earnings. That prompted me to begin investigating to see what I might discover, and the outcomes aren’t good for the way forward for the career.

Chiropractor scholar loans are among the most crushing of any profession in america relative to earnings prospects. On this article, I’m together with my high tips about save 1000’s of {dollars} in curiosity whereas repaying your Physician of Chiropractic scholar loans.

The common chiropractor scholar mortgage steadiness is over $150,000

The most recent survey I might discover from 2014 of recent chiropractic grads confirmed that 88% had a mortgage quantity above $100,000. An academic study from early 2014 discovered that 54% of recent grads would owe over $150,000 in chiropractor scholar loans.

And that’s actually the most recent stats accessible in the present day in 2021. You’d suppose that the American Chiropractic Affiliation (ACA) would wish to replace their common chiropractic college debt variety of for no different motive than to build their case for why chiropractors must be included within the NHSC Mortgage Compensation Program. However no more moderen research have been revealed.

Additionally, College Scorecard nonetheless isn’t displaying debt ranges and default charges for many main chiropractic colleges like Palmer School of Chiropractic. So given how little knowledge is out there on the true value of chiropractic faculty, let’s take a look at one other supply of data the place we would have the ability to guess the size of the issue.

My chiropractor consumer’s common debt stage

Of the folks I’ve labored with, the common chiropractor scholar mortgage quantity has been roughly $260,000. And that quantity doesn’t embody any enterprise loans that my purchasers might have taken out in direction of opening their chiropractic practices. That is what led me to research the magnitude of the scholar mortgage drawback within the career.

For the reason that overhaul of the Grad Plus loan rules in 2006, graduate college students have been in a position to entry limitless sums of monetary assist from the federal mortgage applications. In fact, tuition has exploded in nearly each skilled college within the nation since then. And chiropractic colleges are not any completely different.

So even in the event you’re somebody who crammed out your FAFSA and utilized for all of the scholarships and grants that you can, you seemingly nonetheless completed chiropractic college with six-figure scholar debt.

Typical chiropractor incomes can’t help their regular month-to-month funds

The Bureau of Labor Statistics (BLS) places out wage data for varied jobs throughout the nation. The median earnings for a full-time chiropractor is $70,720. That’s roughly according to what I’ve seen from purchasers in my scholar mortgage consulting apply.

With such modest incomes, the common chiropractor has no hope of ever repaying their scholar debt. Even when chiropractors begin their very own apply, it’s very troublesome to make the mandatory funds on chiropractic college loans and have a life on the identical time.

What different reimbursement choices can be found?

I assist chiropractic debtors craft a scholar mortgage reimbursement technique. In case your debt-to-income (DTI) ratio goes to be above 2 throughout your profession, then selecting the best income-driven reimbursement choice is crucial.

Moreover, most chiropractors work within the non-public sector. Therefore, most aren’t eligible for Public Service Mortgage Forgiveness (PSLF). They’ll nonetheless obtain forgiveness on the finish of a 20-25-year income-driven reimbursement plan. However the scholar mortgage forgiveness from these federal applications could possibly be thought-about taxable earnings. I assist stroll purchasers by way of how a lot they should save a month to cowl their future tax legal responsibility.

Most often, I’d assist a chiropractor consumer consider the Revised Pay As You Earn (REPAYE) program or the Pay As You Earn (PAYE) program to determine which choice saved them extra money. If you happen to’re already utilizing the Earnings Primarily based Compensation plan (IBR), it is sensible to consider switching.

It’s important to see how a lot accrued curiosity you’ve got excellent, as it will be added into the principal steadiness and begin producing curiosity too in the event you change plans. Nonetheless, there will be superb causes to take action.

optimize chiropractic scholar loans

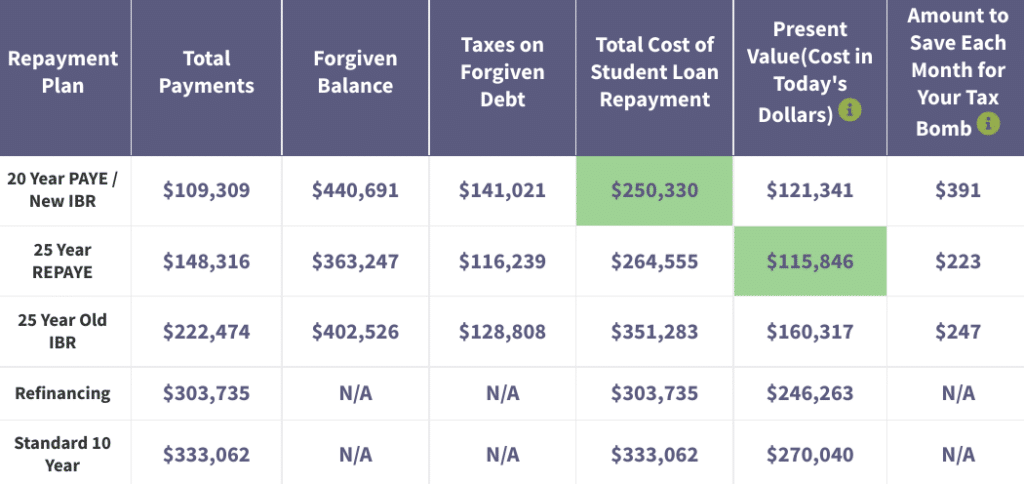

Let’s assume that Brett graduates from chiropractic college this yr with $250,000 in all federal loans at a 6% common rate of interest. He begins out at $60,000 a yr and expects his wage grows at a 3% inflation price. Right here’s how a lot paying again his loans would value below varied reimbursement plans, estimated with the proprietary software we use in scholar mortgage consults to create personalized reimbursement methods:

Let’s perceive this chart. Brett has three main income-driven reimbursement choices accessible for his federal scholar loans. The previous IBR plan is a legacy plan that’s been round a very long time. Previous IBR requires 15% of your discretionary earnings. And after 25 years, the loans are forgiven and also you’re taxed on the leftover steadiness.

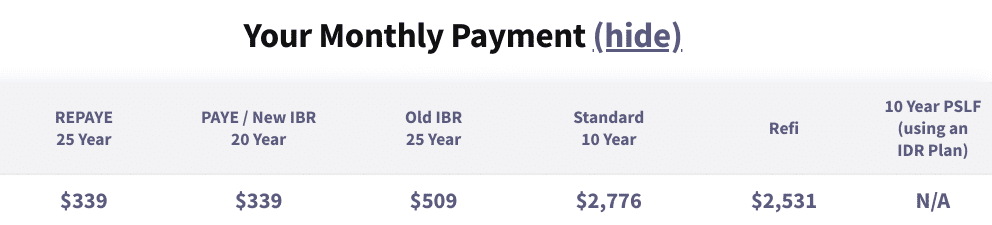

PAYE and REPAYE each require 10% of discretionary earnings, which is a decrease cost than the previous IBR plan. Below IBR, Brett would begin off paying $509 a month. Below PAYE and REPAYE, Brett would solely owe $339 a month.

If you happen to take a look at the whole value column within the first picture, clearly IBR is a giant loser. The Normal 10-year plan can be untenable as it will require $2,776 a month in mortgage funds. Clearly the Normal plan is off the desk. So we’re left with making an attempt to determine what plan is best for Brett: PAYE or REPAYE.

Selecting the best reimbursement plan

The whole cost till forgiveness below REPAYE is about $148,000. The identical determine for PAYE is roughly $109,000. The explanation for this distinction is as a result of PAYE has a 20-year forgiveness interval. REPAYE, however requires 25 years of funds earlier than you may qualify for forgiveness. So by way of whole funds over Brett’s profession, PAYE wins right here.

Now we glance to the remaining steadiness on Brett’s chiropractic scholar loans after they’re forgiven by the federal authorities. Below REPAYE, that determine is about $363,000 and with PAYE it’s about $440,000. Why does Brett have a decrease steadiness below REPAYE despite the fact that the loans have an additional 5 years to develop?

The reason being as a result of REPAYE comes with an curiosity subsidy. If you happen to’re not paying all of your curiosity, which many chiropractors received’t be, the federal government covers 50% of the unpaid curiosity. For that motive, REPAYE often leads to a decrease steadiness at forgiveness.

Do not forget that the forgiven steadiness is taxable earnings below the IRS. I’m assuming a 32% tax price. Why? As a result of Brett’s forgiven quantity will push him into the next marginal bracket. Meaning Brett will owe a six-figure tax invoice of roughly $116,000 below REPAYE and $141,000 below PAYE.

It’s necessary to notice that the American Rescue Plan recently made all student loan forgiveness tax-free till the top of 2025. We’ll be monitoring laws over the subsequent few years. If there are discussions about extending this tax profit, we’ll let . However, for now, we advocate that debtors who received’t be ending reimbursement by 2025 ought to plan as in the event that they will be charged taxes on their forgiven balances.

save for the scholar mortgage tax bomb

To the far-right of the primary chart, you’ll see a column known as “Quantity To Save Every Month For The Tax Bomb.” That is the approximate quantity I’ve estimated that Brett would wish to avoid wasting every month in an funding account to cowl that corresponding tax penalty below every reimbursement plan.

For REPAYE, that sum is smaller as a result of the tax penalty is decrease. So Brett would wish to avoid wasting about $220 a month for 25 years to cowl the tax invoice.

For PAYE, the wanted financial savings are increased as a result of the forgiveness tax penalty occurs sooner. This leads to the next forgiven steadiness and tax invoice. I calculate Brett would wish to avoid wasting about $390 a month to cowl this penalty.

Lastly I’d have a dialogue with Brett how a lot he needs to spend a month on his scholar loans. If he’d relatively have them gone in 20 years with PAYE, he would spend about $340 a month in funds and $390 a month in tax penalty financial savings for $730 whole. Maybe he’d relatively unfold out the associated fee over 25 years.

In that case, Brett would pay about $340 a month in funds and $220 a month in tax penalty account financial savings. That may lead to an estimated whole of $560 a month.

Get a personalised chiropractic mortgage reimbursement technique

The examples above define greatest reimbursement methods for one particular state of affairs. However issues might look very completely different if Brett had plenty of children (on this case IDR turns into a fair higher choice) or non-public loans (during which case refinancing to decrease rates of interest turns into just about the one manner to economize).

When you have a six-figure scholar mortgage burden from chiropractic college, click on on the button to ask us a query about your state of affairs beneath. Our crew helps chiropractors conquer big scholar mortgage balances with low value, flat fee consultations.

We’ll carry out a holistic mortgage evaluation with our proprietary simulation software to see what your greatest accessible reimbursement choices are on your kind of mortgage. (authorities cost plans, refinance with non-public scholar loans, and many others). We’ve helped over 90% of our purchasers a mean of $50,000 projected over the lifetime of their loans.

Refinance scholar loans, get a bonus in 2021

$1,050 BONUS1For 100k+. $300 bonus for 50k to 99k.1

$1,250 BONUS2 For 250k+, tiered 300 to 500 bonus for 50k to 250k.2

$1,000 BONUS3 For 100k or extra. $200 for 50k to $99,9993

$1,275 BONUS4 For 150k+. Tiered 300 to 575 bonus for 50k to 149k.4

$1,000 BONUS5For $100k or extra. $200 for $50k to $99,9995

$1,250 BONUS6 For 100k+ or $350 for 5k to 100k.6

$1,250 BONUS7For 150k+. Tiered 100 to 400 bonus for 25k to 149k.7

Undecided what to do along with your scholar loans?

Take our 11 query quiz to get a personalised suggestion of whether or not you must pursue PSLF, IDR forgiveness, or refinancing (together with the one lender we expect might provide the greatest price).

All charges listed above symbolize APR vary. 1Commonbond: If you happen to refinance over $100,000 by way of this web site, $500 of the money bonus listed above is offered straight by Scholar Mortgage Planner. Commonbond disclosure.

2Laurel Street: If you happen to refinance greater than $250,000 by way of our hyperlink and Scholar Mortgage Planner receives credit score, a $500 money bonus will likely be offered straight by Scholar Mortgage Planner. In case you are a member of an expert affiliation, Laurel Street would possibly give you the selection of an rate of interest low cost or the $300, $500, or $750 money bonus talked about above. Gives from Laurel Street can’t be mixed. Charge vary above contains non-compulsory 0.25% Auto Pay low cost. Laurel Road disclosures.3Earnest: $1,000 for $100K or extra, $200 for $50K to $99.999.99. For Earnest, in the event you refinance $100,000 or extra by way of this web site, $500 of the $1,000 money bonus is offered straight by Scholar Mortgage Planner. Charge vary above contains non-compulsory 0.25% Auto Pay low costEarnest disclosures.

4Elfi: If you happen to refinance over $150,000 by way of this web site, $500 of the money bonus listed above is offered straight by Scholar Mortgage Planner. Elfi disclosure. 5Sofi: If you happen to refinance $100,000 or extra by way of this web site, $500 of the $1,000 money bonus is offered straight by Scholar Mortgage Planner. Charge vary above contains non-compulsory 0.25% Auto Pay low cost. Sofi disclosures. 6Credible: If you happen to refinance over $100,000 by way of this web site, $500 of the money bonus listed above is offered straight by Scholar Mortgage Planner. Credible disclosure.

7LendKey: If you happen to refinance over $150,000 by way of this web site, $500 of the money bonus listed above is offered straight by Scholar Mortgage Planner. Charge vary above contains non-compulsory 0.25% Auto Pay low cost.

[ad_2]

Source link

{kind=link}