[ad_1]

The FHA Streamline Refinance

Should you at present have an FHA mortgage, the FHA Streamline Refinance is the best option to get a decrease charge and month-to-month cost.

The FHA Streamline is a “low-doc” refinance with restricted paperwork required. The lender doesn’t need to confirm your revenue or credit score, and there’s no dwelling appraisal.

Which means a Streamline Refinance closes sooner than different loans and has barely cheaper closing prices.

Due to the FHA Streamline, these with FHA loans have simpler entry to at this time’s low charges than most householders.

Verify your FHA Streamline Refinance eligibility (May 7th, 2021)

On this article:

What’s the FHA Streamline Refinance?

The FHA Streamline is a particular refinance product, reserved for householders with current FHA mortgages. An FHA Streamline is the quickest, easiest method for FHA-insured householders to refinance their mortgages into today’s low mortgage rates.

Advantages of the FHA Streamline program embrace:

- Low refinance charges — FHA mortgage charges at present common 2.5% (3.478% APR). That is an extremely low charge in comparison with many of the mortgage trade

- Decrease MIP charges — Should you bought an FHA mortgage between 2010 and 2015, you might be able to decrease your annual mortgage insurance coverage premium utilizing FHA streamline refinancing

- MIP refund — Owners who use the FHA Streamline Refinance could also be refunded as much as 68 % of their pay as you go mortgage insurance coverage, within the type of an MIP low cost on the brand new mortgage

- No appraisal — You should utilize the FHA Streamline Refinance even when your present mortgage is underwater

- No verification of job or revenue — It’s possible you’ll be eligible for FHA Streamline refinancing even if you happen to not too long ago misplaced your job or took a pay reduce

- No credit score examine — A low credit score rating gained’t cease you from utilizing the FHA Streamline program. That is nearly unattainable to search out with different refinance loans

When you have an current FHA mortgage and also you wish to refinance right into a decrease rate of interest, the FHA Streamline must be your first cease.

Its advantages are almost unmatched by some other refinance possibility.

Verify your FHA Streamline Refinance eligibility (May 7th, 2021)

FHA Streamline Refinance Charges

Immediately’s common 30-year FHA charge is 2.5% (3.478% APR). However bear in mind, the FHA mortgage insurance coverage payment provides 0.85% in annual prices. This additionally applies to Streamline refinances.

Should you’re contemplating an FHA Streamline Refinance, now is an effective time to lock in a low base charge and see larger financial savings over the lifetime of your mortgage.

Shop low FHA Streamline Refinance rates here (May 7th, 2021)

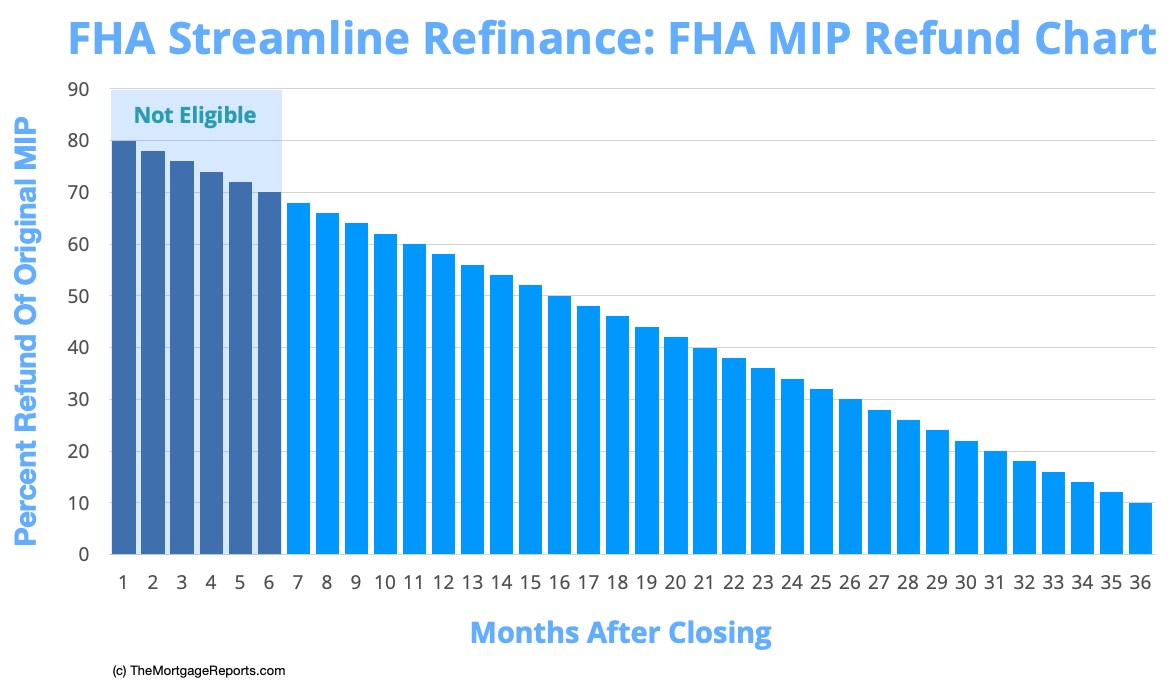

FHA MIP refund chart

There’s a further profit for FHA-backed householders refinancing throughout the first three years of their current mortgage origination.

The FHA offers a partial refund in your previously-paid upfront mortgage insurance coverage premium (UFMIP).

The dimensions of the refund diminishes because the three-year window elapses.

For instance, a home-owner who refinances an FHA mortgage after 11 months is granted a 60 % refund on their preliminary FHA UFMIP.

Thirty days later, the refund drops to 58 %. After one other 30 days, it drops to 56 %, and so forth.

| Months After Closing | MIP Refund | Months After Closing | MIP Refund | Months After Closing | MIP Refund |

| 7 | 68% | 17 | 48% | 27 | 28% |

| 8 | 66% | 18 | 46% | 28 | 26% |

| 9 | 64% | 19 | 44% | 29 | 24% |

| 10 | 62% | 20 | 42% | 30 | 22% |

| 11 | 60% | 21 | 40% | 31 | 20% |

| 12 | 58% | 22 | 38% | 32 | 18% |

| 13 | 56% | 23 | 36% | 33 | 16% |

| 14 | 54% | 24 | 34% | 34 | 14% |

| 15 | 52% | 25 | 32% | 35 | 12% |

| 16 | 50% | 26 | 30% | 36 | 10% |

Word: FHA householders are solely eligible for the Streamline Refinance program after six months. Thus, eligibility for an MIP refund begins at seven months.

This is the reason it’s not often

a good suggestion to “wait to refinance” an FHA mortgage.

With the FHA Streamline Refinance program, the earlier you refinance, the larger your refund, and the decrease your complete mortgage dimension on your new mortgage.

This lowers the month-to-month cost

and preserves the house fairness — two large positives.

Check your Streamline Refinance eligibility (May 7th, 2021)

How the FHA streamline works

For probably the most half, the FHA Streamline works like some other refinance program.

It’s obtainable as a fixed-rate or adjustable-rate mortgage; it comes with a 15- or 30-year time period; and there’s no FHA prepayment penalty to fret about.

Word, the FHA Streamline can’t be used to refinance a 30-year mortgage right into a 15-year mortgage.

It might, nevertheless, be used to increase a 15-year mortgage

right into a 30-year mortgage. Doing this lowers

month-to-month funds even additional for householders.

One other massive plus is that charges for

the FHA Streamline Refinance are the identical as mortgage charges for a homebuyer’s FHA loan. There’s no

penalty for being underwater, or for having little or no fairness.

No dwelling appraisal

The largest distinction between the

FHA Streamline and most conventional mortgage refinance choices is that the FHA

Streamline doesn’t require a house appraisal.

As an alternative, the FHA will mean you can

use your authentic buy worth as your own home’s present worth, no matter

what your own home is definitely value at this time.

Because the FHA Streamline Refinance doesn’t require an appraisal, you may refinance right into a decrease rate of interest even if you happen to owe extra in your mortgage than the house is at present value.

On this manner, with its FHA Streamline Refinance program, the FHA doesn’t care if you’re underwater in your mortgage.

Moderately, this system encourages underwater refinancing.

Even if you happen to owed twice what your own home is now value, FHA might mean you can refinance

your own home with out added price or penalty.

The “appraisal waiver” has been an enormous hit with U.S. householders, permitting limitless loan-to-value (LTV) dwelling loans by way of the FHA Streamline Refinance program.

Check your underwater refinance eligibility (May 7th, 2021)

Decreased documentation

One other massive plus: It’s pretty simple for this refinance.

The FHA Streamline Refinance doesn’t require many of the typical verifications you’d must get a brand new mortgage.

Because it’s written within the FHA’s official mortgage tips:

- Employment verification is just not required with an FHA Streamline Refinance

- Revenue verification is just not required with an FHA Streamline Refinance

- Credit score rating verification is just not required with an FHA Streamline Refinance (although most lenders will examine credit score)

If you put all of it collectively, you will be (1) out-of-work, (2) with out revenue, (3) have shaky credit score report, and (4) haven’t any dwelling fairness. But, you possibly can nonetheless be permitted for an FHA Streamline Refinance.

That’s not as loopy because it sounds, by the way in which.

To know why the FHA Streamline Refinance is a brilliant program for the FHA, we have now to recollect the FHA’s chief role is to insure mortgages — not “make” them.

It’s within the FHA’s finest curiosity to assist as many individuals as doable qualify for at this time’s low mortgage charges. Decrease mortgage charges means decrease month-to-month funds which, in principle, results in fewer mortgage defaults.

That is good for householders who need decrease mortgage charges, and it’s good for the FHA. With fewer mortgage defaults, the FHA has to pay fewer insurance coverage claims to lenders.

Check today’s FHA Streamline Refinance rates today (May 7th, 2021)

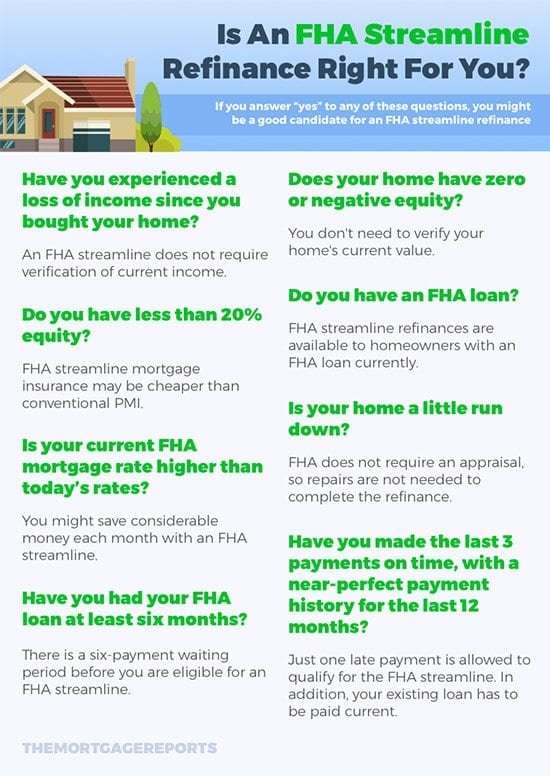

Are you eligible for an FHA Streamline Refinance?

Though the FHA Streamline Refinance bypasses “conventional” mortgage requirements, like revenue verification and credit score qualifying, this system does implement minimal requirements for candidates.

You’ll want to indicate:

- Three months of on-time mortgage

funds - At the very least 210 days since your own home buy or final

refinance - A transparent financial profit

to

refinancing - Which you could decrease your rate of interest

by not less than 0.50% normally

The official FHA Streamline Refinance tips are under. Word that not all mortgage lenders will underwrite to the official tips of the Federal Housing Administration.

Some lenders may implement credit score rating minimums or different underwriting requirements for FHA Streamline mortgages.

In case your present lender is requiring a house appraisal or

revenue verification, you’re free to buy round for a extra lenient lender that

adheres to the FHA’s minimal tips for Streamline refinancing.

Verify your FHA Streamline eligibility (May 7th, 2021)

Excellent, 3-month cost historical past is required

The FHA’s important aim is to cut back

its total mortgage pool danger. Subsequently, it’s primary qualification normal

is that householders utilizing the Streamline Refinance program will need to have an ideal

cost historical past stretching again not less than three months.

Owners with 30-day, 60-day, and 90-day late funds are

not allowed to make use of this refinancing possibility.

One mortgage late cost is allowed within the final 12 months. Loans have to be present on the time of closing.

210-day “ready interval” after shopping for or refinancing

The FHA requires that debtors make six mortgage funds on their present FHA-insured mortgage, and that 210 days cross from the newest time limit, so as to be eligible for a Streamline Refinance.

The refinance will need to have “objective”

Streamline Refinance candidates

should show a ‘Web Tangible Profit’ from the

refinance — that means there shall be a transparent financial

profit to the brand new mortgage.

Loosely, Web Tangible Profit is

outlined as lowering the “mixed charge” by not less than one-half of 1 %.

As an illustration, say a

house owner has an FHA loan opened in

Might 2013 with a charge of 5.00%, and an annual mortgage insurance coverage premium equal

to 1.35 % of the mortgage quantity.

The mixed charge is 6.35 %.

The house owner appears right into a Streamline

Refinance, and receives a charge quote at 4.75% with

MIP of 0.85 %. They save on their charge and

mortgage insurance coverage, since FHA MIP was reduced in January 2015.

The brand new mixed charge can be

5.60 %, or

three-quarters of 1 % decrease than the present mixed charge. This FHA

refinance can be eligible.

One other allowable Web Tangible Profit is to refinance from an adjustable-rate mortgage to a fixed-rate mortgage.

That is thought-about a profit as a result of fixed-rate mortgages have predictable charges and funds that carry much less danger of default.

Taking “money out” to pay payments is

not an allowable Web Tangible Profit.

Check your FHA Streamline Refinance eligibility (May 7th, 2021)

Employment and revenue are usually not verified

The FHA doesn’t require verification of a borrower’s employment or annual revenue as a part of the FHA Streamline course of.

There is no such thing as a Verification of Employment, nor are there paystubs, W-2s or tax returns required for approval.

You will be unemployed and get permitted for an FHA Streamline Refinance as long as you continue to meet the opposite program necessities.

Credit score scores are usually not verified

The FHA doesn’t confirm credit score scores as a part of the FHA Streamline Refinance program. As an alternative, it makes use of cost historical past as a gauge for future mortgage efficiency.

Which means FICO scores under

640, under 620, under 580, and even under 500 could possibly be

eligible for Streamline Refis.

Some lenders, nevertheless, create

their very own minimal necessities. Verify your lender’s credit score qualifying tips

earlier than making use of.

Click here to verify your FHA rate reduction (May 7th, 2021)

Mortgage balances might not improve to cowl mortgage prices

The FHA prohibits growing a

Streamline Refinance’s mortgage steadiness to cowl related mortgage fees, like closing prices.

The mortgage quantity is proscribed by

the maths formulation of (Present Principal Steadiness + Upfront Mortgage Insurance coverage

Premium).

All different prices — together with origination

fees, title fees, and pay as you go taxes and insurance coverage — should

be both (1) Paid by the borrower as money at closing, or (2) Credited by the

mortgage officer in full.

The latter known as a “no-cost FHA

Streamline.”

No cash-out

You’ll be able to’t take further money out when

refinancing with an FHA Streamline mortgage. This refinance is designed primarily

to decrease

the house owner’s rate of interest

and cost.

Nevertheless, the FHA cash-out refinance is

one other refinancing possibility provided by the FHA.

It permits you to open a mortgage of as much as 80 % of your own home’s

worth. If that quantity is bigger than your

present mortgage steadiness, you are taking the distinction in money.

Owners can use these funds for any objective: to pay

off debt, enhance your own home, or create an emergency fund.

Value determinations not required

The FHA isn’t involved about dwelling worth — it’s insuring your mortgage regardless.

Subsequently, the FHA doesn’t require value determinations for its Streamline Refinance program. As an alternative, it makes use of the unique buy worth of your own home, or the newest appraised worth, as its valuation level.

Properties which might be underwater are nonetheless FHA Streamline-eligible.

Must you use the FHA Streamline?

What occurs to FHA mortgage insurance coverage if you happen to Streamline Refinance?

Like different FHA loans, the FHA Streamline Refinance requires debtors to pay mortgage insurance coverage.

Even if you happen to’ve constructed fairness within the dwelling since buying it, the FHA Streamline Refinance can’t be used to eradicate mortgage insurance coverage premium (MIP).

FHA debtors are required to make two varieties of mortgage insurance coverage funds: an upfront mortgage insurance coverage cost paid at closing, plus an annual cost break up into 12 installments, that are paid together with your mortgage every month.

- Upfront Mortgage Insurance coverage Premium (UFMIP) = 1.75% of the mortgage quantity for most up-to-date FHA loans and refinances

- Annual Mortgage Insurance coverage Premium (MIP) = 0.85% of the mortgage quantity most up-to-date FHA loans and refinances

With respect to mortgage insurance coverage premiums, householders utilizing the FHA Streamline Refinance program are break up into two lessons:

- Owners whose new mortgage replaces an FHA-backed mortgage endorsed previous to June 1, 2009

- Owners whose new mortgage replaces an FHA-backed mortgage endorsed on/after June 1, 2009.

Owners within the top quality -— these with “previous” FHA mortgages — are assigned completely different mortgage insurance coverage than newer FHA householders.

Particularly, these older FHA

mortgages qualify for a diminished upfront premium of

simply 0.01%

of the mortgage quantity, or $10 for

each $100,000 borrowed.

Moreover, month-to-month mortgage

insurance coverage is simply 0.55 % of the mortgage quantity yearly,

in comparison with “common” MIP of 0.85 % per 12 months.

FHA Streamline MIP For Loans Endorsed On/After June 1, 2009

In case you are refinancing an FHA mortgage by way of the FHA Streamline Refinance program and your current FHA mortgage was endorsed on, or after, June 1, 2009, your mortgage insurance coverage premium schedule in your new FHA mortgage is as follows.

Upfront Mortgage Insurance coverage Premiums (UFMIP)

For an FHA Streamline Refinance changing a mortgage endorsed on, or after, June 1, 2009, the FHA upfront mortgage insurance coverage premium is the same as 1.75 % of your mortgage dimension, or 175 foundation factors.

That is $1,750 for each $100,000 borrowed. The FHA routinely provides the $1,750 premium to your mortgage steadiness for you — it’s not paid as money.

Nevertheless, not all refinancing households pays the total quantity.

As proven within the chart above, these utilizing an FHA Streamline inside three years of their authentic mortgage stand to get an upfront MIP refund.

This could considerably decrease the quantity of UFMIP added to your new mortgage, thus lowering the quantity you need to pay total.

Annual Mortgage Insurance coverage Premiums (MIP)

The annual MIP schedule for an FHA Streamline Refinance which replaces a mortgage from on, or after, June 1, 2009 is as follows :

- 15- & 30-year mortgage phrases with

an LTV over 90 %: 0.85% annual MIP, payable for the life

of the mortgage - 15-

& 30-year mortgage phrases with an LTV beneath 90 %: 0.85% annual

MIP, payable for 11 years

Word that these MIP prices could also be

decrease than what you’re paying in your current FHA dwelling mortgage.

In January 2015, the FHA lowered its mortgage insurance coverage premiums on 30-year loans, making it cheaper to hold an FHA dwelling.

In case your present FHA MIP is increased than what’s proven above, take into account beginning a refinance instantly to learn from a new, decrease FHA MIP.

FHA Streamline Refinance MIP (For Loans Endorsed Earlier than June 1, 2009)

In case your current FHA dwelling mortgage was

endorsed previous to June 1, 2009, your mortgage insurance coverage premiums have been

“grandfathered.”

You’ll be able to refinance by way of the FHA

Streamline Refinance program and pay diminished charges for each your upfront and annual mortgage

insurance coverage premium.

Upfront Mortgage Insurance coverage Premiums (UFMIP)

For an FHA Streamline Refinance that replaces a mortgage endorsed previous to June 1, 2009, the brand new FHA mortgage’s upfront mortgage insurance coverage is the same as 0.01 % of the mortgage dimension, or 1 foundation level.

For instance, in case your new FHA Streamline Refinance is for $100,000, the FHA will assess a $10 upfront mortgage insurance coverage premium (MIP) to be paid at closing.

The FHA routinely provides the $10 cost to your new mortgage steadiness.

Annual Mortgage Insurance coverage Premiums (MIP)

Annual MIP is equally low cost for older FHA loans. For an FHA Streamline Refinance changing an FHA mortgage endorsed previous to June 1, 2009, the annual MIP is 0.55 % yearly, or 55 foundation factors.

The whole annual MIP schedule is as follows:

- 15- & 30-year mortgage phrases with

an LTV over 90 %: 0.55% annual

MIP, payable for the lifetime of the mortgage - 15-

& 30-year mortgage phrases with an LTV beneath 90 %: 0.55% annual

MIP, payable for 11 years

FHA MIP Cancellation Coverage

The FHA requires some householders to pay mortgage insurance coverage for so long as their mortgage is in impact.

In case your FHA Streamline Refinance replaces a mortgage from on, or after, June 1, 2009, the principles in your FHA MIP cancellation are as follows:

- LTV of 90 % or much less on the time of closing: MIP is required for 11 years

- LTV larger than 90 % on the time of closing: MIP required for the lifetime of the mortgage

The FHA MIP cancelation coverage applies to 15-year mortgage phrases and 30-year mortgage phrases equally.

Word that refinancing householders are welcome to carry money to closing so as to scale back their mortgage steadiness and alter their MIP disposition. Nevertheless, not everybody could have the money to make such a transfer.

This is the reason, when exploring an FHA

Streamline Refinance, you must also have a look at different mortgage

refinance choices together with the traditional

mortgage mortgage by way of Fannie Mae or Freddie Mac, which is on the market with almost

each mortgage lender.

The FHA permits its householders to refinance to a conventional loan

to cancel FHA MIP.

FHA Streamline Refinance FAQ

FHA Streamline is a refinance program that solely present FHA householders can use. It’s sooner and simpler than most refinance packages, with no documentation required for revenue, credit score, or dwelling appraisal.

An FHA Streamline Refinance may help householders decrease their annual mortgage insurance coverage premium (MIP) and even get a partial refund of their upfront MIP cost.

The FHA Streamline Refinance resets your mortgage with a decrease rate of interest and month-to-month cost. When you have a 30-year FHA mortgage, you should utilize the FHA Streamline to refinance into a less expensive 30-year mortgage. 15-year FHA debtors can refinance right into a 15- or 30-year mortgage.

The FHA Streamline doesn’t cancel mortgage insurance coverage premium (MIP) for individuals who pay it. However annual MIP charges might go down, relying on when the mortgage was originated.

The borrower has to pay closing prices on an FHA Streamline Refinance. Not like different varieties of refinances, you can not roll these prices into your mortgage quantity.

FHA Streamline closing prices are sometimes the identical as different mortgages: 2 to five % of the mortgage quantity, which might equal $3,000 to $7,500 on a $150,000 mortgage. The distinction is, you don’t need to pay for an appraisal on an FHA Streamline, which might save about $500 to $1,000 in closing prices.

No, the FHA Streamline Refinance doesn’t eradicate mortgage insurance coverage. Refinanced FHA loans nonetheless have annual mortgage insurance coverage, in addition to a brand new upfront mortgage insurance coverage payment equal to 1.75 % of the mortgage quantity. The upfront payment is added to your mortgage quantity.

Nevertheless, if you happen to use the FHA Streamline Refinance inside three years of opening your mortgage, you’ll be refunded a part of your authentic UFMIP payment — thus reducing the overall mortgage quantity.

To qualify for an FHA Streamline Refinance, your present dwelling mortgage have to be insured by the FHA. Should you’re unsure whether or not it’s, ask your lender.

FHA additionally requires three months of on-time funds, and a 210-day ready interval since your own home’s final time limit (both buy or refinance). Lastly, the FHA Streamline Refinance will need to have a “objective.” That normally means the refinance must decrease your mixed curiosity and insurance coverage charge by not less than 0.50%.

Technically, the FHA Streamline doesn’t require a credit score examine. Which means householders might probably use the Streamline Refinance even when their credit score rating has fallen under the 580 threshold for FHA loans. Nevertheless, some lenders might examine your credit score report anyway. So in case your credit score is on the decrease finish, be sure you store round.

No, you can not take money out on an FHA Streamline Refinance.

The FHA Streamline Refinance is a “low-doc” refinance mortgage; it requires much less paperwork than most different mortgages. However there’s nonetheless some documentation required. For an FHA Streamline Refinance, you’ll nonetheless want:

– A mortgage utility

– A present mortgage assertion displaying a six month cost historical past

– Contact info on your employer (the lender might confirm employment, however not revenue)

– Two months’ value of financial institution statements displaying you may cowl out-of-pocket closing prices

– Utility payments displaying you employ the house as a major residence

FHA householders are eligible for a Streamline Refinance 210 days after their final closing. Which means you need to have made six consecutive mortgage funds since you bought or final refinanced the house.

Sure, you should utilize the FHA Streamline Refinance greater than as soon as. You simply want to fulfill FHA’s tips — that means it’s been not less than 210 days since your final refinance, you’ve made your final three funds on time, and you’ll decrease your charge round 0.50%.

The large advantage of an FHA Streamline Refinance is that you could swap your FHA mortgage to a decrease charge and month-to-month cost. It can save you cash by eliminating your current increased rate of interest with out as a lot problem as conventional refinancing choices.

One other advantage of the FHA Streamline is that there’s no dwelling appraisal – so you may refinance right into a decrease FHA mortgage charge even when you have little or no fairness or your mortgage is underwater.

The FHA Streamline Refinance might be value it if you happen to can decrease your mortgage charge and month-to-month cost a big quantity. It’s an particularly whole lot for householders who bought or refinanced from 2010 to 2015, as a result of FHA has since lowered its annual mortgage insurance coverage charges.

By refinancing a pre-2015 mortgage with the FHA streamline, you might be able to drop your annual mortgage insurance coverage charge from over 1 % to simply 0.85 %.

FHA mortgage insurance coverage premium (MIP) lasts 11 years if you happen to made a down cost of 10 % or extra, or the total lifetime of the mortgage in case your down cost was lower than 10 %.

The one option to do away with FHA mortgage insurance coverage is my refinancing your present FHA mortgage into a traditional mortgage with out PMI.

To do that, you’ll want not less than 20 % fairness in your house and a credit score rating of not less than 620 or increased. You’ll additionally must pay closing prices and full the brand new mortgage’s underwriting course of.

What are at this time’s FHA Streamline charges?

FHA mortgage charges are low and householders sometimes shut in lower than 30 days. Keep in mind: the sooner you shut, the larger your FHA MIP refund.

Get began by checking at this time’s FHA refinance charges to see what you

might save.

[ad_2]

Source link

{kind=link}