[ad_1]

ARMs are on the rise. Do you have to get one?

Adjustable-rate mortgages are getting extra common.

In keeping with the Mortgage Bankers Association, the spike in ARMs is being pushed by rising mortgage charges and rising residence costs.

Why is that? Nicely, ARMs usually have decrease rates of interest than fixed-rate mortgages — at the least at first. So residence patrons may doubtlessly decrease their month-to-month funds and improve their budgets.

However ARMs include very actual dangers, too. So it’s vital to grasp the professionals and the cons earlier than signing on.

Verify your mortgage eligibility (Jun 1st, 2021)

On this article (Skip to…)

What’s an ARM?

An ARM is an adjustable-rate mortgage. In different phrases, its mortgage price can float up and down in step with the bigger rate of interest market.

That makes an ARM very totally different from most mortgages, which have mounted rates of interest.

With a fixed-rate mortgage (FRM), you’ll be able to make sure that all of your month-to-month funds would be the identical over the lifetime of the mortgage.

However with an ARM, you don’t have the identical assure. Your price may change down the road, and with it, your month-to-month cost.

Decrease value = better danger

The attraction with ARMs is that they usually begin with a decrease mortgage price — and thus a decrease month-to-month cost — than an equal FRM.

A decrease month-to-month mortgage cost means you’ll be able to usually afford a much bigger mortgage quantity. So in at the moment’s market, the place actual property costs are quickly rising and rates look set to increase, ARMs may appear extra enticing to some debtors.

For first-time residence patrons an ARM may even seem like a lifeline.

That’s as a result of the decrease preliminary month-to-month funds may imply they will nonetheless afford to purchase a house, although maybe a extra modest one than they had been dreaming of.

Nevertheless, debtors who go for an ARM are shouldering much more danger if charges rise in a while. That low price is usually solely locked for the primary 5-10 years. After that, it’s potential in your price and cost to rise to an unaffordable stage.

So, how are you aware if an ARM is a great monetary selection for you?

Is an ARM a good suggestion in at the moment’s market?

Whether or not or not it is best to get an ARM depends upon two components: your urge for food for danger and your future plans as a home-owner.

Your character and danger administration

ARMs are inherently riskier than FRMs, as a result of your price and cost can change. So your selection relies upon partly on how a lot danger you’re keen to simply accept as a home-owner.

Will charges be larger in 5-10 years when your fixed-rate interval ends? And if that’s the case, by how a lot?

Nobody can say for sure. Economists are at the moment divided over what they suppose will occur to inflation. And if it finally ends up rising in a sustained and sharp manner, homebuyers with ARMs may find yourself uncovered to a number of danger.

Understanding ARM caps needs to be central to your danger administration technique. (For those who’re unfamiliar with ARM caps, there’s more information below.)

Even when you’ve got the form of character with which risk-taking comes naturally, you continue to want to pay attention to simply how excessive your month-to-month funds may go. And also you’ll need to ensure you would cope if the worst occurs.

Private plans

Some residence patrons who select an ARM plan to keep away from the chance of upper charges altogether.

An ARM may be completely secure in the event you’re planning on shifting or refinancing the mortgage inside your preliminary fixed-rate interval. Since you’ll shut the ARM earlier than larger charges can kick in.

Nevertheless, there’s at all times danger of plans altering.

A transfer might be delayed because of household or work plans altering, or sudden monetary troubles. And there’s no assure a refinance will make sense within the subsequent few years — if charges go up, your subsequent residence mortgage might be dearer in any case.

That’s to not say an ARM is at all times a foul concept. Many residence patrons do transfer earlier than their fixed-rate interval ends, and save some huge cash because of their ARM selection. Nevertheless it’s vital to completely perceive the dangers earlier than selecting this sort of mortgage.

Compare mortgage options (Jun 1st, 2021)

Right now’s ARM charges versus mounted charges

Charges for ARMs are historically decrease than these for FRMs. However the hole narrows and widens over time. And it additionally depends upon the kind of mortgage you need.

For instance, in April 2021, the common price throughout all ARM loans was 3.10%, in response to ICE Mortgage Technology. The common price for all fixed-rate mortgages was 3.22%.

Nevertheless, the hole for standard ARM loans was extra enticing: 3.25% for FRMs in contrast with 2.1% for ARMs. Let’s have a look at what meaning in chilly, arduous {dollars}.

An instance in {dollars}

Utilizing The Mortgage Experiences’ mortgage calculator, we modeled the numbers for a $250,000 residence with a $50,000 down cost, making the standard mortgage quantity $200,000:

| Fastened-Price Mortgage | Adjustable-Price Mortgage | |

| Curiosity Price | 3.25% | 2.1% |

| Month-to-month Principal & Curiosity Fee | $870 | $750 |

| Mortgage Curiosity Paid in 5 Years | $31,300 | $20,000 |

That $120 a month distinction appears fairly good. It would make the distinction between your turning into a home-owner or persevering with to lease. Or it could allow you to purchase a nicer, extra expensive residence than in any other case.

However, in the event you’re shopping for a endlessly residence (or one you propose to remain in at the least 10 years), a hard and fast price may look extra enticing.

The funds are somewhat larger, however they’re assured to remain the identical over the lifetime of the mortgage. And that gives a number of peace of thoughts.

How ARM charges work

Adjustable price mortgages are extra complicated than fixed-rate loans. For those who’re contemplating one, you’l need to perceive the ins and outs of how adjustable charges work.

Hybrid ARMs — An preliminary mounted price

These days, most ARMs are hybrid ones. Which means they arrive with an preliminary interval when the speed is mounted. Solely when that interval ends can the speed float up and down.

You’ll see ARMs marketed with an x/y designation, equivalent to 7/1.

The primary numeral is the variety of years the preliminary fixed-rate interval lasts. And the second quantity is the frequency with which your lender can regulate the speed after that preliminary interval ends.

Maybe the most typical kind is the 5/1 ARM. Which means the preliminary fixed-rate interval lasts 5 years. And the /1 means lenders can regulate the speed each one 12 months (yearly).

Importantly, most ARMs nowadays have a complete mortgage time period of 30 years.

Which means, for a 5/1 ARM:

- Your preliminary rate of interest is mounted for five years

- The speed can regulate annually after that for the remaining 25 years

- Your house is totally paid off on the finish of the 30-year mortgage

There are different ARM flavors, too. You may select from the preferred ones: 3/1, 5/1, 7/1, and 10/1, although you might discover others.

However the longer your preliminary interval, the upper the mortgage price you’re prone to be supplied.

Verify your new rate (Jun 1st, 2021)

ARM caps

Right now, most ARMs include caps. These restrict the quantity your mortgage price can rise. ARM caps apply in 3 ways:

- Restrict the quantity your price can rise on the first adjustment

- Restrict the quantity your price can rise with every subsequent price adjustment

- Restrict the quantity your price can rise over the whole lifetime of your mortgage mortgage

Nevertheless, such caps should not legally required. So it is best to examine that the ARMs you’re supplied have these invaluable borrower protections.

You must also be sure you’re comfy with the extent of safety supplied.

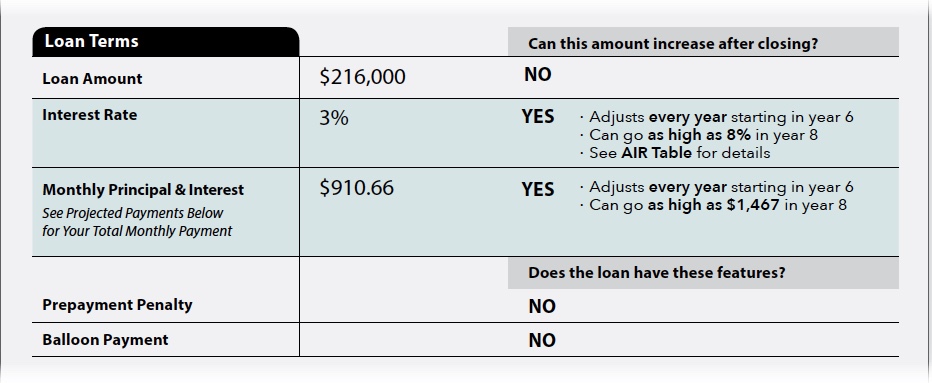

Because of the CFPB, your “Mortgage Estimate” (one other identify for the quote lenders should ship you) should present the extent of your publicity to danger.

Look on the primary web page of your estimate for this part:

Picture: Client Monetary Safety Bureau

You’ll see that, on this instance, your preliminary month-to-month cost of $910 may shoot as much as $1,467 in 12 months eight. That ought to solely occur if different rates of interest rise sharply. However they could.

So it is advisable ask your self: How assured am I that I may comfortably afford that larger cost at the moment — and probably larger funds going ahead?

For those who’re not comfy with the prospect of upper funds, an ARM doubtless isn’t best for you.

Planning forward: The place will charges be in 5 years?

Most debtors who select an ARM have a hard and fast price for the primary 5 years. So the massive query to think about is, the place will charges be 5 years from now, when the mounted interval ends?

Nobody can say for sure.

The late Harvard economist John Kenneth Galbraith as soon as stated, “The one perform of financial forecasting is to make astrology look respectable.” And he was proper. As a result of anybody who predicts with certainty the place mortgage charges might be subsequent week — not to mention in 5 years — is greater than prone to be proved incorrect.

What we can do is have a look at what’s influencing charges and guess the place they could find yourself. Proper now, that’s not wanting so good.

Charges set to go larger?

In the meanwhile, the Federal Reserve is retaining rates of interest artificially low. Many of the charges you pay (together with ARMs which are past their preliminary fixed-rate interval) are straight linked to the federal funds price. And that’s at the moment at its all-time low.

However many economists worry that we’re about to expertise a bout of higher inflation because the financial restoration from the COVID-19 pandemic features traction.

That may power the Fed to hike its charges — inflicting ARM charges to rise — maybe sharply and for years or many years to return.

Sure, we’ve grown used to uber-low rates of interest during the last decade or so. However they’re not regular or assured. And also you actually shouldn’t depend on them staying the place they’re in the event you go together with an ARM.

The best way to determine between a fixed- and adjustable-rate mortgage

To sum it up, now is definitely a really dangerous time to purchase your endlessly residence utilizing an ARM.

Sure, you’ll be able to refinance to an FRM or one other ARM additional down the road. However that’s not low cost. And there’s a great probability each these charges may have risen by then.

So, pay shut consideration to the caps we mentioned above that restrict your publicity to danger. And ask your self: Will you actually be capable of comfortably afford these larger funds in the event that they turn out to be needed?

You must also query how sure you might be that you just’ll transfer residence earlier than your preliminary, fixed-rate interval expires, if that’s your plan.

What you don’t need to do is be dazzled by the financial savings you’ll be able to initially make with an ARM and ignore all of the dangers.

That is a type of choices you need to make with due consideration. Your mortgage lender and mortgage officer can assist you determine.

However finally, solely you can reply the query: “Is an ARM mortgage a good suggestion?”

Sources for debtors: For those who’re contemplating getting an ARM, you’ll be able to obtain a free PDF of the CHARM booklet (Client Handbook on Adjustable-Price Mortgages) from the Client Monetary Safety Bureau (CFPB). It’s 12 pages lengthy and is filled with important data.

[ad_2]

Source link

{kind=link}